Can Independents Compete in a Consolidating Market?

Insurance brokerage M&A is raising the bar on strategy, technology, and more for firms that don’t want to sell.

Insurance brokerage mergers and acquisitions (M&A) are often framed from the potential seller’s perspective.

Is it time to partner with a buyer? Raise debt or equity capital to support growth strategy? Or stay the course and remain independent? But even firms with no intention of selling can’t avoid the effects of industry consolidation—it reshapes the competitive environment for all brokerages. The entire market is increasingly influenced by private capital-backed platforms, serial acquirers, and scaled national brokers.

Consolidation by the Numbers

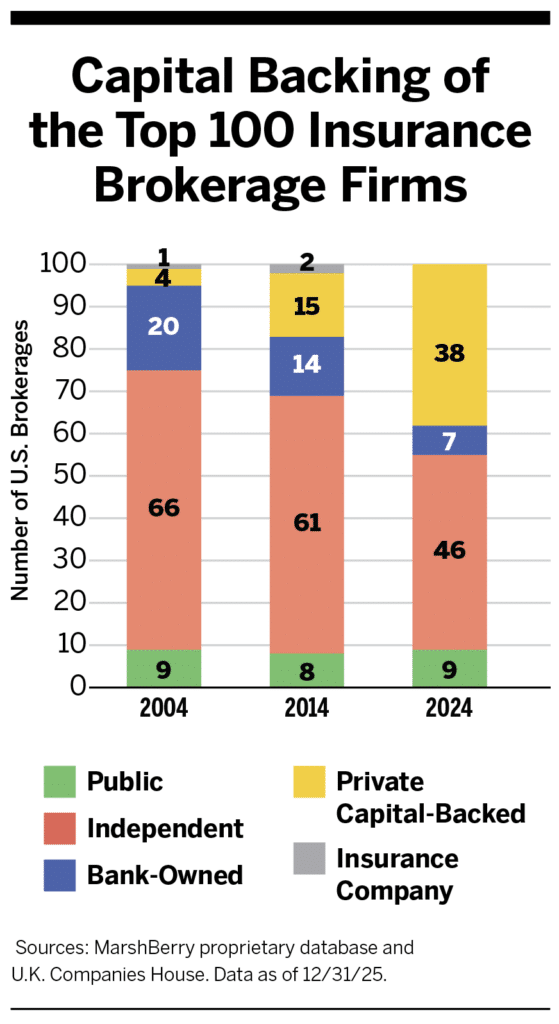

Ownership of the top 100 U.S. insurance brokerage firms, based on revenue and primarily comprised of property and casualty (P&C) business, has changed over the past 20 years. Most notable has been the simultaneous shrinking of the number of independently owned firms and the increase in private capital-backed brokerages.

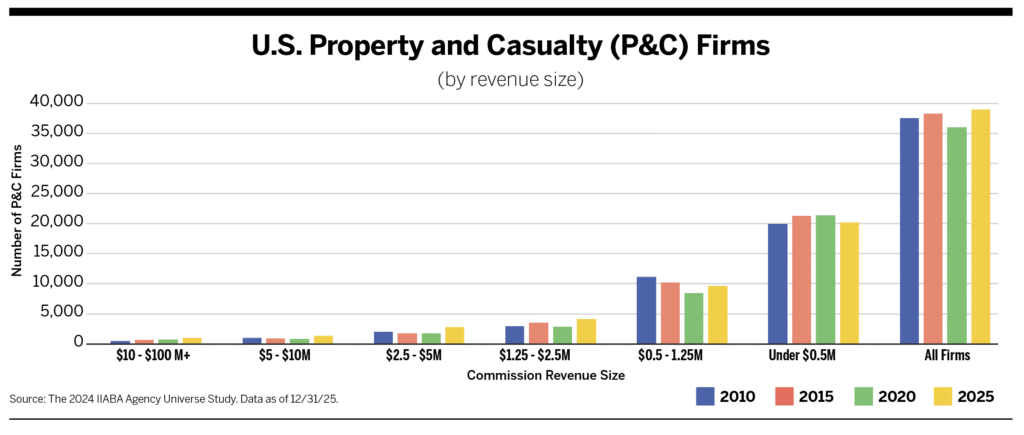

The total number of P&C firms also continues to grow. This initially seems counterintuitive, as M&A indicates a decrease in market size. Over the past 15 years, nearly 10,000 P&C insurance brokerages have sold. Yet, there are 1,500 more P&C firms in 2025 (approximately 39,000) than there were in 2010 (approximately 37,500). Essentially, for every firm that sells, another brokerage pops up.

Impact of Consolidation on Independents

Some owners ask, “If I’m not planning to sell, why should I care about M&A?” Because consolidation changes the terms of competitive differentiation. The traditional independent value proposition—local relationships and personal responsiveness—remains important. But on its own, it may not suffice in a market where the effects of consolidation constantly ripple outward.

Here are examples of how M&A affects even brokers who are not putting their firms in play.

Rising expectations: As larger platforms acquire specialty brokers and expand capabilities, they broaden their value proposition: deeper analytics, specialized vertical expertise, alternative risk solutions, claims advocacy infrastructure, and expanded geographic reach. M&A raises the baseline for what the term full-service brokerage means. An independent firm is competing against brokerages that provide not only an expanded set of coverage offerings but also more proactive risk advisory services, data-driven renewal strategies, specialized coverage knowledge, and well-coordinated and responsive claims support.

The power of scale: Consolidators present carriers with large, diversified books of business and standardized submission processes. This can translate into stronger market leverage and preferred access in difficult underwriting environments. There is no question that carriers value independent brokers. However, they increasingly reward predictable underwriting outcomes, clean submission quality, operational consistency, and data discipline. For firms that are not selling, the implication is clear: access is tied not just to relationships, but to execution quality.

Talent pressure: M&A does not just consolidate revenue, it compresses high-level talent within a smaller number of organizations and creates recruiting engines. Scaled firms often have dedicated recruitment teams, capital to support producer lift-outs, more clearly structured compensation models, and better-defined career tracks to attract the best and brightest.

Growth strategies: Consolidators can introduce clients to broader capabilities and solutions to help drive cross-selling. Independent firms can still compete effectively, but the best firms define a clear niche, market their advisory capabilities, demonstrate measurable client outcomes, and build structured referral networks. In other words, in a consistently consolidating marketplace, growth becomes less about relationships alone and more about repeatable delivery of value.

Practical Considerations for Non-Sellers

Firms committed to remaining independent should consider these priorities:

- Clarify your strategic identity: Define whether the firm is a specialist, a best-run generalist, or a hybrid—and align investment accordingly.

- Institutionalize client ownership: Reduce key-person exposure through teambased account management.

- Formalize talent pathways: Document career tracks and invest in producer development programs and incentives that can attract and retain top talent.

- Enhance operational rigor: Standardize submissions, renewal processes, and stewardship communication.

- Explore selective partnerships: Even without pursuing a sale, firms may consider small tuck-in acquisitions and/or geographic or capability-driven alliances to remain competitive.

- Invest in technology: AI and data management investments are accelerating in the insurance industry. Firms need a strategy for investment, clarity on the amount in dollars, and the cash flow required to keep pace. Once the investment decision is made, it’s important to have someone, potentially a new hire, to help support this investment in the future infrastructure of the business.

Consolidation does not eliminate a brokerage’s ability to remain independent, but it does raise the bar for what an independent firm requires to thrive. Taking proactive measures strengthens the firm’s ability to remain independent and makes the business even more valuable to potential acquirers—if the time does arrive to exit. As market pressures mount, insurance brokers need clarity and confidence that their current investment strategy will be sufficient to help them drive consistent growth throughout the future of their business.