Numbers Don’t Always Tell the Whole Story

Access to capital is starting to tighten.

In July, the Federal Reserve raised its benchmark interest rate by 25 basis points, for the fourth time this year.

At the same time, the Fed reversed its April stance on a late-year recession, stating that the risk of a U.S. recession was diminishing on the heels of improved underlying inflationary numbers as well as continued economic growth.

For insurance distribution mergers and acquisitions, the numbers that matter most are those around transaction volume and valuations. Through the end of July, the M&A market continues to be active, with quality firms still commanding top-of-the-market valuations.

But numbers don’t always tell the whole story.

It has been a good two-year run for top performing insurance brokerages, fetching valuations at historic levels. It has also been good for average firms that have benefited from the high demand of private-capital backed buyers that are seeking expertise and looking to expand into new geographies, specialty services or anything that can help give them a competitive advantage. The average base purchase price for brokerages for the 12 months ending June 30, 2023, was 10.6x EBITDA. This is 17.3% higher than the average base purchase price in 2019, prior to the pandemic, of 9.03x EBITDA.

Despite the rosier economic outlook and robust two-year M&A run for insurance brokerages, access to capital is starting to tighten. As firms start to exhaust their dry powder and are unable to find financing via senior debt due to leverage ratios that are higher than lenders are willing to accept, they may be forced to seek funding by raising some type of equity. Buyers could soon be reaching a point where they will need to make a decision on issuing preferred or common equity to get cash for their next acquisitions. This shift in strategy will likely lead to a more discriminating approach to evaluating acquisitions, as equity is a more costly source of investment funds from a shareholder return perspective.

Additionally, with private equity funding having contributed to an increasing portion of deal volume over the past few years, demand will be impacted by the ability of these buyers to continue their aggressive acquisition strategies. There are a significant number of PE-backed firms, potentially as many as seven or eight, that are looking to possibly recapitalize in 2024. Historically, value placed on these firms has been high given the scarcity of opportunity in the space. This could pose a potential risk for average firms that may not be able to attract the right capital in a more competitive environment.

We expect the remainder of the year to see sustained levels of activity, particularly for high-quality firms that can show sustained organic growth. However, firms that are not able to demonstrate sustained organic growth may see valuations reset to pre-pandemic levels as these other market factors influence demand and the ability for buyers to fund activity.

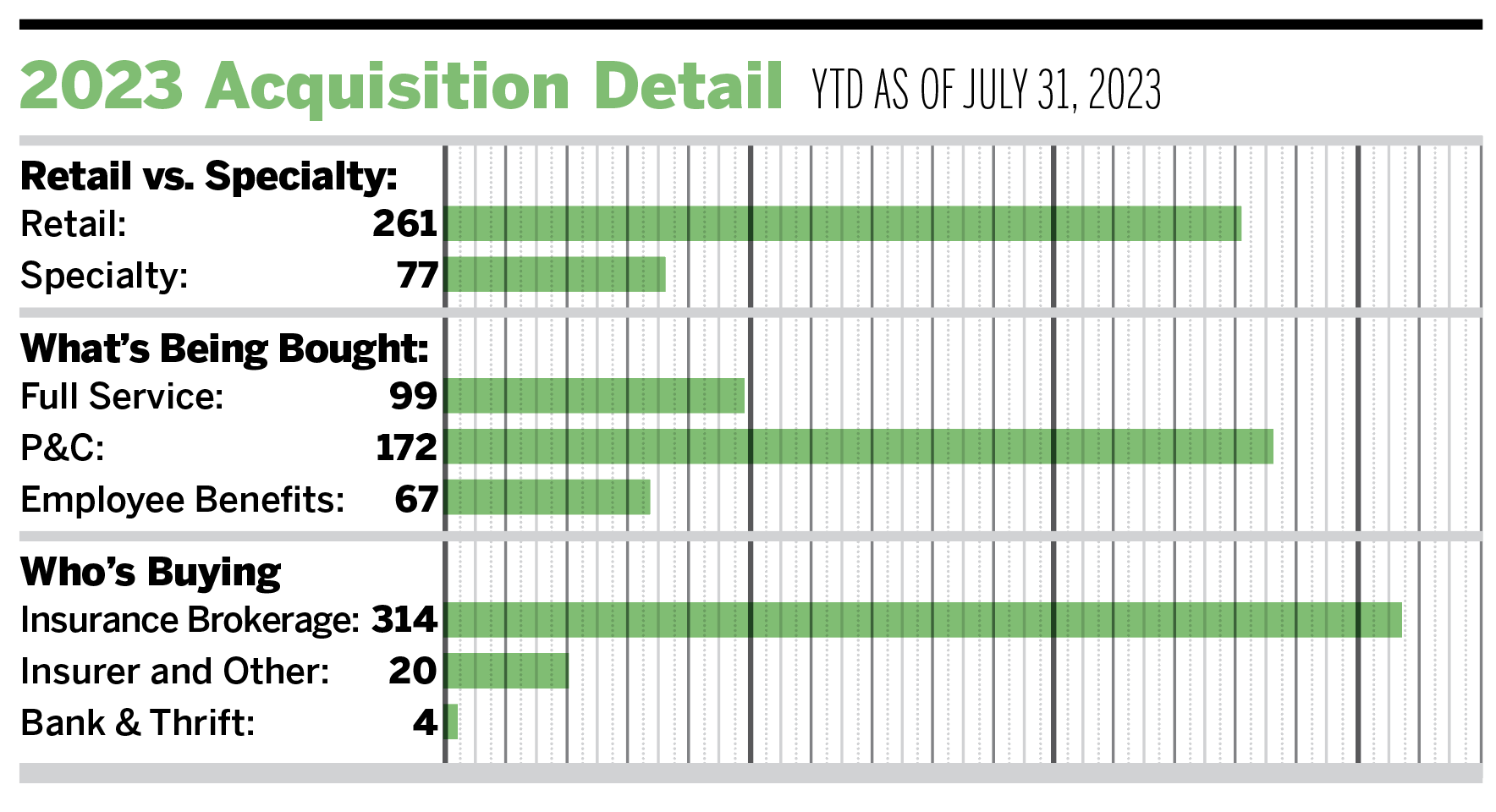

M&A Market Update

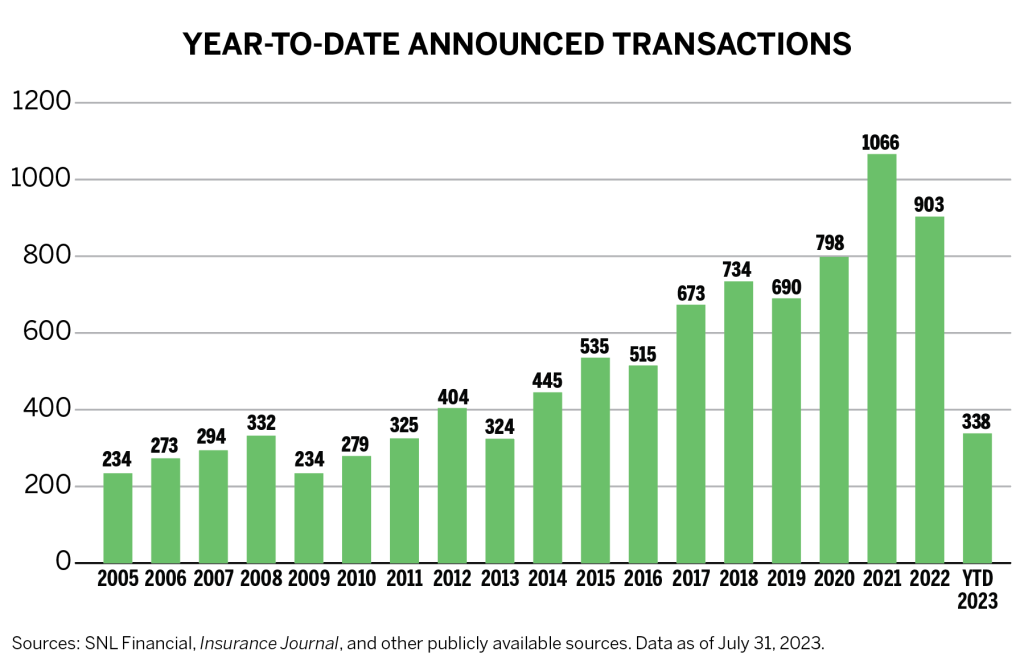

Through July 31, 2023, there have been 338 announced merger and acquisition transactions in the United States.

Private-capital backed buyers have accounted for 245 of the 338 transactions (72.5%) through July, which is consistent with the proportion of announced transactions in 2022. Total deals by these buyers has increased at a compound annual growth rate of 11.1% since 2018, with a marked increase after the onset of the pandemic.

Through July, independent agencies as buyers accounted for 48 transactions (or 14.2%), down from 17.2% in 2022. Bank and thrift as buyers accounted for four announced deals (or 1.2%), down from 2% in 2022.

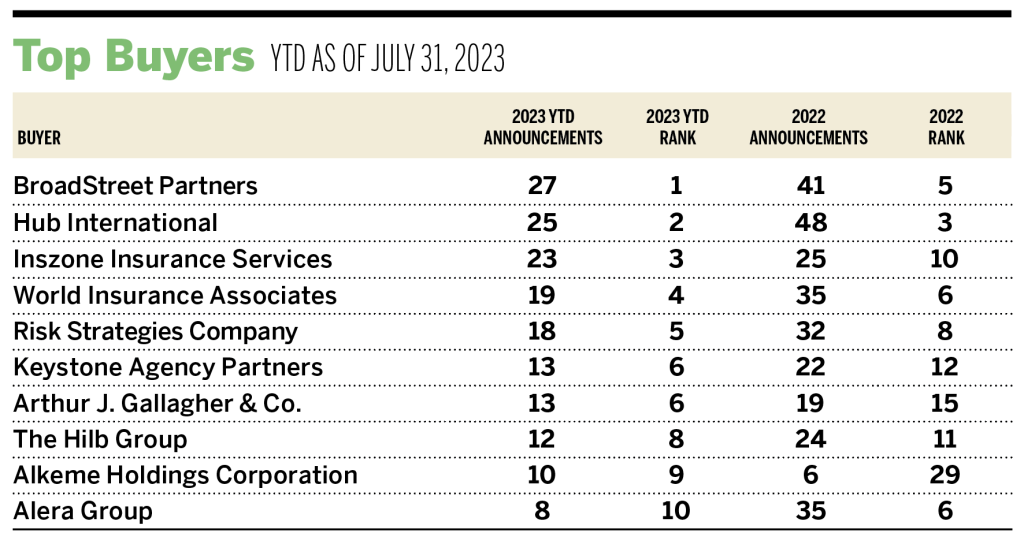

Deal activity from the marketplace’s most active acquirers has remained strong in 2023. Ten buyers account for 56% of all announced transactions, while the top four (BroadStreet Partners, Hub International, Inszone, and World Insurance Associates) account for 31.3% of the 338 total transactions.

Notable transactions include:

- July 6: Higginbotham announced it has acquired Cress Insurance Group. Cress, a New Mexico-based P&C and employee benefits agency, is Higginbotham’s second acquisition in New Mexico. With the acquisition, Higginbotham’s New Mexico customer base rises to 2,500 customers.

- July 7: Evertree Insurance Services announced the acquisitions of First American Insurance, Alliance Insurance Services, and The Banks Agency. These three Colorado-based agencies will establish Evertree’s Mountain Region.

- Aug. 1: The Graham Company announced its sale to Marsh McLennan Agency. The Graham Company is an insurance and employee benefits brokerage that partners with businesses in high-risk industries.