Brokerage M&A Holds Firm in Volatile Economy

It wasn’t an easy ride, but insurance brokerage deal volume in 2025 eclipsed the previous year. Can the industry maintain course in the face of growing headwinds?

The scope of insurance brokerage mergers and acquisitions (M&A) in 2025 will be remembered as another example of this industry’s resilience in the face of economic uncertainty and market challenges.

The market entered 2025 facing one of the most volatile economic environments in years. Fluctuating interest rates, shifting inflation dynamics, and questions around trade and fiscal policy changes as the second Trump administration began created instability that directly influenced capital markets and, by extension, valuations of publicly traded insurance brokers.

Despite slowing organic growth and challenging valuations for public brokers, 2025 was the third-highest year for insurance brokerage mergers and acquisitions, according to MarshBerry data. The 854 announced deals just edged out 2024’s 847 transactions.

Even with a shifting economic environment and all signs pointing toward a softening market, average firm and platform valuations in 2025 reached record levels.

Supply of specialty and employee benefits firms continues to lag demand, impacting deal numbers. Wealth advisory hit another high mark for transactions, with private capital and insurance brokerages leading the buyer groups.

As concerns increased about an insurance cycle shifting toward a softer rate environment, highlighted by slowing (or even decreasing) premiums and tapering organic growth, investors began rotating out of the sector. After peaking in March 2025, stock valuations for public brokers ended the year collectively down 10.2% as calculated by the MarshBerry Broker Composite Index. This decline stood in stark contrast to broader equity indices, with the S&P 500 and Dow Jones Industrial Average rising 16.4% and 13.0% in 2025, respectively.

Despite this environment, M&A activity stayed on pace and valuation multiples for private brokerages remained elevated. Some valuations reached all-time highs, with top-performing platform firms fetching record multiples in 2025.

The 854 announced brokerage transactions represented the third-most-active year on record, trailing only 2021 and 2022 for total dealmaking and inching above 2024’s 847 announcements. Private capital continued to exert meaningful influence, using declining capital costs and fresh dry powder to pursue deals that could offset slowing organic growth.

Carrying over from 2024’s “year of big deals,” the largest strategics continued buying in 2025. Standout transactions included Gallagher’s $1.2 billion acquisition of Woodruff Sawyer, Brown & Brown’s $9.8 billion acquisition of Accession Risk Management, Ryan Specialty’s purchase of Velocity Risk Underwriters for $525 million, and The Baldwin Group’s acquisition of CAC Group worth $1.03 billion.

The 2026 economic outlook remains a moving target, and the insurance rate cycle is shifting toward softer, more competitive waters. Still, all signs point to another active year for insurance brokerage M&A and elevated valuations for top-performing firms.

MarshBerry believes that as the capital markets become even more friendly, and as the pressure to generate revenue to replace slowing organic growth increases, demand for partners will grow—either through recapitalizations or as new acquisitions. Expect deal activity in 2026 to be defined by well-capitalized private capital-backed brokers and perhaps a few new public entities, all potentially leading to more large strategic acquisitions.

The Economic Picture

While 2025 will be considered a strong economic year, it never felt easy. The U.S. economy endured many ups and downs, including dramatic shifts in trade and fiscal policy and the longest federal government shutdown in history. However, once past the rocky first quarter, there were indicators of an economy that was fluctuating and perhaps improving: real gross domestic product (GDP) grew at a higher-than-expected rate, inflation cooled, interest rates were cut, and equity markets proved strong.

GDP Remains Resilient

After 2024 exceeded expectations for GDP, forecasters were optimistic heading into 2025. But the new year started off with a surprise: GDP shrank in the first quarter, driven primarily by reduced federal government spending and rising imports, paired with a significant increase in private inventories in anticipation of new U.S. tariffs. Imports then declined rapidly in the second quarter, and inventories also fell substantially. Imports dropped again in Q3, but at a significantly slower rate than in the second quarter. Seasonally adjusted annualized gains in GDP for the first three quarters of 2025 were -0.6%, 3.8%, and 4.3%.

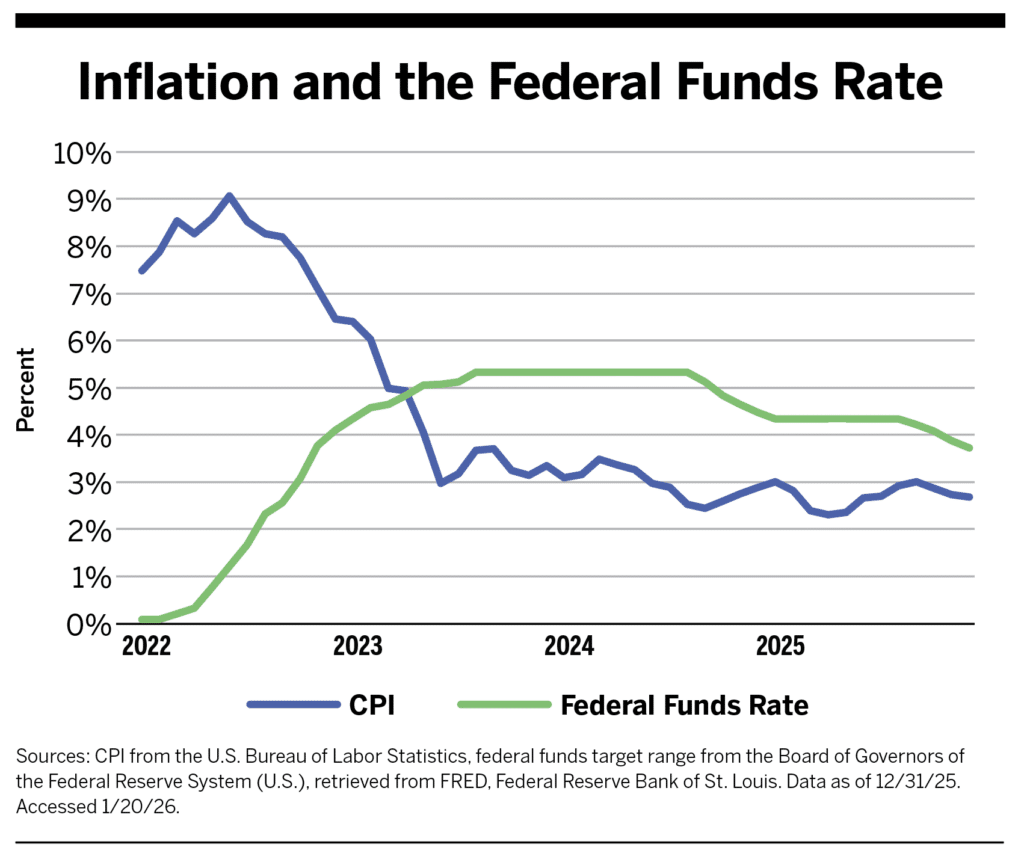

Inflation Stabilizes as Fed Steps Back

On average, inflation was lower in 2025 than in 2024. But the Consumer Price Index (CPI) barely dropped through the year as the Federal Reserve (Fed) focused on employment.

As a result, the Fed held its federal funds target range steady for most of 2025 following three rate cuts in the last four months of 2024. In September 2025, the Fed announced that it judged the downside risks to employment had risen and reduced the federal funds rate by a quarter percentage point. Two more quarter-point cuts followed in October and December as unemployment edged up. The target range for the federal funds rate finished 2025 at 3.5% to 3.75%.

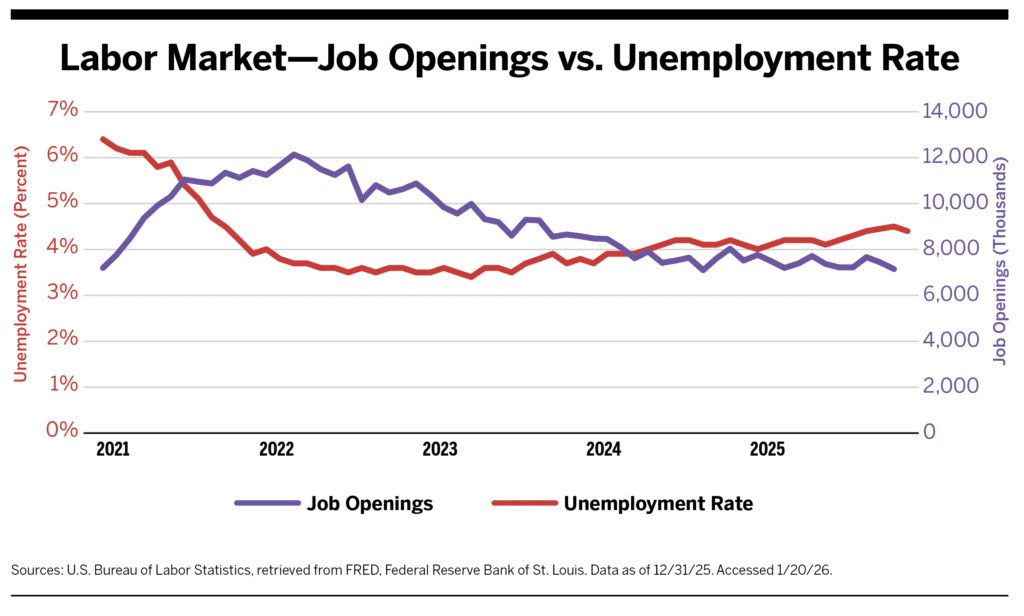

The Labor Market Cools

U.S. unemployment reached 4.5% in November 2025, its highest point since October 2021, before dropping to 4.4% to finish the year. In its December meeting, the Fed cited evidence of a cooling labor market: slowing overall employment growth, a rise in initial claims for unemployment insurance benefits, declining job openings alongside an uptick in layoffs, and survey measures indicating that the balance between labor demand and supply was weakening.

Healthy unemployment is generally considered to be between 3.0% and 5.0%. Still, the Fed determined that economic uncertainty justified the three small rate cuts.

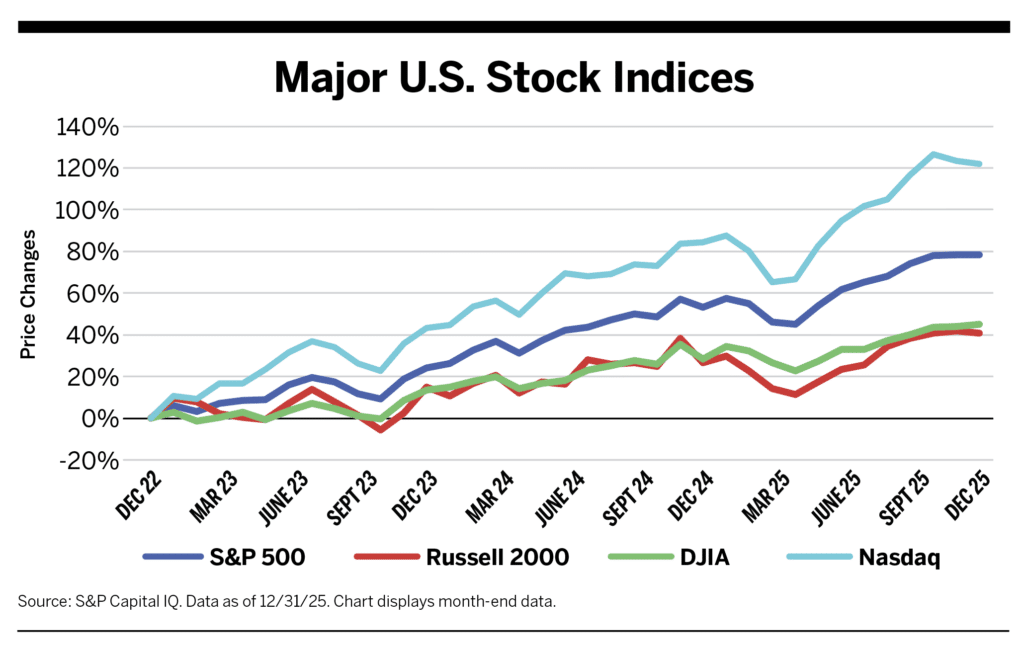

Equity Markets Continue Growth

The four major U.S. stock indices—the S&P 500, Dow Jones Industrial Average (DJIA), Nasdaq composite, and Russell 2000—each reached multiple all-time highs in 2025. On the year, all rose by double-digit rates: 20.4% for the Nasdaq, 16.4% for the S&P 500, 13.0% for the DJIA, and 11.3% for the Russell 2000. This was the third consecutive year of gains following declines in 2022.

However, a relatively small group of large-cap technology companies, particularly those with significant exposure to artificial intelligence, continued to account for a disproportionate share of index returns. Market participation outside of these leaders improved modestly but remained uneven.

P&C Market Profitable

The U.S. property and casualty (P&C) sector’s financial performance improved markedly in 2025. The sector recorded $34.9 billion in net underwriting gain for the first nine months of 2025, according to AM Best—up significantly from a $3.7 billion gain reported for the same period of 2024. (Full-year 2025 data was not available at press time.)

This performance reflects continued growth in premiums written, improved loss ratios across several major lines, moderating catastrophe losses, and sustained underwriting discipline— particularly within personal lines, where loss experience and pricing actions taken in prior periods have supported profitability. Additionally, insurance companies’ surplus—the difference between assets and liabilities—stood at $1.2 trillion through the first three quarters of 2025, further highlighting the industry’s financial strength.

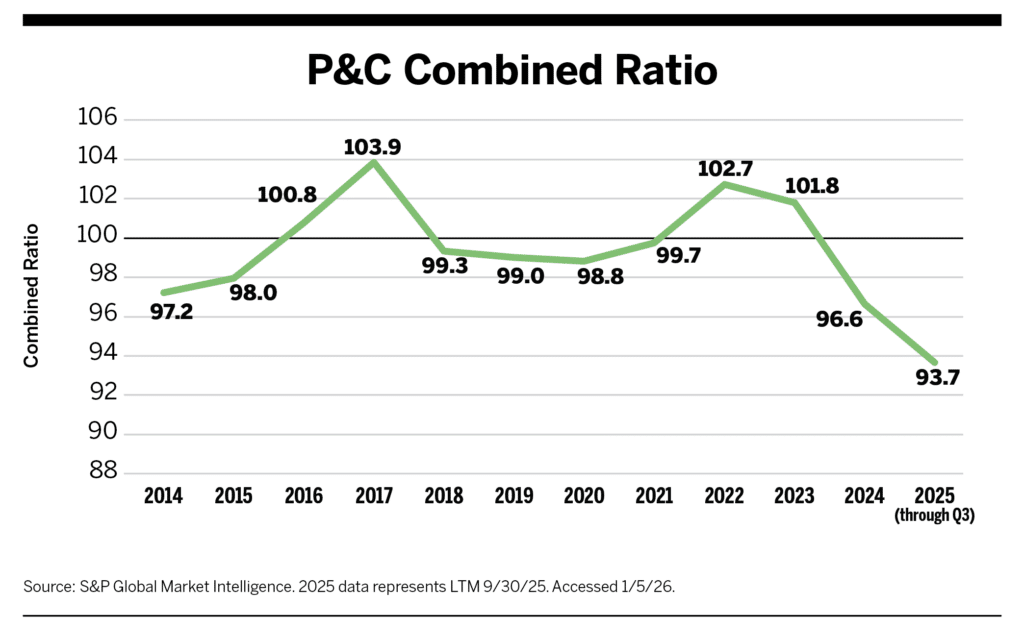

Underwriting Profits Rise

The P&C combined ratio recorded underwriting losses in 2022 and 2023, as catastrophes drove unprofitability. Underwriting profits improved in 2024 to register a combined ratio of 96.6. Through the first three quarters of 2025, the P&C combined ratio improved even further, with preliminary results indicating 93.7.

While strong underwriting profitability can mean more profit-sharing for brokers, it also often grants greater pricing flexibility to carriers, which could limit the need for significant rate increases. MarshBerry’s data indicates that brokers generally have benefited from rising premiums, with organic growth rates in recent years registering near record highs despite low sales velocity. Consequently, as rate changes enter soft territory, industry organic growth rates are expected to slow in the aggregate.

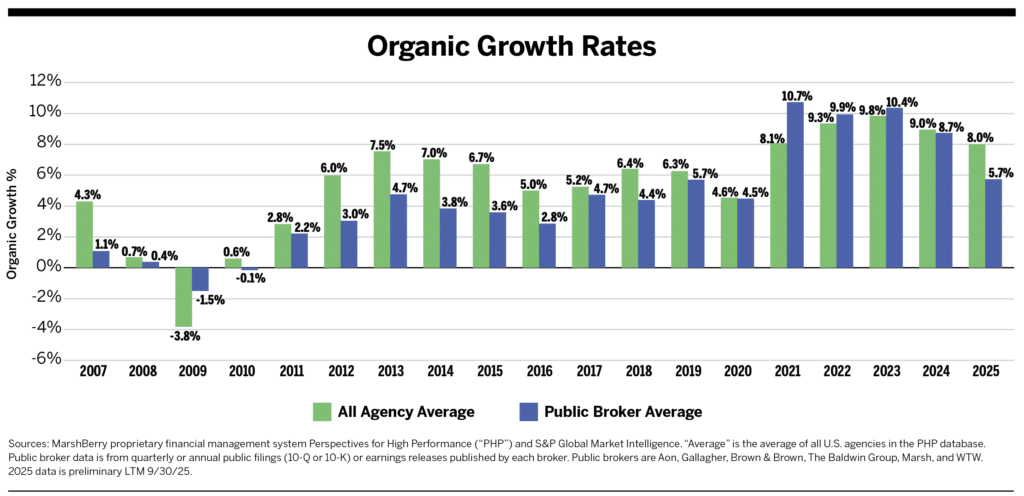

Organic Growth Slows

While total written P&C premiums rose to a new high in 2025, organic growth rates for both public and independent brokers declined from levels in the prior four years. Organic growth for independent brokers, however, appears to be holding on to higher levels than for public brokers.

Average organic growth for public brokers fell from 8.7% in 2024 to 5.7% in 2025, while the average for all firms dipped from 9.0% to 8.0% year over year.

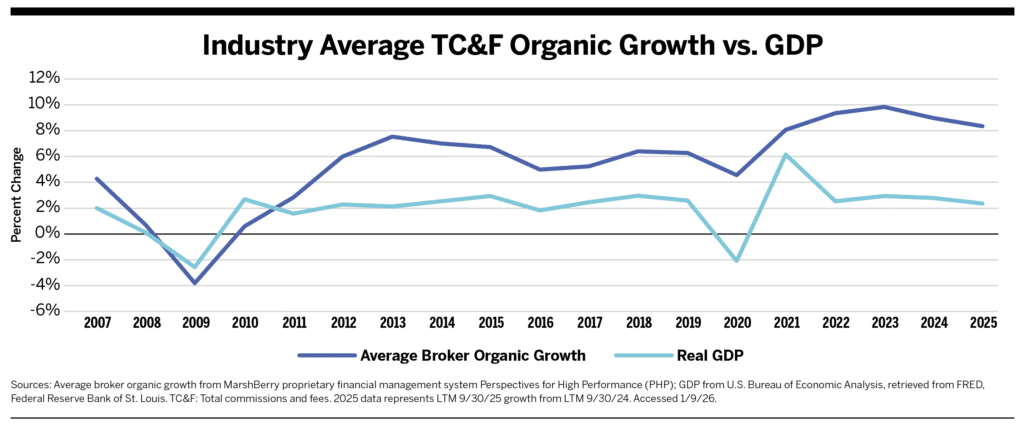

Organic growth often tracks GDP growth. However, in recent years, the hard market supported elevated broker organic growth despite more moderate GDP increases. Insurance rates softened in 2025 to a point where many lines are now considered to be in a soft market.

Commercial P&C premiums rose by just 0.2%, on average, across all account sizes in the fourth quarter, according to The Council’s P/C Market Survey. That was down from 4.2%, 3.7%, and 1.6% in the first three quarters of the year.

Alongside the minimal overall commercial P&C premium growth in the fourth quarter, The Council’s survey showed many lines recorded declines, including directors and officers liability (-3.8%), cyber (-3.3%), employment practices (-2.6%), and business interruption (-0.7%).

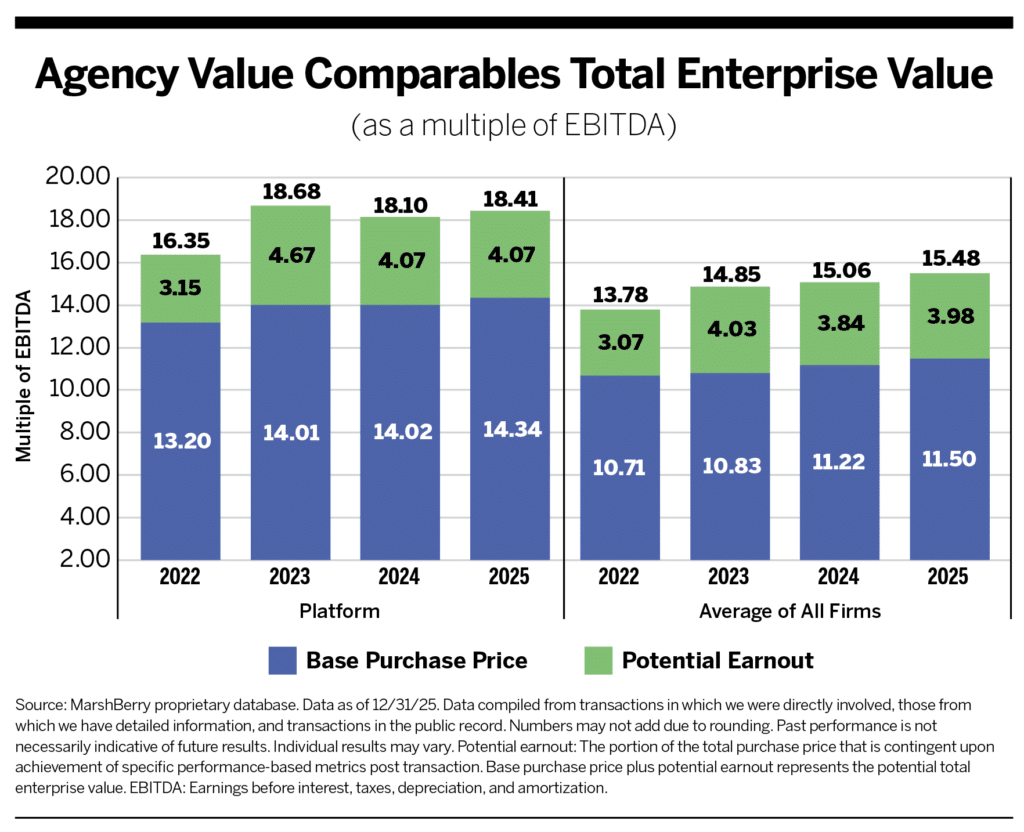

Valuations Remain Strong for High-Performing Firms

Even with the shifting economic environment and softening P&C market, brokerage average and platform valuations in 2025 stayed elevated. Valuations as a multiple of EBITDA (earnings before interest, taxes, depreciation, and amortization) on an upfront base purchase price ending Q4 2025 averaged 11.50x across all firms, with a potential total enterprise value up to 15.48x when achieving maximum earnout. Platform firm valuation multiples ending Q4 2025 averaged 14.34x on an upfront base purchase price, with a potential total enterprise value up to 18.41x when achieving maximum earnout.

Despite these record multiples, expect continued pressure on valuations for firms that cannot generate organic growth outside of rate or exposure base expansion. Firms that generate sales velocity in the mid to high teens should still command aggressive valuations as buyers look for ways to enhance their own organic growth metrics.

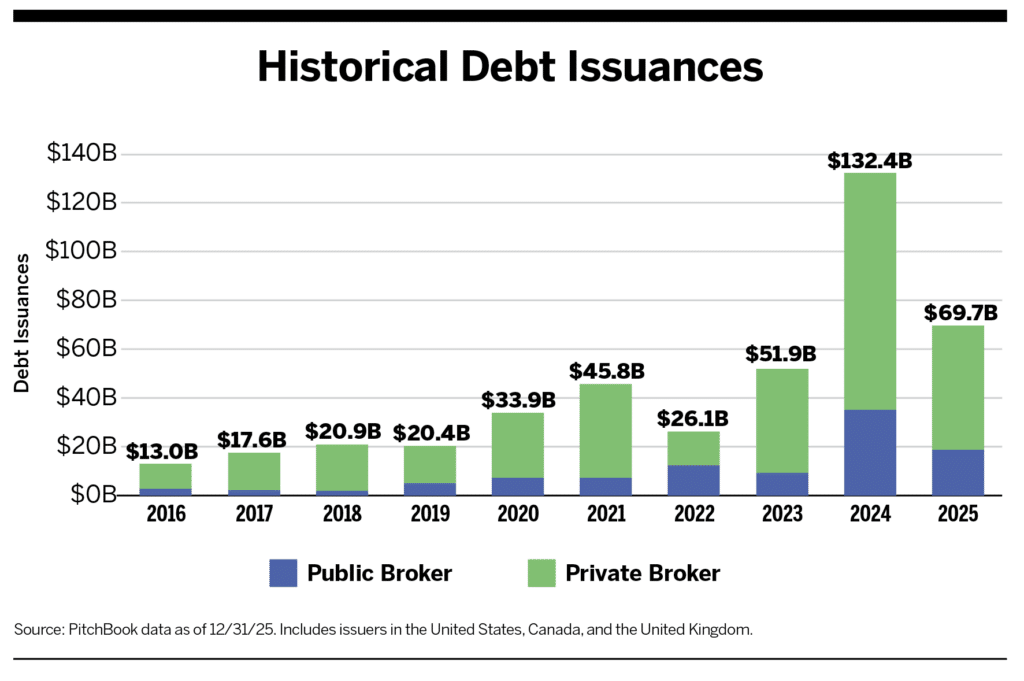

Brokerages Moderate Debt Raising

In 2025, total institutional debt issuance moderated to $69.7 billion following 2024’s record $132.4 billion haul, yet activity remained well above historical norms. Private brokers still account for most issuance (73% in 2025), though public broker participation increased meaningfully year over year.

The pullback appears more cyclical than structural. According to PitchBook, “refinancing” represented the largest share of 2025 volume at $24.4 billion, followed by “acquisition-related financing” at $17.4 billion, underscoring that M&A remains a central driver of capital demand. “General corporate purposes” and “recapitalizations” also comprised a meaningful portion of issuance.

Meanwhile, leverage ratios across the industry have steadily compressed from peak 2021 levels. As spreads tighten further and lenders remain constrictive on the sector, improving balance sheet flexibility and disciplined leverage profiles should position buyers to reaccelerate acquisition activity in 2026.

2025 Insurance Brokerage M&A Review

In 2025, there were 854 announced insurance brokerage transactions in the United States, according to MarshBerry data. This deal count represents a 0.8% increase from 2024, becoming the third-most-active year on record.

Who’s Buying?

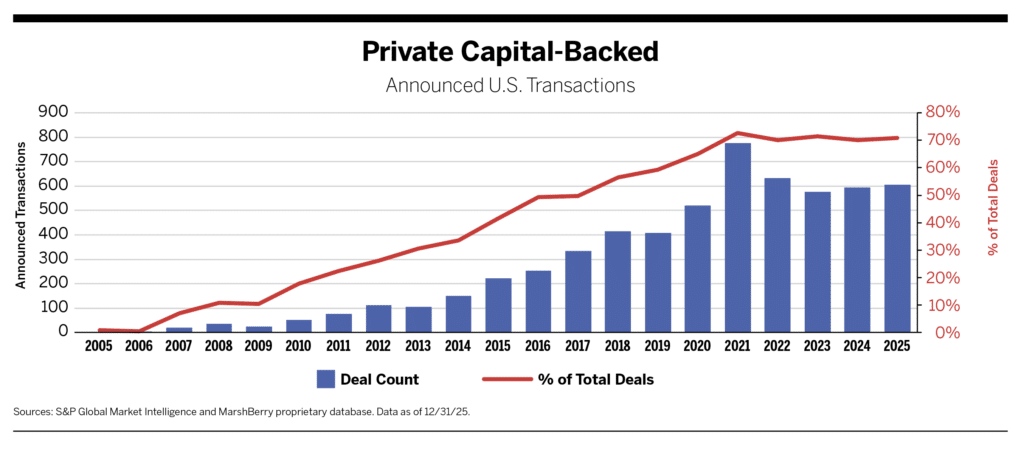

Private capital-backed buyers accounted for 605 of the 854 transactions (70.8%) in 2025, sustaining their multiyear dominance of the insurance distribution M&A market. These buyers’ deal count increased by a compound annual growth rate (CAGR) of 6.7% from 2019 to 2025.

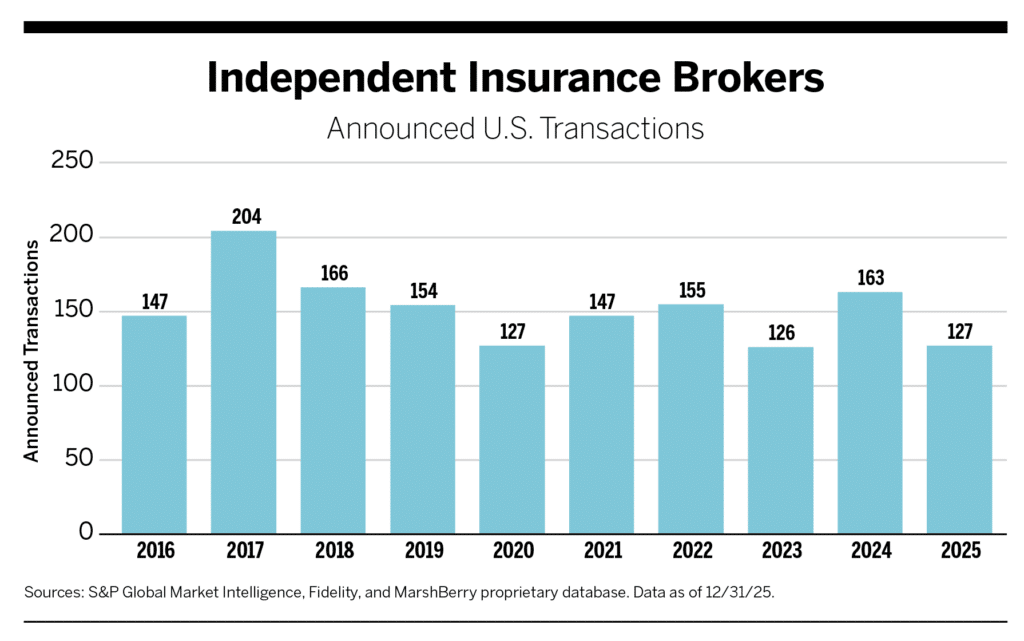

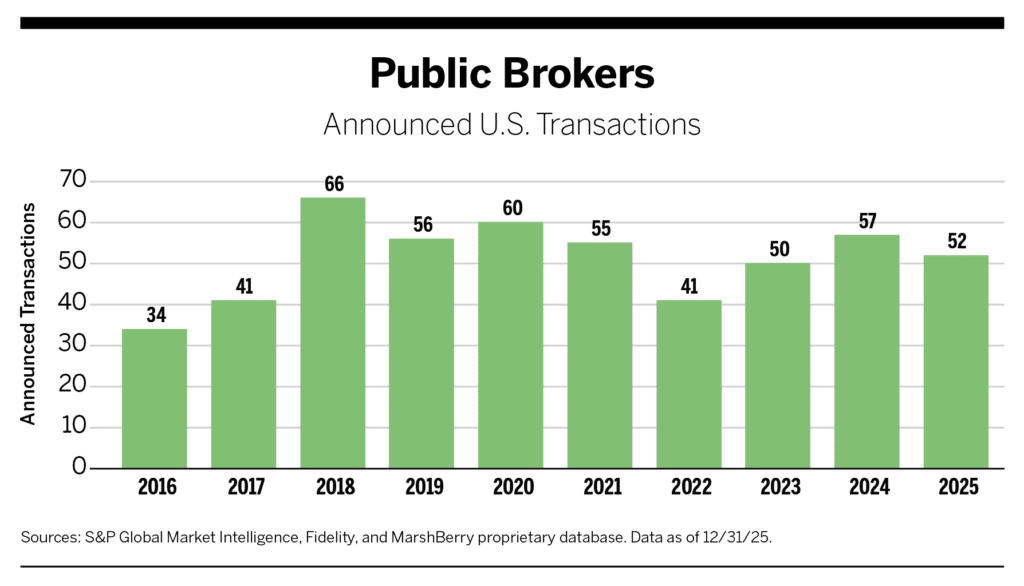

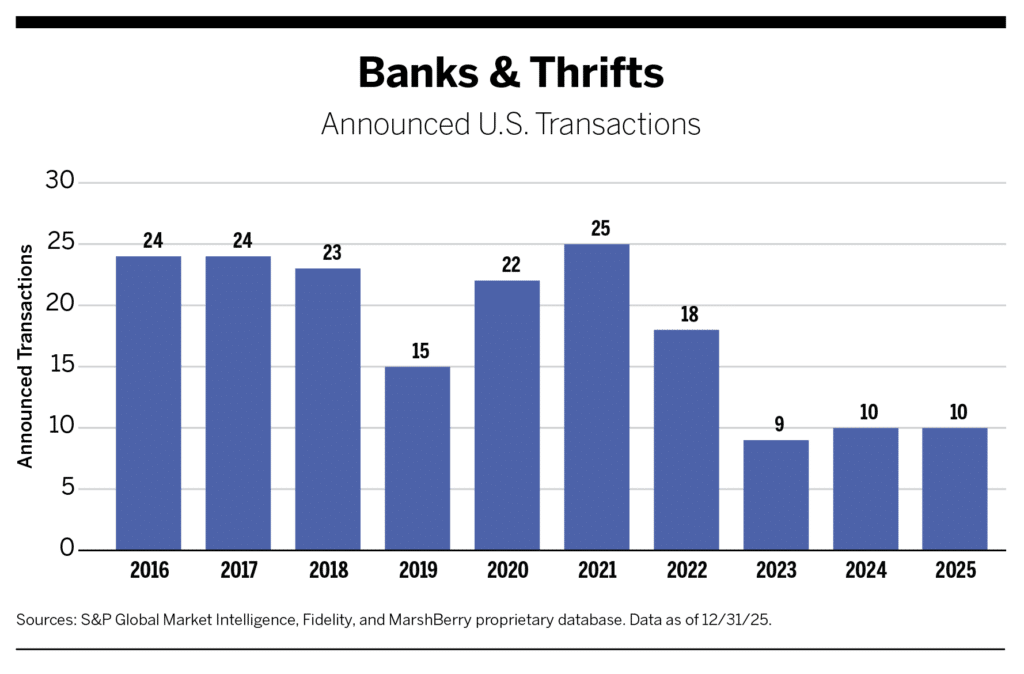

Independent agencies were buyers in 127 deals, representing 14.9% of the market, down from 163 transactions announced in 2024 (for 19.2% of the market). Public brokerages announced 52 deals, roughly 6.1% of the total transaction count (versus 6.7% in 2024). There were 10 announced transactions by bank buyers in 2025, matching the 2024 number.

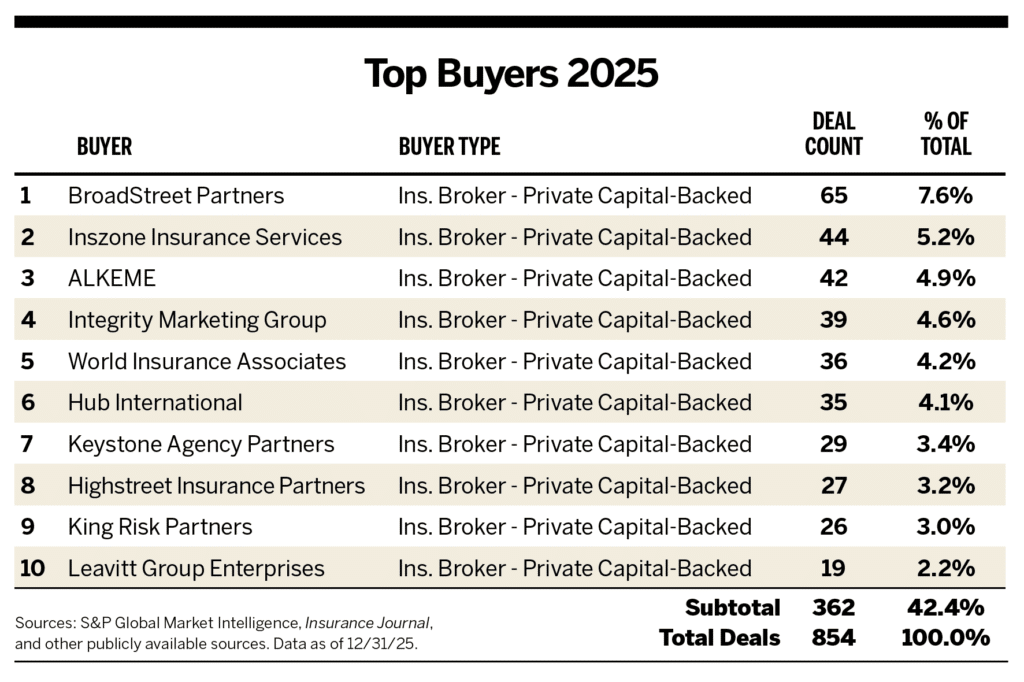

For the third consecutive year, the two most active U.S. buyers, based on deals announced, were BroadStreet Partners (with 65 deals) and Inszone Insurance Services (with 44). ALKEME ranked No. 3 with 42 deals, more than doubling the 20 that earned the brokerage the No. 10 position in 2024. The top three buyers’ 151 transactions accounted for 17.7% of the total in 2025, while the 10 most active buyers completed 362 (42.4% of the 854 deals).

Private Capital-Backed Buyers Remain Most Active

Private capital-backed buyers in 2025 included 63 unique insurance brokerages, plus 27 “other” types of capital-backed buyers, such as investment firms and private capital-backed companies in other industries. That was a notable increase from the 47 unique brokerages and 12 “other” capital-backed buyers from 2024, but still a relatively small concentration compared to the total number of transactions.

While private capital-backed buyers continued to account for the largest share of acquisition activity in 2025, more firms entered or reentered the acquisition landscape during the year. Several notable trends included:

- BroadStreet Partners led all buyers for the third consecutive year, accounting for nearly 8% of U.S. dealmaking alone, despite completing fewer deals than its 76 in 2024.

- 19 private capital-backed buyers completed more than 10 transactions in 2025, modestly below the 21 buyers that reached that threshold in both 2023 and 2024.

- Among the 63 unique private capital-backed insurance brokerage buyers active in 2025, 30 increased their acquisition activity from 2024, while 24 reduced activity and nine maintained a consistent pace.

- A total of 194 unique buyers announced completed transactions in 2025, a meaningful increase from 153 buyers in 2024 and 169 in 2023. In addition, 77 firms completed two or more acquisitions during the year, up slightly from 73 buyers in 2024 and 68 in 2023.

A Down Year for Independent Firms

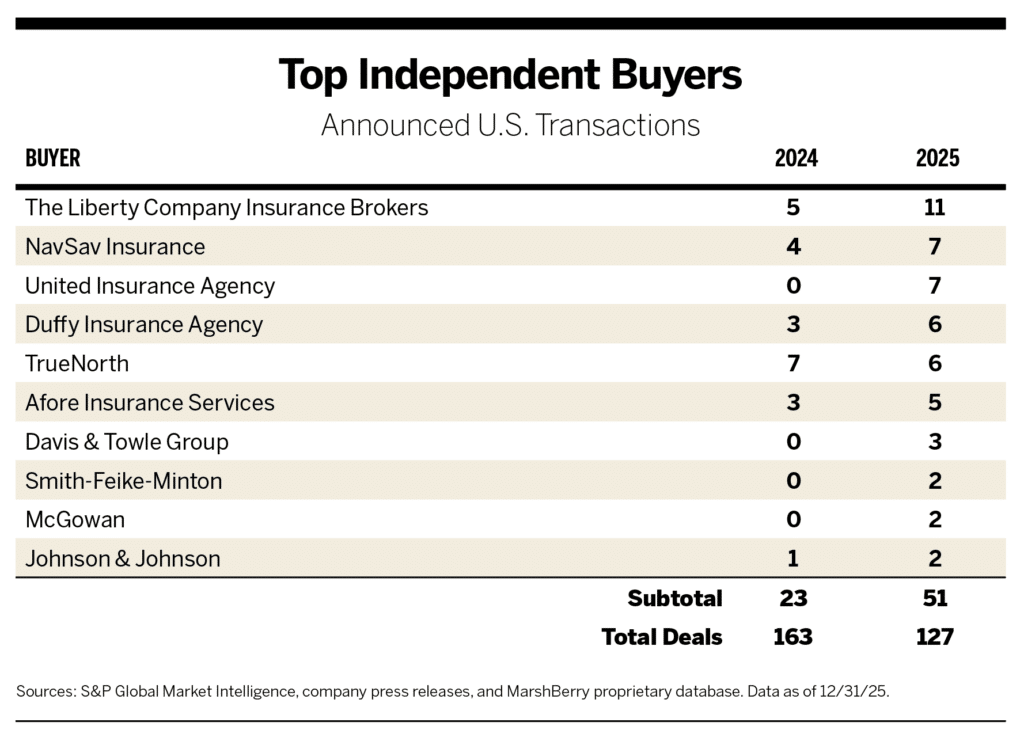

Independent firms accounted for 127 (or 14.9%) of the total deal count in 2025, down from 19.2% market share and 163 transactions in 2024. Sixty-nine distinct independent firms without known private capital backing announced transactions in 2025, equaling the 2024 number.

Ten of those independent buyers accounted for 51 of the 127 deals (or 40.2%), while 14 (or 20.3%) also completed a transaction in 2024. That deal share was down from 50.3% in 2024, driven in part by notable independent firms completing capital transactions that year, including Leavitt Group’s sale of a stake to Capital Z Partners and TWFG Insurance Services’ initial public offering (IPO).

Public Brokerages Keep Focus on Acquisitions

Public brokerages announced 52 deals during 2025, roughly 6.1% of the total transaction count (versus 6.7% in 2024). Here’s how the public brokers fared.

- Gallagher was the most active public buyer, announcing 16 transactions, representing 30.8% of public brokerage deal activity in 2025.

- Marsh completed nine acquisitions, a slight decrease from 10 in 2024.

- Aon, including subsidiary NFP, announced six U.S. acquisitions for the year, down from nine in 2024.

- TWFG Insurance announced six U.S. acquisitions in 2025 after reporting no transactions in 2024, the year of its IPO.

- Brown & Brown completed six U.S. transactions, slightly below its seven acquisitions in 2024.

- Ryan Specialty announced three U.S. acquisitions, compared to five transactions in 2024.

- WTW completed three U.S. acquisitions in 2025 after announcing none the year before.

- The Baldwin Group announced two U.S. deals, including the acquisition of CAC Group (announced Dec. 2, 2025; closed Jan. 2, 2026), after completing no transactions in 2024.

- Steadfast Group, a publicly traded Australian insurance brokerage, announced one U.S. acquisition in 2025 with its purchase of Novum Underwriting Partners, an Ohio-based managing general agency and wholesale brokerage.

Banks Maintain M&A Pullback

Bank-owned agency buyer activity remained subdued, extending a long-term decline in bank participation in insurance brokerage M&A. The 10 deals from this group in both 2025 and 2024 are just one acquisition above 2023 and nearly half the count from 2022. In 2006, bank acquisitions accounted for 24.5% of total announced insurance brokerage transactions. That share declined to 4.7% by 2016 and to just 1.2% of total deals in 2025.

This trend is expected to persist, as banks face structural disadvantages when competing with private capital-backed buyers, including lower acquisition leverage tolerance, more restrictive regulatory oversight, and balance sheet constraints following the regional bank disruptions in early 2023. As banks divest their insurance operations, it will logically eventually reduce the number of bank-owned firms in the market for acquisitions.

U.S. Buyers Crossing Borders

While U.S.-based insurance brokers remain focused on international expansion, overseas acquisition activity moderated in 2025 for the second consecutive year. U.S. buyers completed 32 European transactions during the year, down from 55 in 2024 and 66 in 2023, marking a continued pullback from peak international deal volume. Still, European activity is above 2021 levels, when U.S. buyers completed 23 transactions, suggesting that international M&A remains a strategic priority, albeit at a more measured pace.

A small group of large, well-capitalized platforms led international dealmaking. Gallagher headed all U.S. buyers with 15 transactions outside of North America, followed by Brown & Brown and Acrisure with six transactions each. Marsh completed three acquisitions, while Aon announced two transactions during the year.

What’s Being Bought?

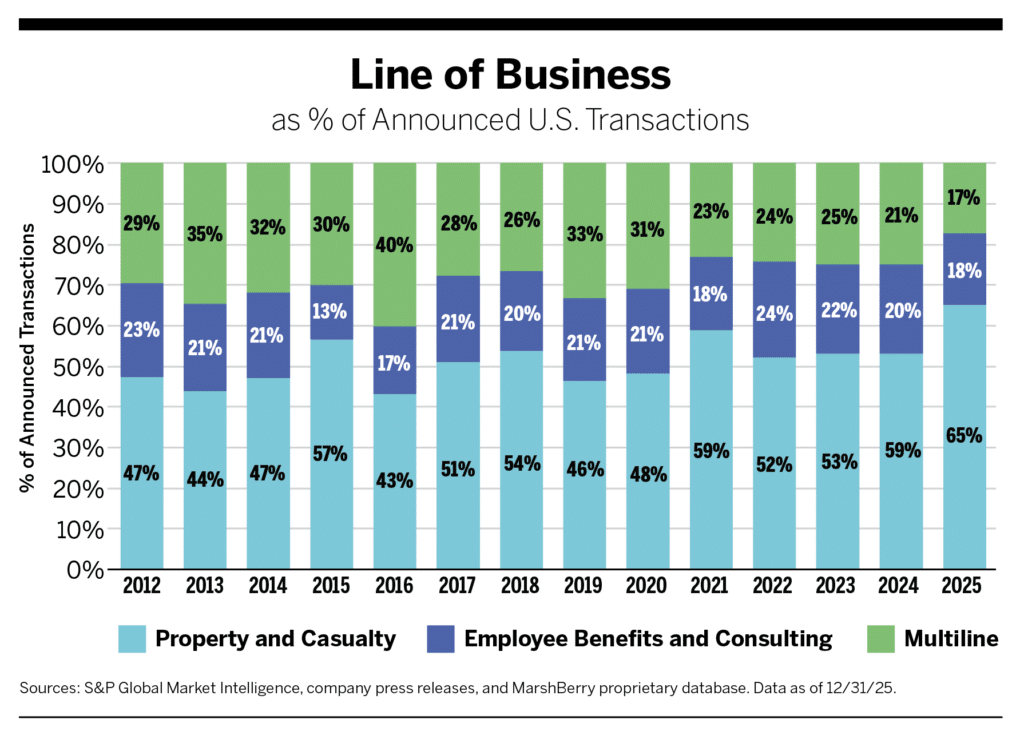

P&C brokers accounted for 558 announced deals in 2025, or 65% of total activity, up from 497 P&C transactions (59%) in 2024. Employee benefits and consulting brokers accounted for 18% of total transactions in 2025, down from 20% in 2024. Multiline brokers represented 17% of the market, declining from 21% in the prior year.

Specialty transactions totaled 149 deals in 2025, representing 17.4% of market activity. This marked a 24.2% increase from 120 specialty transactions recorded in 2024, although activity remained below the elevated levels observed from 2021 through 2023.

10 Most Notable Transactions in 2025

While definitions of “notable” will vary, here we’re focusing on the amount of capital deployed in a deal as well as companies that significantly expanded their geographic reach with a deal.

- Feb. 3: Ryan Specialty acquired Velocity Risk Underwriters, a Nashville-based MGU specializing in catastrophe-exposed property risks. Velocity covers perils such as hurricanes, earthquakes, tornadoes, and hail, focusing on small to midsize commercial businesses. The $525 million transaction strengthens Ryan Specialty’s underwriting capabilities in property catastrophe coverage. As part of the transactions, Velocity’s wholly owned excess and surplus (E&S) carrier, Velocity Specialty Insurance, was acquired separately by FM, a leading commercial property mutual insurer.

- April 10: Gallagher completed its $1.2 billion acquisition of Woodruff Sawyer, adding a well-established middle- and large-market brokerage to its U.S. retail property and casualty platform. The business generated approximately $268 million of pro forma revenue and $88 million of adjusted earnings in 2024, reflecting valuation multiples consistent with recent large brokerage transactions. The acquisition expands Gallagher’s footprint on the U.S. West Coast and deepens its capabilities in targeted industry segments.

- May 12: Hub International secured a $1.6 billion minority equity investment led by T. Rowe Price, Alpha Wave Global, and Temasek, valuing the firm at $29 billion. The investment follows a series of valuation increases since Hellman & Friedman’s initial investment in 2013. The capital will support Hub’s growth strategy, including M&A, technology investment, and debt reduction. H&F remains the controlling shareholder, with Altas Partners and Leonard Green staying on as minority investors.

- May 20: Acrisure announced a $2.1 billion capital raise through issuance of new convertible senior preferred stock, led by Bain Capital. Other participants included Fidelity, Apollo Funds, Gallatin Point Capital, and BDT & MSD Partners. No existing investors exited, and BDT & MSD remains Acrisure’s largest minority shareholder. Proceeds from the raise will be used to refinance existing nonconvertible preferred stock, pursue strategic M&A, and accelerate Acrisure’s evolution as a tech-enabled financial services platform.

- June 10: Brown & Brown acquired Accession Risk Management Group, the parent company of Risk Strategies and One80 Intermediaries and the ninth-largest privately held brokerage in the United States, for $9.8 billion. The purchase price reflects an approximately 12x EBITDA multiple, including expected synergies, but the headline number without synergies is about 16.4x EBITDA. Accession reported $1.7 billion in pro forma revenue with an estimated roughly $600 million in pro forma adjusted EBITDA.

- July 16: Keystone Agency Partners announced that Warburg Pincus had acquired a majority stake in the firm, with Bain Capital retaining a minority interest through a new investment from Bain Capital Insurance. Launched in 1983, Keystone is among the largest insurance brokerage and agency networks in the United States, with 28 platform partners, over 350 network agencies, and more than $8 billion in premium volume.

- Sept. 19: OneDigital secured a majority investment from Stone Point Capital and the Canada Pension Plan Investment Board, valuing the integrated insurance, financial services, and workforce consulting platform at more than $7 billion. Founded 25 years ago, OneDigital has built a diversified national platform spanning employee benefits and HR, retirement and wealth management, property and casualty, PEO services, and Medicare Advantage. The investment involves the purchase of ownership from existing shareholders, while Onex Partners retains a meaningful minority stake following its initial investment in 2020.

- Oct. 28: Ryan Specialty acquired Stewart Specialty Risk Underwriting (SSRU), a Toronto-based MGU specializing in large-account, high-hazard property and casualty risks. SSRU joined Ryan Specialty Underwriting Managers, expanding the company’s presence in Canada and significantly increasing its total addressable market.

- Dec. 1: Marsh acquired Honolulu-based insurance brokerages Atlas Insurance Agency, Pyramid Insurance Centre, and IC International from Tradewind Group. The acquisition significantly strengthens Marsh’s presence in Hawaii, expanding its capabilities in commercial, personal, and employee benefits insurance, with industry specializations in municipalities, transportation, and hospitality.

- Dec. 2: The Baldwin Group announced its acquisition of CAC Group, a nationally recognized specialty and middle-market insurance brokerage firm ranked 35th in Business Insurance’s 2025 rankings. The deal will create one of the largest independent insurance advisory and distribution platforms in the United States.

Specialty Market Supply Stays Tight

For the second year in a row, deal volume in the specialty insurance M&A market remained characterized by low supply of quality acquisition targets. This ongoing imbalance between supply and demand has been driven by heavy consolidation paired with robust interest from a growing buyer community.

There were 149 announced specialty firm M&A transactions in 2025, a 24% increase from 120 deals announced in 2024. However, this is still off the highs from 2021 to 2023.

Strong M&A increases in the specialty market over the past decade have been fueled by significant premium growth within the surplus lines and delegated authority markets. This growth has driven rampant consolidation in the sector as buyers, with access to investment capital, seek to create more value and economies of scale. The major ancillary benefits for buyers are additional market clout and diversification of what tend to be highly concentrated businesses when an independent organization sells to larger organizations.

In 2009, there were approximately five specialty firms with $1 billion or more in P&C premium. By 2025, that number had exploded to over 27 firms, of which seven have at least $5 billion in P&C premium and the top three each over $25 billion. Currently, MarshBerry estimates these firms collectively place over three-quarters of specialty P&C premium in the U.S. marketplace.

The Most Active Specialty Firm Buyers

- Integrity Marketing Group made 38 specialty deals and led the specialty buyer leaderboard for the fifth consecutive year. IMG is focused on the life and health sector.

- AmeriLife Group recorded seven transactions in 2025, following seven transactions in the prior year. AmeriLife is also focused on the life and health sector.

- Brown & Brown, through specialty division Arrowhead Specialty, recorded five transactions.

- Amwins completed four transactions in 2025 after completing the same number in 2024.

- Balance Partners also completed four transactions for the year, marking its formal entry into the M&A market following a strategic investment from BV Investment Partners in 2024. The firm first acquired Vanguard Specialty in March, a transaction in which MarshBerry advised Vanguard.

- Tokio Marine, Ryan Specialty, The Amynta Group, OneDigital, and Brightstone all completed three transactions in 2025.

Large Retail Brokers Stay Interested in Specialty

Large broker platforms continued to invest in the specialty space in 2025. All top 10 firms (and 15 of the top 20) have specialty platforms, and every top 20 firm has previously acquired specialty businesses. These firms are interested in specialty operators’ high-growth and niche operations.

Large retail brokers are also pursuing specialty firms’ rising premium volume and increasing P&C market share. Specialty firms have gone from placing approximately 8.5% of overall premium in 2010 to over 21% in 2025, per MarshBerry’s estimates. As such, specialty premium (i.e., E&S and delegated authority) has grown at a multiyear CAGR that is three times that of the non-delegated authority admitted market premium over the last decade.

Specialty Firm Valuations Remain High

Even with the high cost of capital, the continued demand and low seller supply drove up specialty firm valuations to all-time highs. This is unlikely to change, as top performers continue to command impressive multiples.

Among specialty firms represented by MarshBerry, valuations as a multiple of EBITDA averaged 13.89x in upfront consideration last year. This population averaged a 19.42x multiple when contemplating the total all-in valuation after post-close growth incentives (e.g., earnouts). All-in valuations of specialty firms increased by over 60% from 2020 to 2025, which speaks to the heightened investor demand.

Specialty Market Outlook for 2026

While market and economic conditions could become more challenging, potentially lessening acquisition appetite and/or availability of capital (debt and equity), for now demand remains robust for specialty firms. Consolidation of the specialty marketplace is likely to persist this year, with private capital-backed buyers maintaining a large presence. Valuations should remain near historic highs amid a limited supply of quality sellers in a sector with historically strong and consistent growth. However, all eyes will be on the changing rate environment and whether it will materially influence growth trends and M&A activity.

Wealth Advisory M&A Breaks Out

The wealth advisory M&A market accelerated meaningfully in 2025, delivering a record-high 394 announced deals in 2025, rising 11.6% from 353 transactions in 2024. This growth came absent a single defining catalyst or macroeconomic influence. Instead, momentum was carried forward by a market that has grown up.

Compared to prior cycles, this period of activity reflects a more mature buyer base and a far more sophisticated seller mindset. Capital still matters, but how it is deployed matters more. Private capital has helped professionalize the market, pushing buyers to sharpen their investment theses, build real integration capabilities, and focus on long-term value creation rather than short-term expansion. M&A is no longer opportunistic. It has become a core strategic lever for scale, specialization, and relevance.

Private capital-backed buyers represented the largest share of wealth advisory deals in 2025. They are drawn by the sector’s strong and consistent business retention rates, opportunities for operational efficiencies, and, most crucially, recurring and predictable revenue.

Private capital-backed buyers’ portion of overall deals rose from 52% in 2020 to 73% in 2025. This shift is partly attributed to a nearly equivalent decline in public buyers. The shift from public to private backing was mainly driven by wealth advisory firms’ need to be more competitive in the marketplace, as privately backed firms can focus more on long-term growth than quarterly growth.

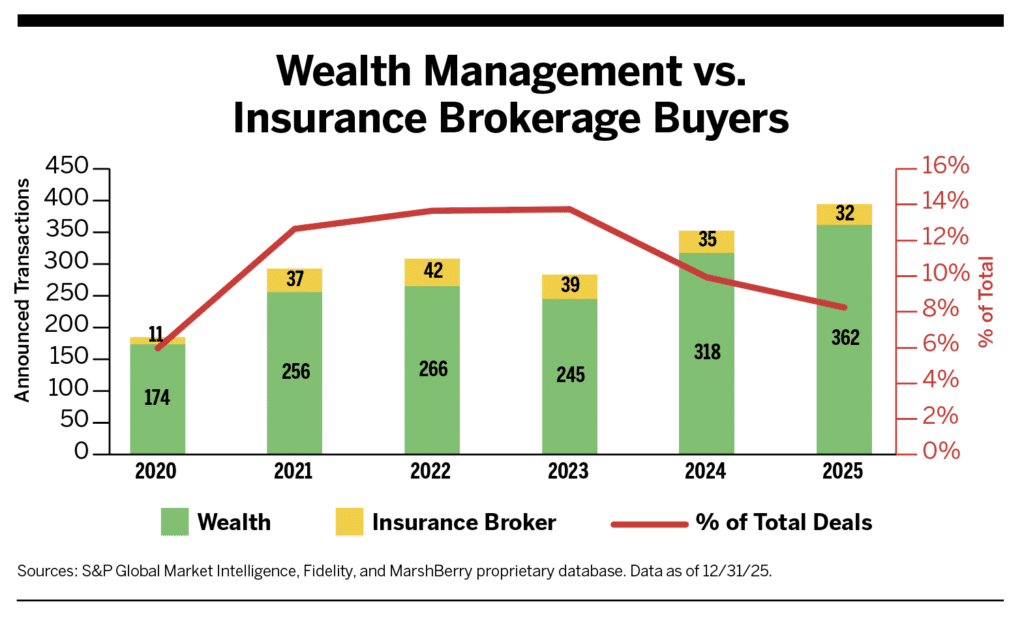

The number of wealth advisory transactions involving insurance brokerages declined from 35 in 2024 to 32 last year, falling from 9.9% to 8.1% of the total deal count.

Twenty-five of those 2025 transactions (78% of the total) were for firms that provide wealth advisory services, a shift from the historical range of 40%–60% from 2021 to 2023 but in line with the 77% from 2024. Traditionally, insurance brokerage firms led with retirement plan businesses and viewed wealth as a complimentary feature of the deal. However, as these brokerages have built out their wealth platforms, they have become increasingly comfortable targeting firms with wealth advisory businesses.

The Most Active Wealth Firm Buyers

- MAI Capital Management (EPIC Insurance Brokers) and Hub International each added seven firms, with Hub acquiring two retirement firms and five wealth firms and MAI acquiring seven wealth firms.

- OneDigital made four acquisitions in 2025—two retirement planning firms and two wealth advisory firms.

- Simplicity Group closed three deals, all for wealth advisory firms.

- Other noteworthy acquirers were World Insurance, Heffernan Insurance, and Alera Group with two acquisitions each and public brokers Aon, Gallagher, and Marsh with one each.

Wealth Advisory M&A Outlook

The wealth advisory M&A market enters 2026 with sustained momentum. Valuations remain strong, and the depth and quality of the buyer universe supports activity. Well-capitalized acquirers are still leaning in, providing real optionality for firm owners and confidence in the near-term dealmaking environment.

That said, valuation environments are cyclical, as market conditions, innovation cycles, and competitive dynamics can change quickly. Many firms are reaching an inflection point where success driven by founder energy, favorable tailwinds, and entrepreneurial execution is in the rearview mirror. The next phase of growth will require different capabilities, deeper infrastructure, and sustained investment.

One key trend to watch for involves young high-growth business owners seeking partnerships. These business owners, once inclined to stay independent, are now exploring partnerships as consolidation accelerates. High-growth firms see strategic alliances as a means to capture market share faster and with less risk, leveraging the capital and expertise of private capital-backed partners.

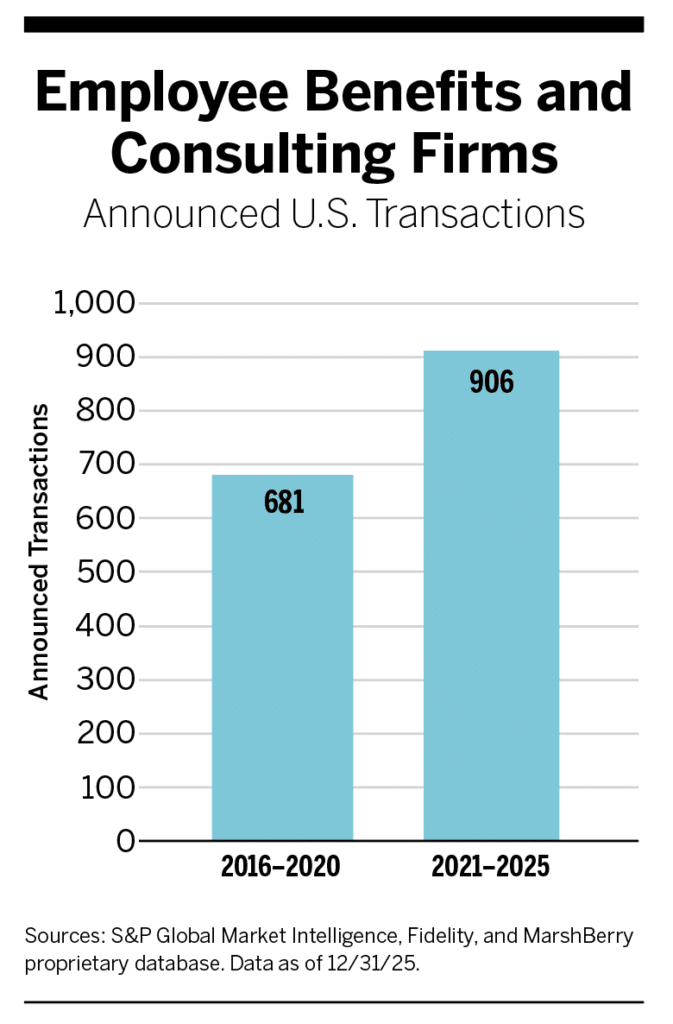

Consolidation Persists in Employee Benefits and Consulting

Since 2016, there have been 1,587 publicly announced insurance brokerage transactions in which the seller was an employee benefits (EB) and consulting firm. There were 906 transactions from 2021 to 2025, a steep climb from 681 total reported deals from 2016 to 2020. Although deal counts have declined in the last two years, MarshBerry believes this isn’t a reflection of interest in the EB space, but rather representative of the lack of available EB-only firms.

As employers’ benefits needs evolve, brokers have had to invest in the resources to serve them and stay competitive. Alongside these upgrades, EB valuations continue to increase, driving a large amount of consolidation within the space.

The 152 announced EB and consulting firm M&A deals in 2025 represented roughly 18% of all insurance brokerage transactions. And while the number of deals for EB-only firms hovers around 150 per year, EB revenue was a large part of the publicly announced top 100 broker transactions over the past two years.

An analysis of the top 100 insurance brokerages deals by revenue shows a sharp increase in EB revenue embedded within large, multiline transactions involving large, diversified brokerages with significant employee benefits operations. The percentage of EB revenue as part of the acquired revenue from deals in the top 100 went from 0.4% in 2021 to 8.0% in 2025—highlighting a clear shift in where EB value is being transacted.

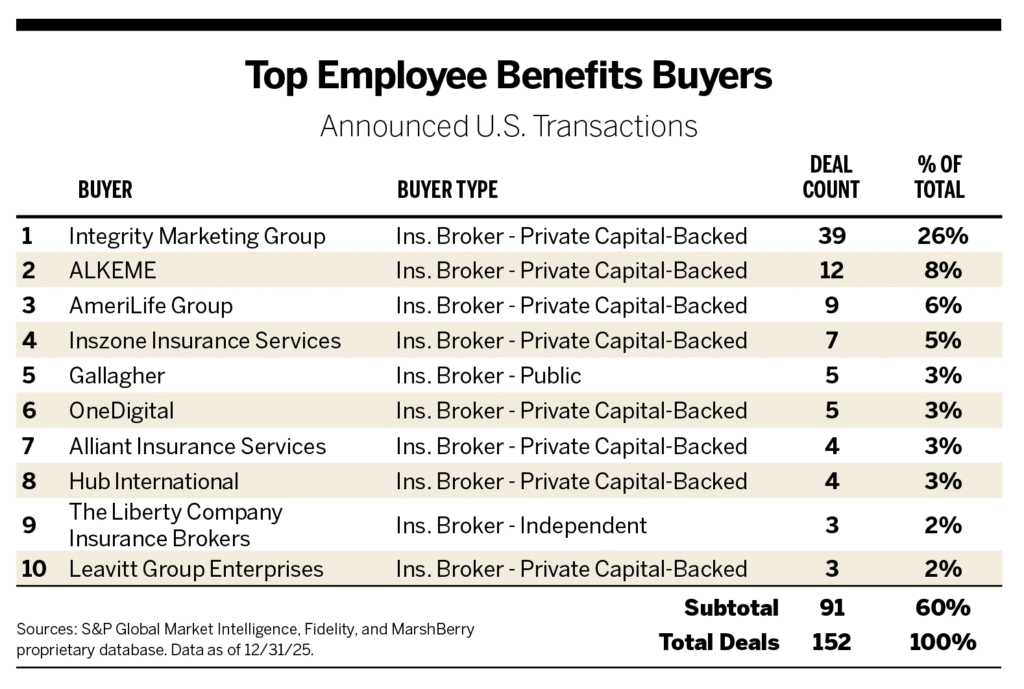

EB Firm Top Buyers

In 2025, the top 10 buyers of EB firms represented 59.9% of total transactions, compared to 58.2% in 2024. They were led by Integrity Marketing Group, which announced 39 deals for EB firms for the year, up from 30 in 2024. Integrity Marketing Group and No. 3 buyer AmeriLife Group, which together executed 48 deals in 2025, are focusing on the individual market, whereas most other active acquirers target employer-sponsored medical and ancillary benefits services.

EB M&A Outlook

Most active buyers have made considerable investments in the EB and consulting space and remain confident in the long-term sustainability of the brokerage and advisory model. In the near term, the primary challenge for active EB acquirers is the limited availability of quality, scaled platforms coming to market. As the competitive landscape evolves and larger, well-capitalized firms continue to invest in technology, talent, and specialization, independent firms face increasing pressure to scale thoughtfully and differentiate their value proposition.

While EB inventory is expected to remain constrained, it’s still a valuable space with an abundance of buyers prepared to invest capital in high-quality independent firms, particularly those evaluating ownership transition options. Overall, market signals indicate sustained and growing interest in the EB space.

A New Phase for the European Market

European insurance distribution M&A is increasingly playing out on different timelines by market, driven by local consolidation maturity, regulation, and the depth of buyer platforms. Momentum in the United Kingdom, long seen as the most transparent bellwether, cooled materially in 2025. Across continental Europe, the picture is more varied: dealmaking in Iberia, Italy, and parts of Central and Eastern Europe is accelerating as professionalization, succession, and compliance investment bring more owners to market, while several Northern and Western European markets remain broadly steady.

MarshBerry identified 531 announced M&A transactions involving European insurance brokers in 2025. The true total is likely higher, as many smaller deals go unreported and are therefore difficult to track comprehensively. This leaves 2025 slightly below the previous two years, when around 560 transactions were announced annually. Regionally, the most notable shifts were a roughly one-third reduction in the U.K. and Ireland deal count, to 115, and a near-doubling of transactions in Southern Europe, led by Spain, Portugal, and Italy.

Buyers Emphasize Strategic Fit

For several years, rising premium rates and higher commissions provided a steady uplift to broker revenues across many European markets. That tailwind has now moderated in numerous insurance lines, most notably commercial, reducing the level of automatic top-line growth. As a result, underlying performance is coming into sharper focus. Brokers with strong client retention, genuine organic growth, and a clear value proposition are pulling away in revenue, while weaker platforms are struggling to sustain momentum. Buyers are placing greater emphasis on strategic fit rather than pure scale.

Private capital has been a dominant force for the past few years in European M&A, but the playbook is shifting. Private capital is backing both established platforms and new consolidators across the continent, and there is no shortage of capital still looking for deployment. At the same time, the pool of scale targets is tightening in several markets, pushing more activity toward smaller add-ons and capability buys. A growing number of larger private capital-backed platforms are also moving into refinancing and exit windows, which puts secondary sales, selective trade exits, and, occasionally, renewed initial public offering talk back on the agenda for 2026.

U.K. M&A Enters a More Measured Phase

The U.K. insurance broking market remains the most mature and best capitalized in Europe, supported by a large domestic commercial lines base and its global role in specialty and wholesale business through Lloyd’s of London. After years of intense consolidation, the market has become more measured. In 2025, 99 U.K. insurance distribution transactions were announced, the lowest annual total since 2017 and well below peak levels of 151 in 2023 and 152 in 2024. Activity is now characterized by smaller, targeted acquisitions and selective platform investments rather than rapid-scale expansion, reflecting both limited availability of attractive midsize targets and a stronger focus on integration capacity, earnings quality, and long-term strategic fit.

Private capital-backed platforms continue to shape competitive dynamics, but with more disciplined acquisition strategies. Groups such as Ardonagh, Howden, JMG, PIB, and Seventeen remain active, primarily pursuing bolt-ons that deepen local density or add specialist capability. Large international brokers, including Marsh, Aon, WTW, and Gallagher, compete selectively for high-quality assets. Valuation discipline is firmly embedded, with greater scrutiny on organic growth and execution risk.

Continental Europe Still Hot

Consolidation of insurance brokers in Europe is no longer concentrated in the British Isles. In markets across the continent, the pressure is on. Here are some highlights:

- Germany, often described as Europe’s most promising market for broker consolidation, recorded 73 M&A transactions in 2025. This was broadly in line with the past three years, despite expectations for a meaningful increase.

- Austria continues to show higher relative momentum, with more than 43 announced transactions from 2023 to 2025, largely involving very small brokers and driven by a concentrated set of active platforms.

- Switzerland remains selective and specialist-oriented, with transactions typically aligned to targeted capability and regional density plays.

- France remains highly fragmented, with more than 90% of broking firms employing fewer than 10 people. MarshBerry recorded 39 announced French transactions in 2025. However, micro deals (under 1 million euros in revenue) in the French market are often not disclosed and can be difficult to track.

- Italy deal activity accelerated from 57 announced transactions in 2025 versus 20 the year before. This headline number still likely understates the true pace of consolidation, as many smaller, succession-driven tuck-ins remain private and under-reported.

- The Iberian market, which includes Spain and Portugal, is quickly emerging as one of Europe’s most attractive regions for insurance distribution M&A. Deal activity in Spain has remained high for several years, going from 21 announced deals in 2021 to 34 in 2025. Meanwhile in Portugal, the number of announced transactions tripled from five in 2024 to 15 in 2025.

- The Benelux region, encompassing the Netherlands, Belgium, and Luxembourg, remains one of continental Europe’s more investable insurance distribution consolidation arenas. In the Netherlands, there were 80 transactions in 2025, and the market is now firmly in a long-tail consolidation phase. Belgium recorded 27 transactions in 2025 and remains structurally under-consolidated, leaving a longer runway for platform build-out. Q4 2025 combined digital convergence with continued rollup momentum.

- The Nordic market recorded 28 announced transactions in 2025, down from 54 in the peak year of 2023. That slowdown reflects a shrinking pool of available acquisition targets, but also more disciplined buyers prioritizing proven organic growth, specialist capability, and strong execution over rapid rollups.

- Central and Eastern Europe picked up insurance distribution M&A in 2025, with 38 transactions versus 20 in 2024. The true total is likely higher given the prevalence of undisclosed micro deals that are difficult to track consistently.

Projected Trends for Europe in 2026

In many European markets, deal flow in 2026 is expected to remain steady but disciplined, with buyers focused on specialist capability additions and opportunities where scale genuinely improves service quality, compliance, and technology investment, rather than growth for its own sake.

Private capital shows no signs of losing interest in the brokerage market. In 2025, European broker M&A transactions involving private capital-backed acquirers represented 61% of all deals, continuing the trend from the preceding two years. Now, with interest rates declining, which may lead to more investment capital as debt becomes less expensive, conditions appear even more favorable for increased private capital activity.

The Road Ahead

The insurance brokerage industry entered 2026 with a blend of cautious optimism and structural strength. Even as shifting insurance rate cycles, declining public broker valuations, and macroeconomic uncertainty made 2025 volatile, the sector has demonstrated resilience—particularly in M&A activity and private-market valuations.

However, 2026 could be a transitional year for insurance brokers. As the rate environment shifts, brokers—many who have only experienced the beneficial tailwinds of premium rate increases and limited capacity—may feel the impact of flat or declining rates and broader capacity on their organic growth.

M&A momentum is expected to continue, as the demand for quality firms still outpaces supply. Private capital-backed buyers remain a dominant catalyst, supported by plenty of dry powder, declining capital costs, and the need for inorganic growth.

Valuation multiples for high-quality and top-tier platform firms should remain strong in 2026, as specialization and niche expertise are increasingly driving premium pricing. With interest rates expected to ease further, competition for scarce high-performing assets may intensify, especially among private capital-backed consolidators nearing the end of investment cycles and preparing for recapitalizations, secondary sales, or IPO considerations.

The Future of the Independent Broker

Independent brokers must focus on growing without reliance on rate and market exposure. To do that, better client services remain key. End clients continue to demand more from their brokerage. Industry expertise, data and analytics, loss control and claims services, or even broader solutions (e.g., human resources consulting, retirement planning, individual wealth) are becoming a cost of entry to remain competitive. Independent firms are weighing their options regarding building these services on their own or partnering with one of the 40+ well-capitalized buyers in the marketplace that has already made the investments. Layer all of these client expectations on top of the deluge of headlines on AI moving closer to the point of sale in the insurance brokerage chain, and pressure is mounting on independent firms.

The process of evaluating a long-term strategic direction has become increasingly complex for independent firms. If a firm is not committed to continual double-digit organic growth even in a softening rate environment, it will have a tough time keeping up with the high valuations that others are getting. Some firms will invest heavily in people and technology, utilizing AI for efficiencies and building for continued long-term independence. Others will find a partner that can help them elevate their business to the next level. In either case, 2026 will likely be a year defined by a need for independent brokers to take action.