2023 Insurance Brokerage Deal Roundup

Who was buying? What was bought?

Who Was Buying?

Private-capital backed buyers accounted for 576 of the 807 transactions (71.4%), a 12.1 percentage point increase from 2019 when those buyers accounted for 59.3% of all transactions. Independent buyers accounted for 126 deals, 15.6% of total transactions in 2023, a 6.7-point decrease from the 22.3% of independent deals in 2019. Transactions with banks as buyers also continued to fall, from 18 transactions (2% of all deals) in 2022 to nine (1.1%) in 2023, an all-time low.

The top three most active U.S. buyers in 2023 were BroadStreet Partners (47 deals), Inszone Insurance Services (45 deals) and Hub International (39 deals). This marks Inszone’s first year and Hub’s second consecutive year in the top three. The three companies’ combined transactions (131) accounted for 16.2% of the 807 total transactions, while the top 10 most active buyers completed 41.9% of the total (338).

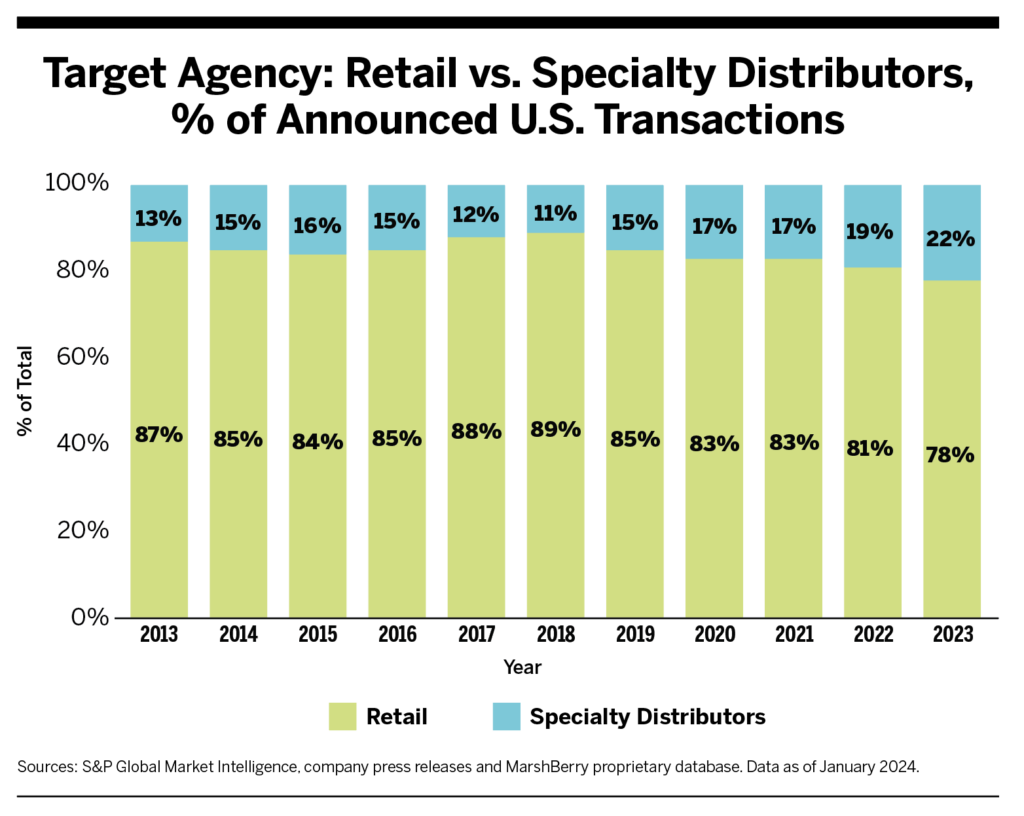

What Was Bought?

Specialty transactions totaled 22% of the total market for 2023, 181 deals in all. Both figures represent all-time highs, compared to the previous transaction count record of 179 in 2021 and the 19% market-share high from 2022. Specialty transactions have increased at a compound annual growth rate (CAGR) of 18% since 2018.

Acquisitions of P&C brokerages accounted for 431 deals (53% of the total), down from 472 in 2022 but consistent with 52% total market share for that year. Employee benefits (EB) and consulting firms accounted for 173 deals, representing 22% of the total (versus 24% in 2022), while there were 203 transactions for multiline brokerages, representing 25% of deals (versus 24% in 2022).

Brokerage Buyers

April 11: Arch Insurance announced the acquisition of Thimble, a prominent insurtech platform catering to small businesses and agents. This acquisition enhances Arch’s digital solutions for small business clients and brokerages.

June 5: Hub International announced the acquisition of the employee benefits assets of Horan Associates and Horan Smart Business, collectively known as Horan Health, a significant privately held insurance and financial services organization in the Cincinnati tri-state area that provides employee benefits solutions to over 650 small and midsize companies. This acquisition resulted in the establishment of a new regional hub named Hub Heartland.

June 30: Risk Strategies announced the acquisition of First Insurance Group from Premier Financial, a community banking and financial services holding company based in Defiance, Ohio. First Insurance Group is one of the largest multi-line agencies in Ohio. The agency continues to operate as First Insurance Group, a division of Risk Strategies.

Aug. 1: Marsh McLennan Agency, a subsidiary of Marsh, acquired Philadelphia-based Graham Co., a prominent risk management consultancy and one of the leading U.S. independent insurance and employee benefits brokerages.

Oct. 24: Gallagher announced its acquisition of the insurance operations of Cadence Bank (Cadence Insurance). Cadence Insurance was the second largest bank-owned insurance brokerage in the United States and among the top 50 brokerages in the country. Nov. 2: Hub International announced the acquisition of Columbus, Ohio-based Overmyer Hall Associates, one of the largest P&C insurance agencies in the state. It specializes in the construction and real estate industries.

Dec. 14: AUB Group announced its strategic investment in Miami-based reinsurance brokerage Mexbrit. AUB Group is an Australian general insurance brokerage network operating in 570 locations globally. Mexbrit is an independent reinsurance intermediary specializing in the Latin American and Caribbean markets. This investment also includes Forte Underwriters, a specialty underwriter focused on the Latin American insurance market. This is AUB Group’s first acquisition in a U.S. brokerage.

Dec. 20: Aon announced the acquisition of NFP, a middle-market provider of risk, benefits, wealth and retirement plan advisory solutions, from funds associated with Madison Dearborn Partners and HPS Investment Partners for an estimated $13.4 billion. This transaction expands Aon’s presence in the middle-market segment, with an opportunity to enhance distribution through Aon’s Business Services platform. The transaction is expected to close in mid-2024.

PE Investment

Feb. 17: Top-20 U.S. brokerage firm Peter C. Foy Insurance Services (PCF) secured a $500 million preferred equity investment. This transaction was co-led by Carlyle’s Global Credit platform and private equity firm HGGC, an existing minority investor. Additionally, PCF received significant investment participation from funds managed by Owl Rock, a division of Blue Owl, and Crescent Capital, both of which already held minority equity stakes in the company. PCF’s valuation at the time of investment was $4.7 billion.

April 3: Truist sold a 20% stake in Truist Insurance Holdings to funds managed by PE-firm Stone Point Capital, for $1.95 billion. The Truist subsidiary is the sixth-largest insurance brokerage in the United States. The transaction valued Truist Insurance Holdings at an aggregate of $14.75 billion. In February 2024, Truist announced an agreement to sell the remaining 80% to an investor group led by Stone Point and Clayton, Dubilier, & Rice, valuing the company

at $15.5 billion.

Sept. 11: USI Insurance Services announced that Kohlberg Kravis Roberts (KKR), an existing shareholder, would make a new equity investment of over $1 billion in the company. As part of the agreement, KKR and USI will acquire shares from Caisse de dépôt et placement du Québec (CDPQ) and other investors, with KKR becoming the largest single shareholder upon completion of the transaction. Despite this change, USI’s management and employees will maintain significant ownership in the company.

Sept. 26: Corsair, a New York-based private equity firm targeting payments, software and business services, sold its majority stake in Oakbridge Insurance to Audax Private Equity. Audax in turn announced a partnership alongside management to invest in Oakbridge. This is Boston-based Audax’s first investment in the U.S. insurance brokerage industry.

Nov. 27: Lightyear Capital announced a “strategic investment” in Inszone alongside existing investor BHMS Investments. BHMS will not only retain a substantial portion of its current equity in Inszone but will also invest additional capital. With a history of investing in U.S. wealth management firms, this marks Lightyear’s first investment in the U.S. insurance brokerage industry.