Not All Growth Is Equal

Players in the brokerage space are seeking more than just organic growth.

In this current hard market, capacity is shrinking in certain markets and exposure bases and premiums continue to rise. As a result, it's difficult to assess whether organic growth is being driven by concerted efforts of brokerages or simply by external factors.

For buyers, there is significant risk in making acquisitions in firms that may not be able to sustain their organic growth when market conditions change and the rate environment settles down.

That’s why most acquirers are digging down into the details of those organic growth numbers, poking holes, and looking for the true drivers of a firm’s organic growth.

Buyers want to understand how much of that growth comes from new business written (sales velocity). This includes business from new clients or by writing new lines of coverage for existing clients.

In a hardening market, or increased exposure base (given U.S. GDP growth of 3.1% in 2023), revenue and annual organic growth numbers have been lifted due to rate increases, and not necessarily the results of new business generation.

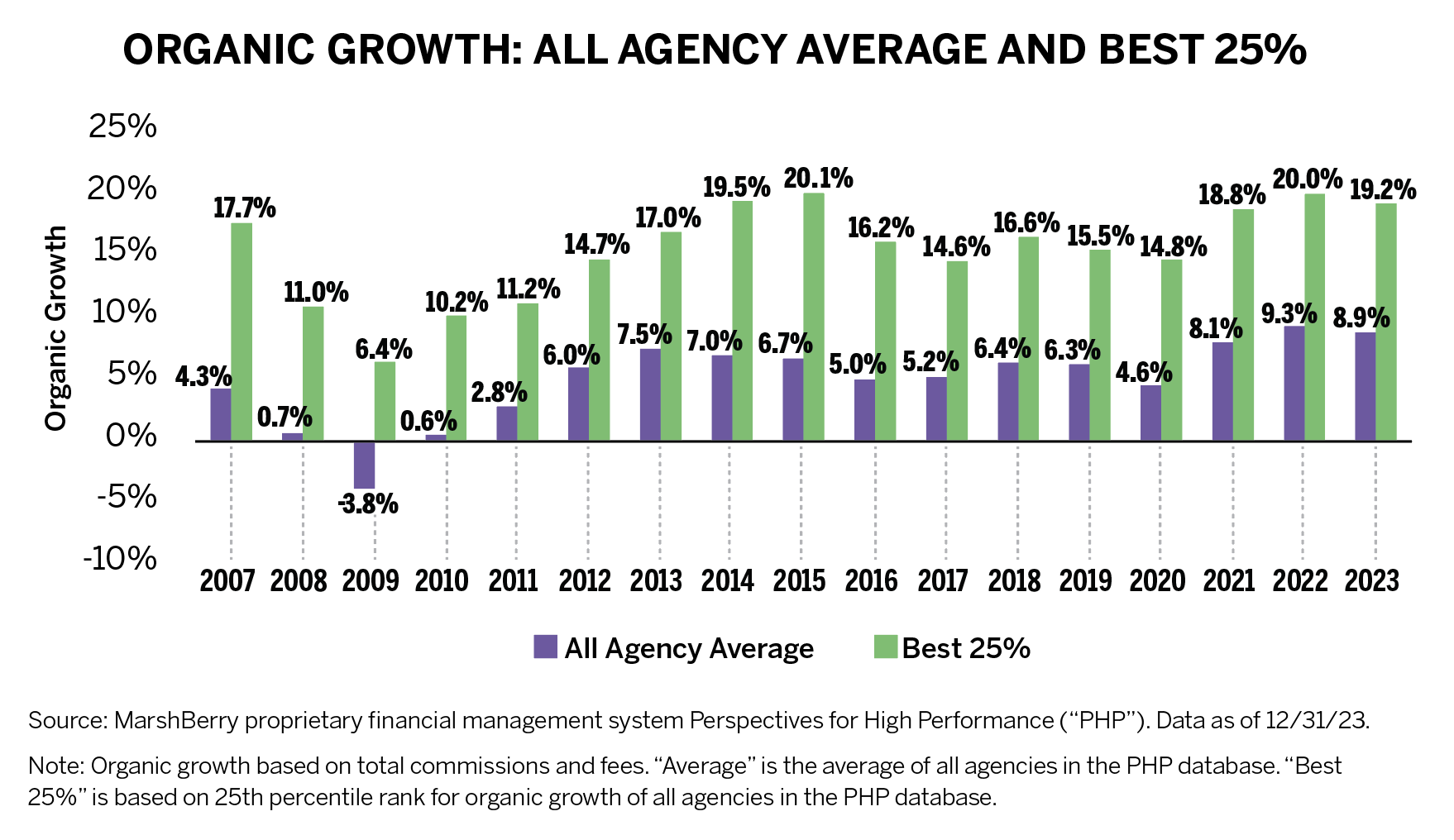

Organic growth in 2023 across the insurance brokerage industry, driven by the hard market environment and premium rate increases, saw numbers that rivaled the highs over the previous two years.

According to MarshBerry’s proprietary financial management system Perspectives for High Performance (PHP) the average organic growth rate for all agencies in 2023 was 8.9% (slightly down compared to the 9.3% growth in 2022). But how much of that is growth due to external factors?

Conversely, high-performing firms (the best 25%) grew an average of 19.2% in 2023. This is where organic growth differentiation exists. These are firms that are making strategic decisions to help create more value for their firm and drive meaningful, sustainable, organic growth. This is growth that is not dependent on rate increases, renewals or external macroeconomic conditions. These firms are investing in technology, recruiting and retaining the best people, expanding product offerings, developing specialization, and expanding geographically. The sales velocity of the best 25% of firms is nearly 10 percentage points higher than the average firm. They are writing more new business and controlling their firms’ growth in and out of market cycles.

When the decision comes to sell or partner, these firms offer strategic elements to potential partners that are looking to fill gaps or build upon their own strategy of growth. So regardless of market conditions, those companies that display strong organic growth that is driven by new business and intentional value creation become far more attractive to buyers.

M&A Market Update

As of Jan. 31, 2024, there have been 29 announced insurance brokerage merger & acquisition (M&A) transactions in the United States this year.

Private capital-backed buyers have accounted for 21 of the 29 transactions (72.3%) through January. This represents a 13.1% increase since 2019 when private capital-backed buyers accounted for 57.3% of all transactions. Independent agencies accounted for three deals so far in 2024, representing 10.3% of the market, a slight decrease from 2023 when independent agency acquisitions represented 15.6% of the market. Bank buyers continued to fall, declining from 18 transactions in 2022 to nine transactions in 2023—an all-time low. Bank buyers had no transactions in January.

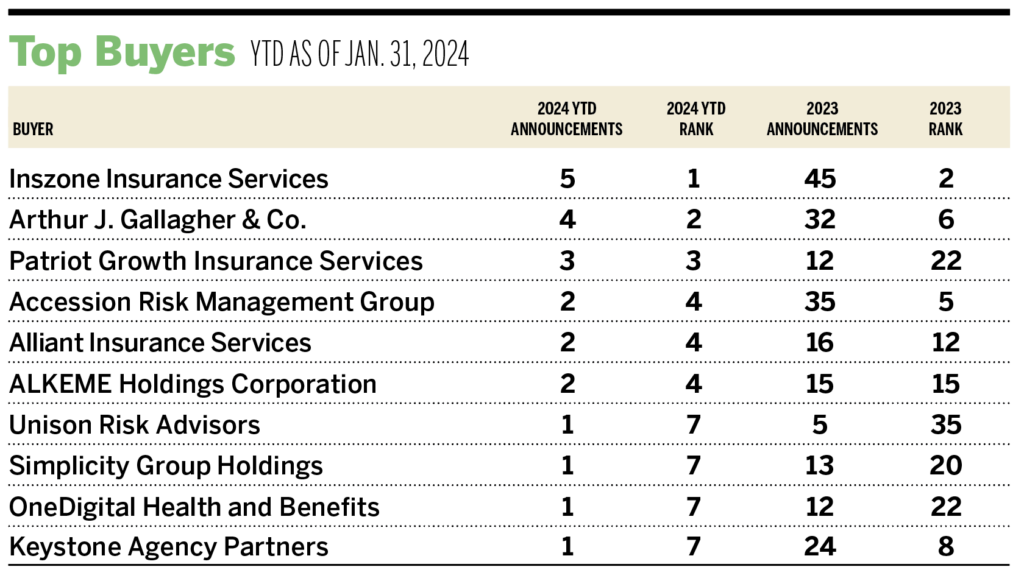

Deal activity from the marketplace’s most active acquirers has remained strong in the beginning of 2024. Ten buyers have accounted for 75.9% of all announced transactions, while the top three (Inszone Insurance, Arthur J. Gallagher, and Patriot Growth) account for 41.4% of the 29 total transactions.

Notable Transactions

January 5: Johnson & Johnson Insurance announced that it has acquired Mid Valley General Agency, headquartered in Salem, Oregon, with operations in Idaho, Montana, and Washington. Mid Valley General Agency, a family owned managing general agency, specializes in catering to retail insurance agents with difficult-to-place risks. Based in Charleston, South Carolina, Johnson & Johnson is also a managing general agency.

January 9: Unison Risk Advisors-owned Oswald Companies announced that it has acquired Brieden Consulting Group. This integration strengthens Oswald’s presence in Michigan, complementing its existing operations in Bloomfield Hills. Brieden brings a significant portfolio of employee benefits business to Oswald, while Oswald specializes in property and casualty, employee benefits, life insurance, and retirement plan services.