War in Iran Targets Marine, Energy Infrastructure

Q&A with Ben Gibbons, Global Head, and Harry Bower, Senior Director, Miller Credit, Surety & Political Risks

The U.S.-Israeli war with Iran has had significant global ramifications. Among the insurance markets, both marine and political risk have felt the effects.

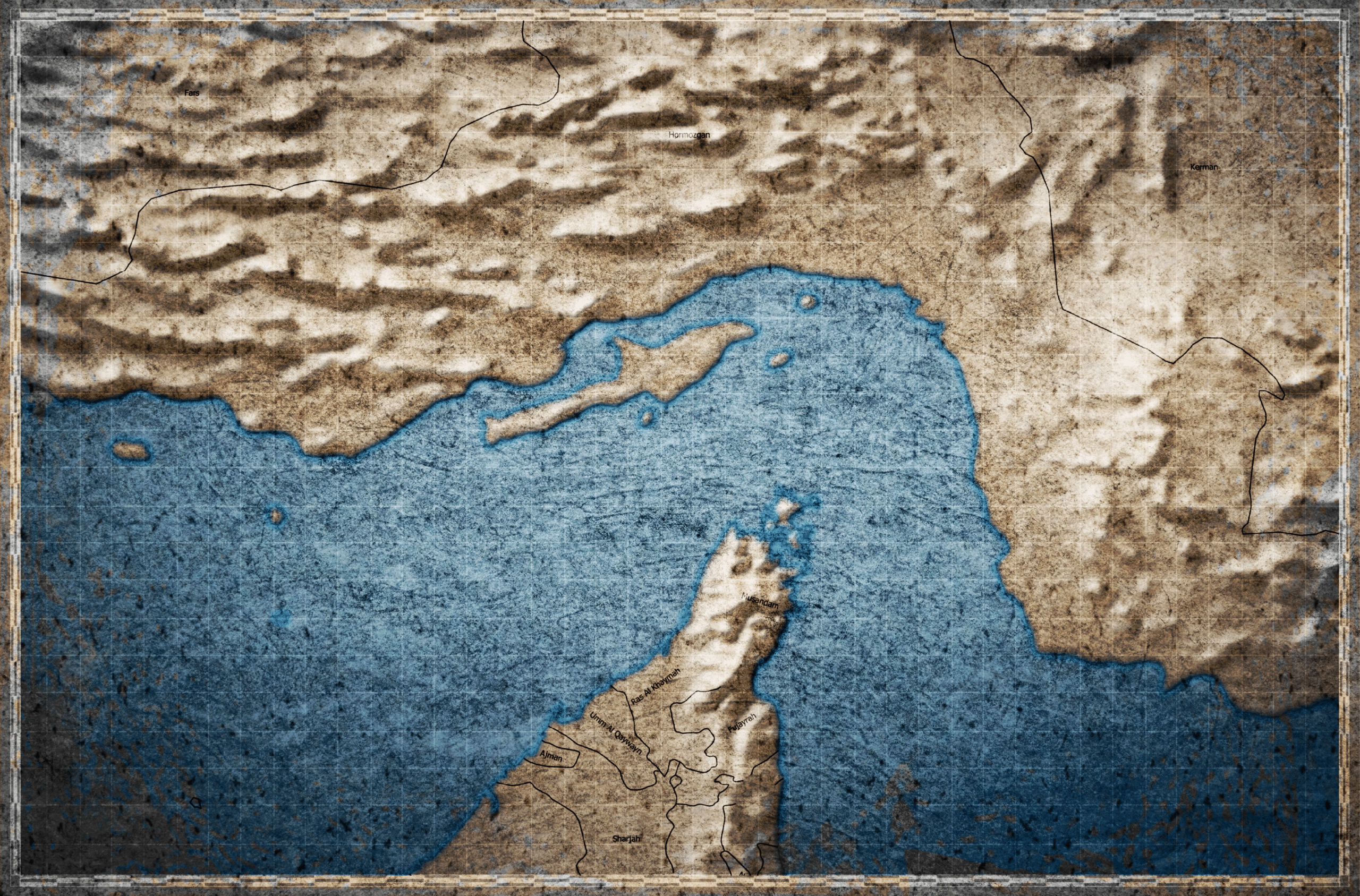

After the start of military operations in February, only a handful of vessels passed daily through the Strait of Hormuz, a key maritime transit route for at least 20% of the world’s oil. A number of vessels were attacked in the Strait, which Iran also peppered with mines. Energy infrastructure in the region, among other facilities, sustained damage—the liquefied natural gas (LNG) production and export complex in Ras Laffan, Qatar, for example, was knocked out of commission in early March by Iranian missile strikes.

At press time, the United States and Iran had declared a two-week ceasefire to allow time for peace talks. The meeting in Pakistan ended without any agreement, and the United States said it would begin blockading Iranian ports along the Strait. There was no sign that the Strait would quickly resume its normal flow of ships.

The effects were felt in many segments of the insurance industry. Marine war risk faced large-scale cancellations and premium hikes of 1,000% or more where coverage was available, while there was “unprecedented demand” for political violence coverage, Howden Re said in a late-March report on the Strait of Hormuz. Eleven distinct lines of business faced impacts ranging from elevated to extreme, the reinsurer said.

Companies that had multijurisdictional political risk programs in place before the conflict escalated were paying rates well below 1% [of the policy limit]. Companies that came to market after the situation deteriorated— if they could find cover at all—were looking at 8% or 9%. Potentially a 15-fold increase, effectively overnight.

Ben Gibbons, global head, Miller Credit, Surety & Political Risks

In this environment, two senior members of Miller’s Credit, Surety & Political Risks (CSPR) team—Ben Gibbons, global head of CSPR, and Harry Bower, associate director of CSPR—sat down with Leader’s Edge to discuss the importance of political risk insurance and what the recent geopolitical turmoil means for companies operating in emerging markets today.

Political risk insurance has evolved from a niche product serving a handful of multinationals in the early 1990s into a sophisticated, multibillion-dollar market relied upon by banks, energy companies, and global investors to protect against events like expropriation, political violence (war/terrorism), currency inconvertibility, and government breach of contract.

It can also serve as a backstop for other forms of insurance. For example, marine coverage quickly grew even more expensive or was canceled outright for vessels that needed to transit through the Strait of Hormuz as the war intensified. Howden Re found that war-risk premiums spiked as high as 3% of vessel value for ships sailing in particularly risky areas around the Strait. “In absolute terms, insuring a USD 100 million vessel for a Gulf transit jumped from USD 250,000 to USD 375,000 per journey.”

The following conversation has been edited for clarity and length.

Q

You mentioned waking up to chaos in February. Walk us through what happens operationally when a conflict triggers marine policy cancellations.

A

HARRY BOWER: That is a fairly accurate description. I woke up on a Saturday morning in late February, turned on the television, and saw reports of Iranian weapons strikes. Anything involving that combination immediately registers—we know our market will be affected. I picked up my phone and, within minutes, saw that marine war cover cancellations were being issued.

In the marine market, any policy with cancellable war cover is monitored constantly. The moment a qualifying event occurs, underwriters can issue a notice of cancellation immediately—there is no waiting until Monday morning, because every hour of additional exposure matters. Those notices typically give 48 hours of continuing cover, which allows policy owners to move the asset away from war-impacted locations.

The problem is that 48 hours is often not enough. If you are operating a drilling rig, shutting down production and preparing for tow takes 24 hours at a minimum. These assets are not self-propelled; so owners need a tug, which then has to get to the location. And a massive rig being slowly moved by a tug is not exactly a discreet target. The operational reality rarely fits neatly into a 48-hour window.

Q

Where does political risk insurance fit in that scenario?

A

BEN GIBBONS: It is important to clarify what marine war cover is and is not designed to do. It is not built to cover war as a permanent risk. It provides a short window intended to give asset owners an opportunity to move vessels out of harm’s way. That is the design. Our product—political risk insurance—therefore exists to complement marine and energy packages.

The real value of having a non-cancellable political risk or political violence policy in place is that it gives you more options. You are able to hold your position, wait for de-escalation, and know your asset is protected in the meantime. You are not forced into a potentially costly and dangerous reactive decision.

BOWER: That is exactly right. A 12-month or multiyear, non-cancellable policy sitting in the background gives you the ability to say: “We will wait until it is safe to move, rather than spending $30 million or $40 million on a short extension under enormous time pressure.” Loss mitigation is expected, but it does not mean mitigation at any cost.

Q

What about companies that were not already covered when this conflict escalated?

A

GIBBONS: They are in a very difficult position. A principle I often come back to is this: insurance is for the unforeseen, not the inevitable. You do not buy political risk cover once a threat is already materializing; you buy it as part of your ongoing risk management strategy, to protect against events that may or may not happen but would have serious consequences if they did.

We have seen this play out starkly in real terms. Companies that had multijurisdictional political risk programs in place before the conflict escalated were paying rates well below 1% [of the policy limit]. Companies that came to market after the situation deteriorated—if they could find cover at all—were looking at 8% or 9%. Potentially a 15-fold increase, effectively overnight. In one case, rates that were stable the week before an event jumped dramatically within days. The window can close that fast.

BOWER: A policy that was bound the week before the situation deteriorated was priced at roughly the same level as it would have been in a calm environment. One decision, taken at one moment, separates manageable cost from extraordinary cost, or no cover at all.

A 12-month or multiyear, non-cancellable policy sitting in the background gives you the ability to say: ‘We will wait until it is safe to move, rather than spending $30 million or $40 million on a short extension under enormous time pressure.’ Loss mitigation is expected, but it does not mean mitigation at any cost.

Harry Bower, senior director, Miller Credit, Surety & Political Risks

Q

What are the broader economic consequences of sustained conflict affecting Gulf energy infrastructure?

A

BOWER: The scale of the issue comes down to infrastructure. Energy infrastructure requires enormous capital investment and years of development time. If you lose a few oil wells, that is disruptive but manageable as there is capacity elsewhere to absorb it. When you lose major refining infrastructure, there is nothing to immediately take up that slack. Facilities like Ras Laffan—the world’s largest LNG export complex, located in Qatar—represent a significant share of global LNG refining capability, and we are talking about a three-to-five year timeline to bring that back online. That means the market is short that supply for half a decade.

At the same time, the Gulf region produces approximately 30% of the world’s oil, historically flowing through the Strait of Hormuz. Alternative routing through Saudi overland pipelines moves perhaps 7 million barrels per day versus the 20-plus million that transit the Strait. Iraq can add roughly 250,000 barrels per day through pipeline, which is economically inconsequential in the context of the total deficit. The math leaves the market significantly short every single day.

There is also the refined product dimension. Jet fuel is a particular concern. Airlines source fuel from established, trusted suppliers for very good reason: aviation safety leaves no margin for substandard supply. When the world’s most sophisticated refining facilities are offline, that cannot simply be replaced by redirecting throughput elsewhere. In fact, we’re already seeing regional carriers canceling flights as a result. Sustained high jet fuel prices will put real pressure on airline economics globally.

Q

What does this situation mean beyond energy markets?

A

GIBBONS: Higher energy costs create inflationary pressures that are not contained to any one region—they flow through shipping costs, manufacturing costs, consumer prices. The second-order effects compound: if inflation rises, interest rates will also rise, which further increases the financing costs for businesses already squeezed by higher energy prices. That translates directly into elevated credit risk across a wide range of sectors and geographies.

For Europe specifically, the questions are significant. How does the continent continue to access oil and gas at manageable cost? What pressure does that put on European businesses and households? And what does it mean for the political positioning around Russia sanctions, given that Russia remains a major gas supplier? Do the economics of energy security force a reassessment of that stance? What happens to North Sea oil and gas policy in the U.K.? These are not abstract questions but are conversations that are already happening at the government level, and they will have real consequences—for the industries affected, for economies, and for the global risk landscape.

BOWER: It is worth adding that, according to OPEC, peak oil demand is not projected to arrive until around 2045. Whatever the trajectory of the energy transition, oil and gas will power this world for at least the next two decades. Conflict in the Gulf is a reminder that energy security is genuinely strategic and not just an economic consideration. Countries that have rationalized energy dependence on the assumption that global markets will always function efficiently are being reminded that that assumption has limits.

Q

Is there any positive note to end on?

A

BOWER: One constructive outcome from this disruption is that it forces a genuine reassessment of energy strategy. For example, decisions to close European refineries, assuming supply will always be available cheaply from elsewhere, will be reevaluated. The energy transition is coming, but so is a 20-year window in which the world still needs to manage oil and gas intelligently.

GIBBONS: From an insurance perspective, our market exists precisely to manage uncertainty for clients, and Lloyd’s in particular has a long track record of staying present through major world events, even when capital markets retreat. Bond markets sell off, credit might tighten. But insurance stays.