Does AI Adoption Matter in M&A?

In mergers and acquisitions, it’s not the technology you build that attracts buyers, it’s how effectively you use it to create differentiation, efficiency, and organic growth.

Artificial intelligence has become a fixation across most business sectors, with financial services and the insurance industry topping the list for greatest potential impact.

Automation and efficiency are the goals for many brokers looking to harness the power of the latest AI technology. But how important is AI adoption in the merger and acquisition (M&A) selection process? Do sellers need a defined strategy for the technology to be attractive to buyers? The answer, perhaps surprisingly, is yes and no.

For independent agencies, investing heavily in proprietary AI technology may not deliver the expected return on investment (i.e., higher multiple) in an acquisition. In most cases, an acquiring organization is unlikely to adopt the technology an independent firm builds. Most of the largest acquirers are already light-years ahead in their technology stacks, leveraging AI to enhance offerings, drive efficiencies, and scale operations.

Acquirers are looking for something they don’t already have. Rather than pouring resources into AI development, firms seeking buyers may be better served by investing in a differentiated niche strategy—such as specializing in construction, healthcare, or another complex vertical—and hiring the talent required to support it. That specialization is far more likely to be an attractive feature and scaled by a buyer.

This is not to say AI investments are unimportant. Any investment in technology should be aimed squarely at driving meaningful improvements in margin or organic growth. AI should be viewed as a tool for creating efficiency, not for replacing people. When technology creates greater efficiency, it also creates more capacity. It is then incumbent on leadership to redirect that capacity toward sales, client service, and other ways of helping the firm reach (or exceed) its growth goals.

Today, AI is fueling a degree of hysteria, with firms racing to “keep up” for fear of falling behind in adoption. According to a MarshBerry technology survey, most firms’ tech enhancements focus on service and operational efficiencies rather than revenue generation. What separates high-performing firms is how they use the extra capacity those efficiencies create. Ultimately, sustainable organic growth—not technology alone— matters most to acquirers.

M&A Market Update

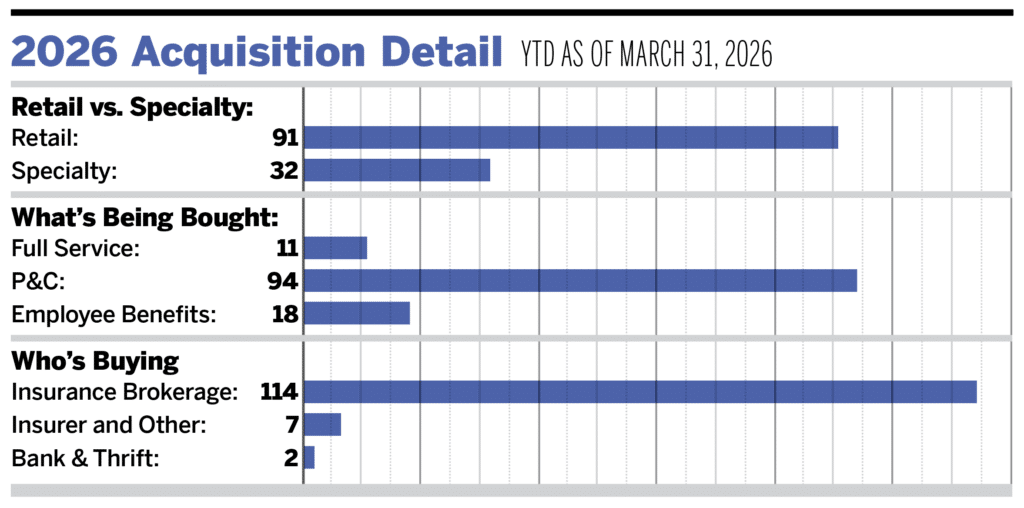

As of March 31, there were 123 announced insurance brokerage M&A transactions in the United States in 2026—down 4.9% from 129 deals announced last year at this time. Private capital-backed buyers accounted for 86 of the 123 deals (69.9%) through March. Independent agencies were buyers in 15 deals, representing 12.2% of the market. Bank buyers have announced two transactions to date this year. Deals involving specialty intermediaries as targets accounted for 32 transactions.

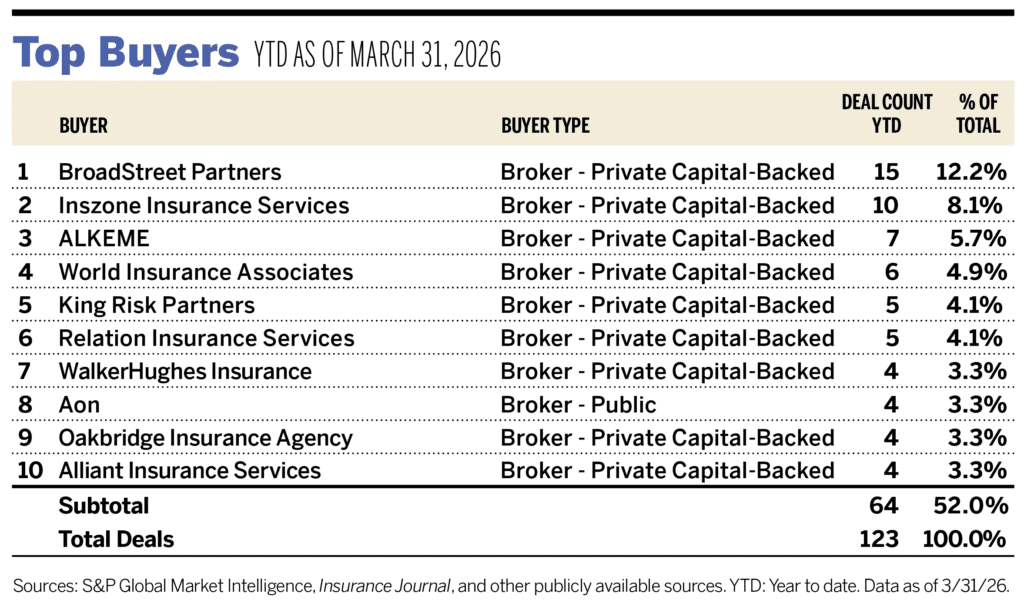

Ten buyers accounted for 52.0% of all announced transactions year to date, while the top three (BroadStreet Partners, Inszone, and ALKEME) accounted for 26.0% of the 123 transactions.

Notable Transactions

- March 2: WalkerHughes Insurance acquired Hometown Insurance Agency, a Missouri-based retail brokerage, marking its entry into the Kansas City metropolitan market. The transaction expands WalkerHughes’ geographic footprint and supports its strategy of growing through partnerships with established local agencies while preserving their client-facing operations and regional identity.

- March 18: TheGuarantors secured a majority investment from Warburg Pincus to support the continued expansion of its technology-driven lease guarantee platform for the U.S. rental housing market. The company provides insurance-backed solutions that help renters qualify for housing while protecting property owners from default risk, supported by AI-powered underwriting and integrations with large institutional property managers.