The Specialty M&A Paradox

Specialty platforms have never been more desirable, but deal flow remains relatively muted.

The M&A market for special intermediaries is caught between two powerful, opposing forces that are shaping its trajectory.

On one side, specialty platforms have never been more desirable, attracting intensely competitive buyer interest. On the other, deal flow remains relatively muted, constrained by a profound lack of supply.

Even so, specialty M&A rebounded in 2025, delivering 149 announced U.S. transactions—up 24% over the 120 deals recorded in 2024. However, this number was still down by 17% from the record high in 2023 of 181 deals in the United States.

The estimated number of available specialty intermediary firms has declined from 2,000 in 2021 to 1,700 firms in 2025, even as the universe of independent retail firms has remained near 39,000. However, demand for specialty firms has increased and is currently consolidating at 8.8%, while retail is consolidating at a rate of 1.8%.

Against this backdrop, several interesting trends emerged in 2025 that may point toward even sunnier days for dealmaking.

First was the surge in platform investments by stand-alone private capital firms, a buyer group distinct from the more common private capital-backed strategics. This group’s activity went from five deals in 2024 to 16 deals in 2025, highlighting growing confidence in the long-term value of specialty intermediaries. A prime example was Aquiline Capital Partners’ formation of Avondale Risk, a new national third-party administration (TPA) platform built by acquiring California-based Intercare, InterMed, and George Hills. This move created immediate scale and signaled Aquiline’s intention to expand Avondale into a leading consolidator across the TPA landscape.

At the same time, large strategic buyers—which include many private capital-backed firms and public entities— continued to reshape the upper tiers of the specialty market. The most prominent transaction was Brown & Brown’s $9.8 billion acquisition of Accession Risk Management Group, the parent company of both Risk Strategies and One80 Intermediaries. The deal underscored the continued appetite among major brokers to strengthen their specialty capabilities and diversify revenue across higher-growth segments.

Even carriers stepped up their activity with 14 transactions in 2025, more than double the deals recorded in 2024, as they searched for growth in a softening market.

The most dramatic trend emerging from this battleground backdrop of supply versus demand has been the push in specialty firm valuations to record levels. Valuations for (primarily delegated authority) specialty firms in 2025, as a multiple of EBITDA, averaged 13.9x on an upfront base purchase price. The potential total enterprise value for these firms reached 19.4x when achieving the maximum earnout. This was up significantly over 2024 valuations when base purchase price was 12.6x and max earnout was 16.5x of pro forma EBITDA.

Valuations across the entire insurance brokerage landscape are maintaining elevated levels, or even increasing. But valuation growth for specialty firms is outpacing the overall insurance brokerage market, trading at a 4.8x valuation premium compared to average retail valuations. Note that all valuation statistics here are based on deals completed by MarshBerry.

M&A Market Update

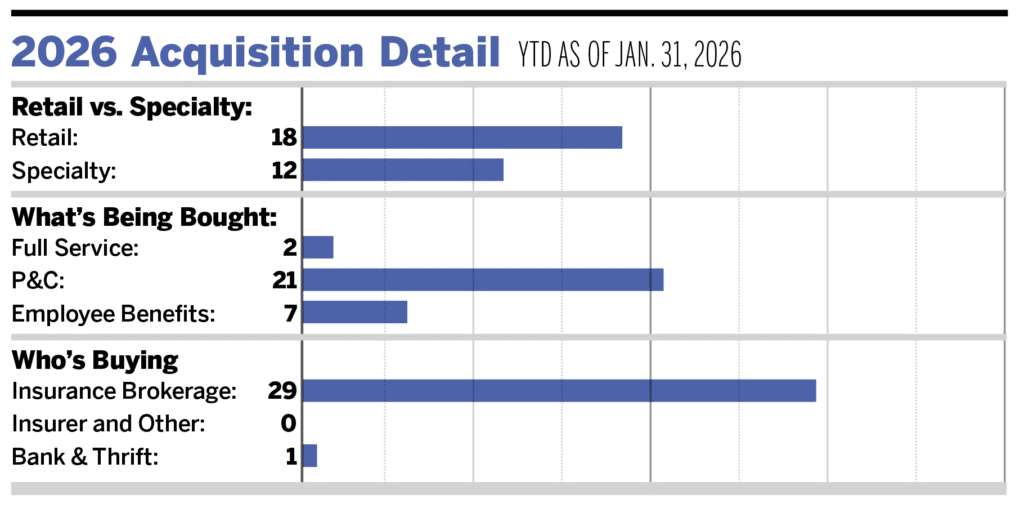

As of Jan. 31, there were 30 announced insurance brokerage M&A transactions in the United States in 2026. Private capital-backed buyers accounted for 20 of the 30 deals (66.6%) through January. Independent agencies were buyers in six deals, representing 20% of the market. Bank buyers announced one transaction in January. Deals involving specialty intermediaries as targets accounted for 12 transactions.

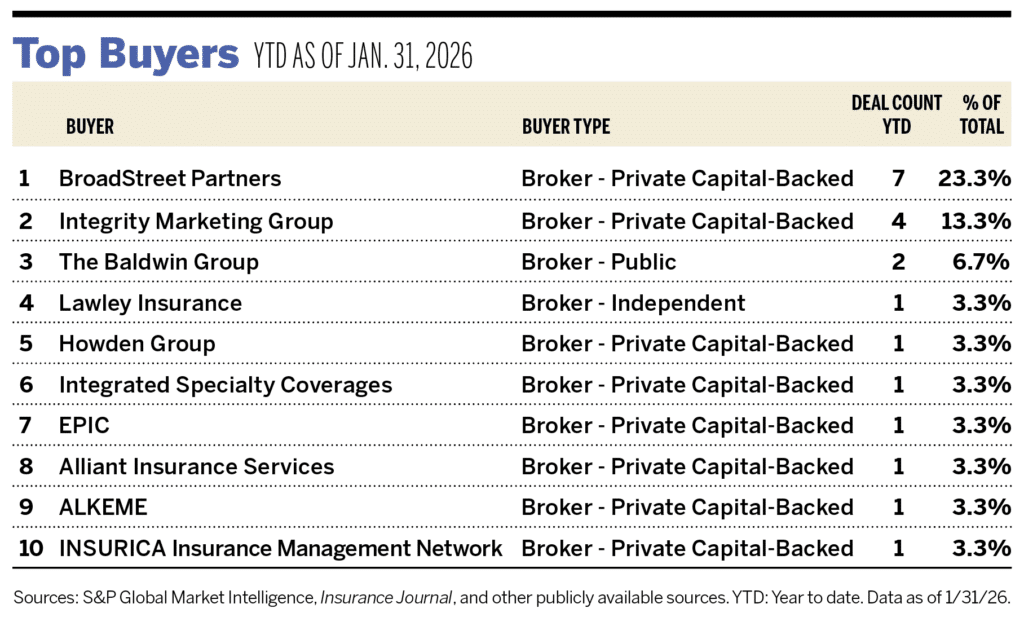

Ten buyers accounted for 66.7% of all announced transactions year to date, while the top three (BroadStreet Partners, Integrity Marketing Group, and The Baldwin Group) accounted for 43.3% of the 30 transactions.

Notable Transactions

- Jan. 8: The Baldwin Group completed the acquisition of Capstone Group, a Philadelphia-area independent insurance brokerage, strengthening its presence in one of the largest and most diverse regional economies in the United States. Founded in 2013, Capstone provides risk management, group health and ancillary benefits, and property and casualty solutions. MarshBerry served as an advisor to Capstone Group on this transaction.

- Jan. 21: EPIC acquired The Bond Exchange, a California-based surety bond agency, adding specialized underwriting and brokerage expertise to its national surety practice. Founded in 1999, The Bond Exchange brings deep experience supporting complex surety programs across industries such as construction, real estate, mining, renewable energy, technology, and private equity. MarshBerry served as an advisor to The Bond Exchange on this transaction.

- Jan. 30: Novacore agreed to acquire CP Insurance Associates, a Texas-based insurance services agency focused on lender-placed insurance and coverage programs for financial institutions and specialty lenders. Founded in 1977, CPIA serves banks, mortgage servicers, credit unions, and other lending-focused clients with collateral protection, compliance support, and technology-enabled insurance administration. MarshBerry served as an advisor to CP Insurance Associates on this transaction.