A Down Year for Deals

The insurance brokerage industry took an M&A breather in 2023, but signs look strong for dealmaking in 2024.

Everyone likes a comeback story.

M&A deal pace slowed in 2023 due to factors including uncertainty around buyers’ capital, increasing buyer selectivity and a continued lack of supply.

Specialty transactions hit all-time highs in deal count and market share.

Despite headwinds, European insurance brokerage M&A remains strong and promising.

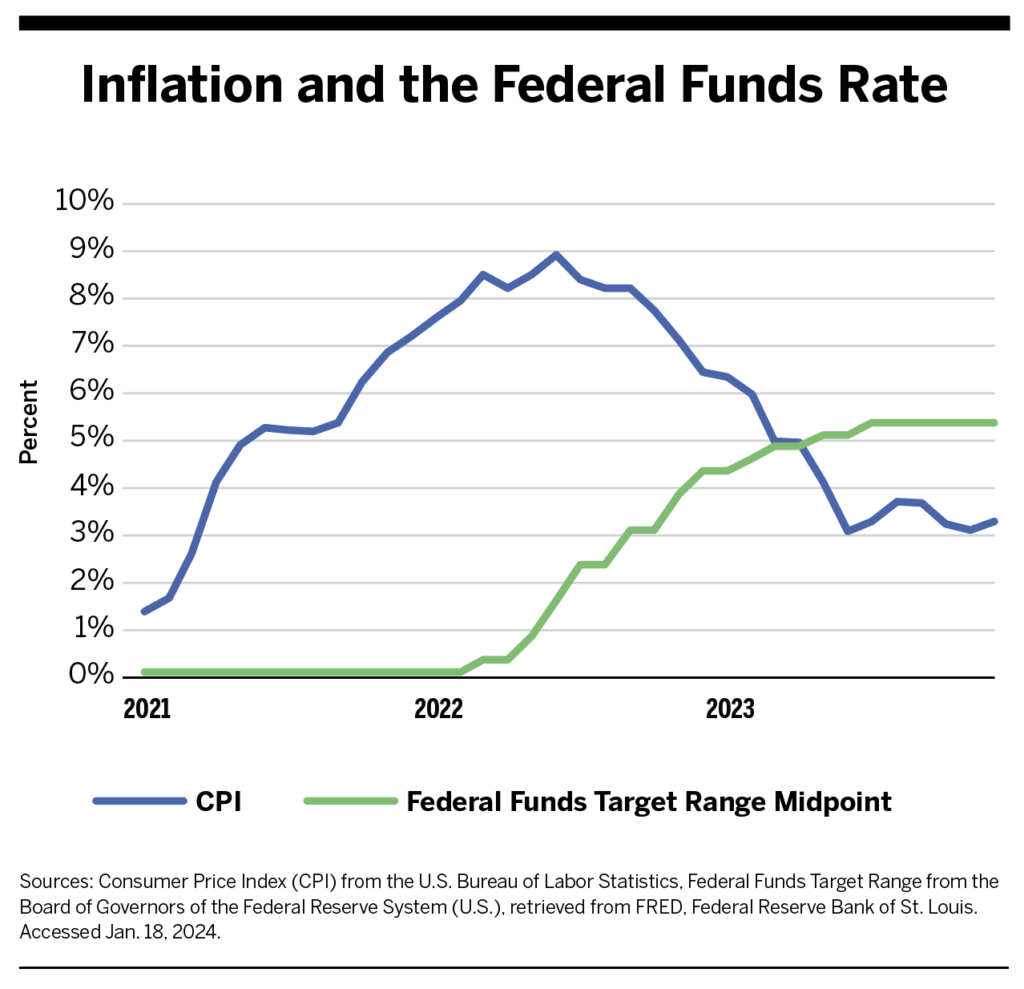

And economically, 2023 will generally be remembered as a comeback year following a tough 2022. While in 2022 everything seemed to be going in the wrong direction—with rising inflation, rising interest rates and falling stock markets—2023 seemingly defied most economic prognosticators. In the end, inflation eased, the Federal Reserve (Fed) paused rate hikes, and the markets rallied.

However, in the insurance brokerage mergers and acquisitions (M&A) world, the year felt like a pause rather than a comeback. Restrictive debt markets from 2022 spilled into 2023, putting a crunch on buyers’ capacity. It was unclear whether companies had enough capital to continue acquiring other businesses while also meeting cash flow demands driven by earnout payments that reflected successful growth by firms bought up two to three years ago. While most buyers continued making acquisitions, many became more deliberate, slowing the pace for deals and reducing their buying appetite. Most of the year felt like a wait-and-see game for the Fed’s next move on interest rates and how the economy would react.

Compounding the impact of lower buyer demand was the continued lack of supply by sellers. Unlike previous end-of-years in which firms were compelled to sell on fears of pending tax or regulatory changes, 2023 offered no urgency for firms to sell.

Additionally, some firms recapitalized their existing private equity (PE) sponsors in 2023, while others added preferred equity to their capital stack given a lack of other compelling options to secure capital.

The year ended with 807 announced deals for insurance distribution transactions in 2023—a 10.6% decline from 2022—according to MarshBerry’s data (see end note for deal count sources). The number of deals increased in the fourth quarter of 2023, compared to earlier in the year, as economic conditions improved and companies raised more debt capital, creating more capacity. That could be a good sign for dealmaking in 2024.

Economy Beats Forecasts

GDP Rises

At the start of 2023, forecasters anticipated at least one quarter of real gross domestic product (GDP) declines on average, and many thought there was a good chance the country would fall into a recession during the year. The Federal Reserve Bank of Philadelphia’s Fourth Quarter 2022 Survey of Professional Forecasters reported a median risk of a negative quarter ranging from 43.5% to 49.4% for each quarter of 2023.

However, GDP instead rose each quarter at annualized rates of 2.2%, 2.1%, 4.9% and (an estimated) 3.3%—for an estimated 2.5% for full-year 2023. The primary contributor to growth was household consumption spending on services, which accounted for a third of real GDP gains. Government spending, business investment, consumer spending on goods, and an increase in net exports also supported GDP gains in 2023, with declining private inventories offsetting further advances.

Inflation Falls

Inflation registered at 6.3% to start 2023, well above the Fed’s long-term goal of 2% but on a downward trend from the peak of 8.9% in June 2022. To combat inflation, the Federal Reserve raised its federal funds target range seven times in 2022, including two hikes of a half point and four of three quarters of a point. In 2023, the Fed resumed its traditional quarter-point increases, raising the target range in February, March, May and July. Inflation ended the year at 3.3%.

In the final quarter of the year, the Federal Reserve indicated it was done raising interest rates. Published projection materials show Fed board members anticipate the federal funds rate will decline in 2024, with a median projection of a 4.5% to 4.75% target range by the end of the year. The federal funds rate sat at 5.25% to 5.50% as of March.

Employment Holds Firm

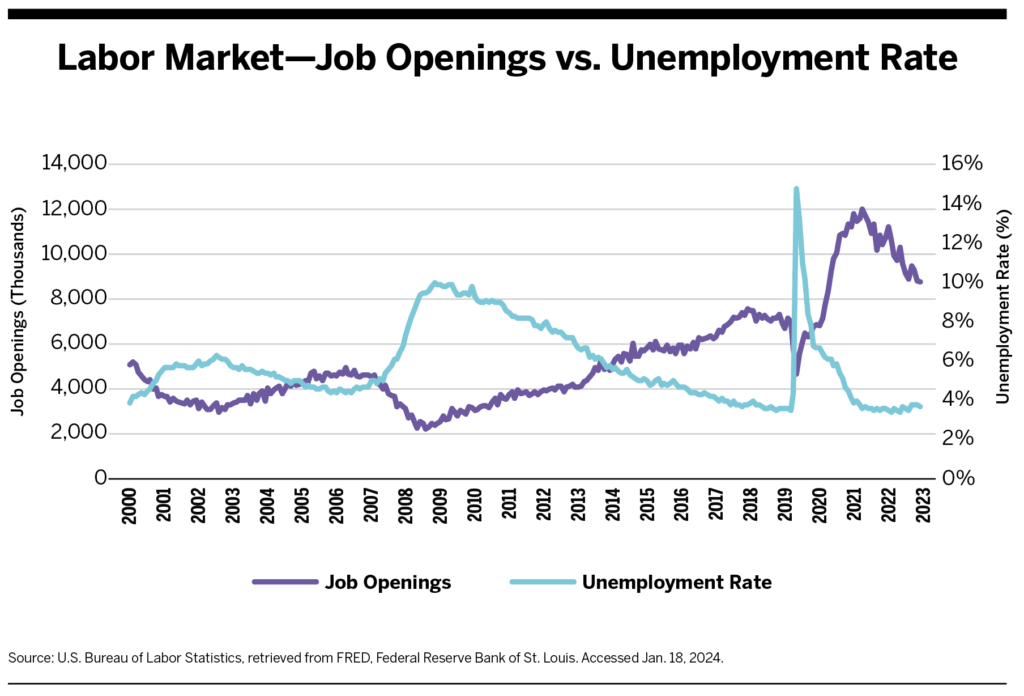

In a simplified view of the economy, many forecasters would expect interest rate hikes to drive up unemployment. An increased cost of capital theoretically should be a headwind to business investment and growth, resulting in fewer job openings. However, unemployment remained low in 2023, rising only slightly over the course of the year to close at 3.7%. Additionally, while job openings declined throughout the year, they remained elevated from pre-pandemic levels.

It is commonly accepted that the economy’s reactions lag monetary policy changes, so both inflation and unemployment could certainly continue to change because of the Fed’s actions over the past two years

Organic Growth Continues

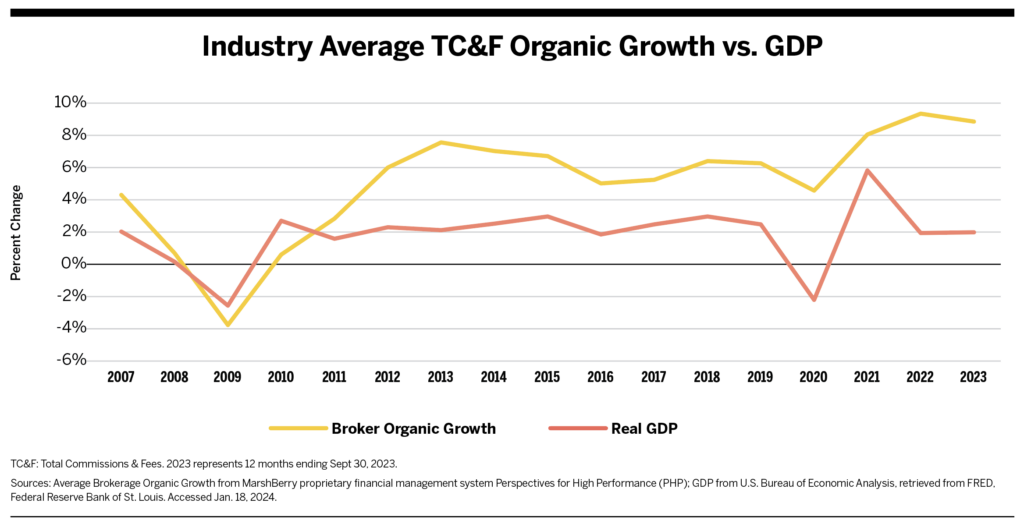

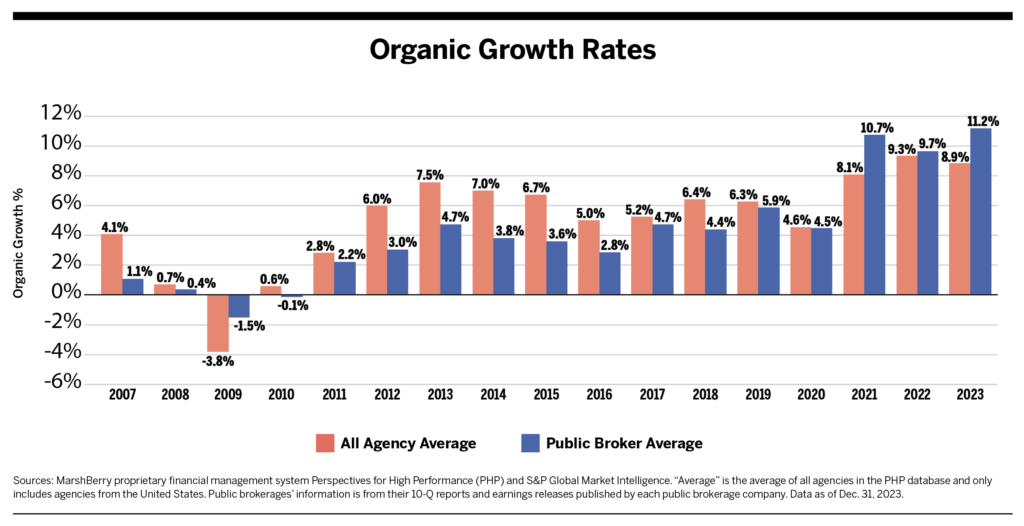

The insurance industry grew strongly again in 2023. Total written property and casualty (P&C) premiums rose to a new high, and brokerage organic growth remained near 2022’s peak, at 8.9% on average in the 12-month period ending Sept. 30, 2023, compared to 9.3% for full-year 2022. Organic growth often tracks movements in GDP growth. However, brokerages continue to benefit from rising premium rates. Inflation and increasing demand for some lines of coverage have expanded the total insurable value of the U.S. economy even as economic growth slowed over the past two years.

Inflation Impairs Underwriting Profits

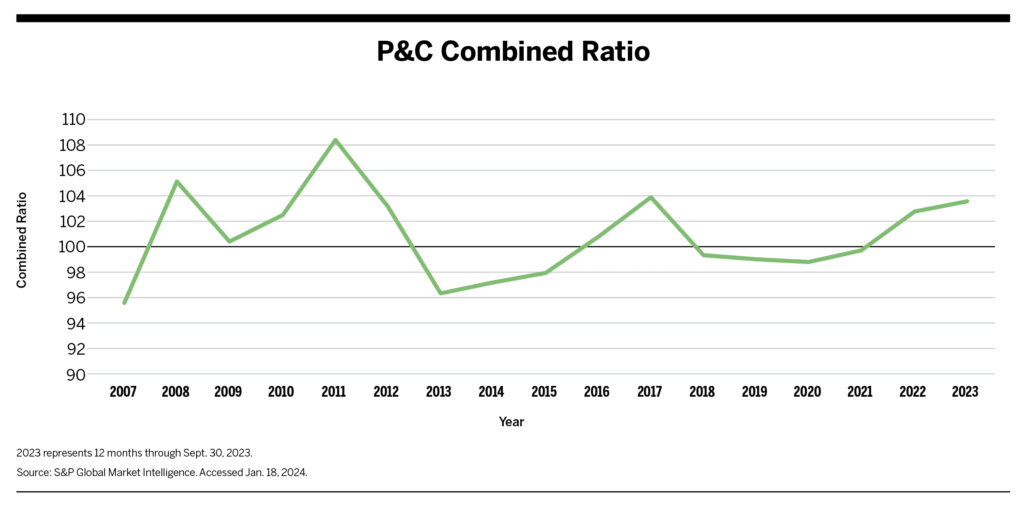

Even as the economy beat forecasts, insurance underwriting profitability took a hit again in 2023. The net combined ratio for P&C underwriting is forecast to worsen to 103.9, up from 102.4 in 2022. Combined ratios under 100 indicate underwriting gains, while ratios over 100 indicate losses.

Deteriorating underwriting profitability can have mixed effects on the insurance brokerage space. An unprofitable year means less profit sharing paid to brokerages. On the other hand, carriers often increase premiums to account for an increase in losses, which means higher commission income for brokerages. However, increased premiums could also prompt insureds to seek coverage elsewhere or even drop coverage entirely, resulting in lost business for brokerages. MarshBerry’s data indicate that, in general, brokerages have benefitted from rising premiums, with organic growth rates registering near record highs despite low sales velocity.

According to data from The Council of Insurance Agents & Brokerages’ P/C Market Index, the strongest commercial line rate increases in the first three quarters of 2023 were in commercial property coverage. Those rate increases were primarily driven by losses from natural catastrophes, a lack of reinsurance capacity, and lingering effects of inflation. Commercial auto and umbrella also experienced strong pricing growth for similar reasons. Cyber, once the business line with the fastest-rising premiums, settled into a below-average rate of pricing growth through 2023.

2024 Economic Outlook

Forecasters are much more optimistic about 2024 than they were going into 2023. The Federal Reserve Bank of Philadelphia’s Fourth Quarter 2023 Survey of Professional Forecasters shows a median forecast of 1.7% real GDP growth in 2024, compared to the 0.7% forecast for 2023. Inflation is much lower than it was a year ago, unemployment has remained low, and the Fed appears to be finished raising interest rates.

This does not mean there are no concerns regarding the economy. The Philadelphia Fed’s fourth-quarter survey reported a median risk of a negative quarter ranging from 34.7% to 40.9% for each quarter of 2024. This is better than the survey results from a year prior but still far from a guarantee of clear sailing.

Market Conditions

Brokerages Remain Attractive to Investors

While the number of M&A transactions for insurance brokerages has decreased for two years in a row, the business of insurance distribution remains resilient during challenging economic times.

Organic growth in 2023 across the insurance brokerage industry, driven by the hard market and premium rate increases, rivaled previous highs from the past two years. In 2023, public brokerages averaged 11.2% organic growth (outperforming 9.7% growth in 2022 and 10.7% in 2021), while all agencies averaged 8.9% growth (slightly below 9.3% from 2022 but outperforming the 8.1% growth of 2021).

Meanwhile, valuations continue to rise, driven by the need for expertise at high-performing platform organizations. Valuations on the upfront base purchase price for average firms and platform firms, for the 12-month period ending in fourth-quarter 2023, both increased from year-end 2022. The total purchase price potential for maximum earnout for platform firms was up 14.3% year over year (from 16.35x to 18.68x), and the overall average for all firms rose 7.8% (from 13.78x to 14.85x).

Is this the peak for valuations? Maybe for average firms. Yet, despite this nearly two-year stretch of suboptimal economic conditions, valuations for average insurance brokerages and platform firms are at all-time highs. What does all this mean? It means buyers will still pay higher multiples for high-performing platform organizations and that the insurance industry is resilient—even in the toughest times.

The Road Ahead

The employee benefits (EB) and consulting industry continues to change, forcing organizations to bolster their expertise, client service delivery, and resources to help clients achieve their benefits goals.

Buyer demand and seller supply both have the potential to increase in 2024, with valuations remaining at or near their elevated levels. However, any increase in supply and/or demand will be influenced by different factors.

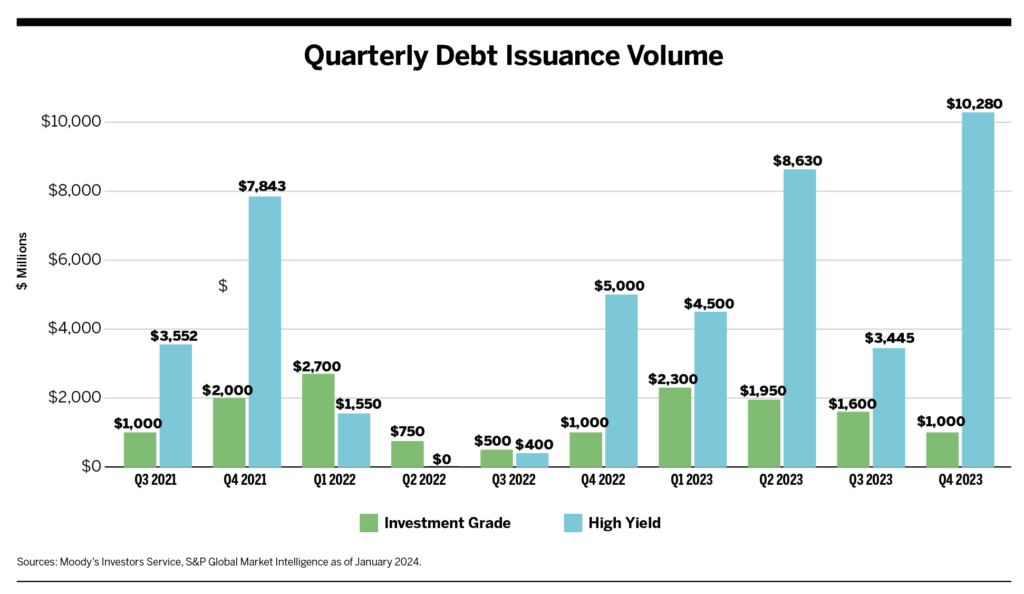

For buyers, the primary factors driving activity will be any Fed interest rate cuts and increased access to debt. Right now, the debt markets are friendlier to buyers. Even at higher interest rates, relevant to the amount of debt a buyer can borrow, leverage ratios are creeping back up to above 7x—like the good old days of 2021.Debt capacity is rising, while debt pricing will hopefully drop at some point. Private-equity backed buyers raised a significant volume of high-yield debt in 2023—estimated to be near $27 billion, compared to $7 billion in 2022. A softer economic environment in 2024 may be just the excuse buyers need to ramp up acquisition strategies and to deploy capital.

Additionally, private equity will continue to play a huge part in insurance industry consolidation. This trend has been building for several years, as PE has seen exceptional returns in this industry. Right now, eight to 10 PE-backed brokerages might be looking for a new partner. Expect several large buyers to recapitalize, restructure or merge in 2024.

For sellers, the drive to provide better client service remains a theme across the independent landscape. The end client continues to demand more from their brokerage and access to industry knowledge, data and analytics, loss control and claims services, or even broader solutions (e.g., human resources consulting, retirement planning, individual wealth)—which are becoming a cost of entry to remain competitive. Independent firms are weighing their options as to whether they need to build these services on their own or partner with a firm that has already made the investments.

Additionally, concerns are starting to grow around the scheduled expiration of the Tax Cuts and Jobs Act (TCJA) of 2017 (aka the Trump tax cuts) at the end of 2025. This sets up the potential for ordinary income tax rates to go up in 2026, which would affect most Americans and corporations.

Potential sellers may start to look toward the upcoming presidential election, the expiration of the TCJA, and how lawmakers will address possible tax increases as factors that could influence considerations for a transaction in 2024 and beyond.

So, while demand for quality firms has been the theme over the past few years, this year could provide macro events impacting the psyche of both buyers and sellers—likely determining the overall volume of M&A activity in 2024 and 2025.