Private Capital Remains Most Active

The 576 deals last year from private-capital backed buyers sustained their multiyear trend of dominating insurance distribution M&A. These buyers’ acquisitions increased by an 8.9% CAGR from 2019 to 2023. Despite tightening access to capital and higher interest rates in 2023, private capital remains interested in insurance distribution because of the industry’s resilience through all market conditions and its strong financial results.

Private-capital backed buyers included 52 unique insurance brokerages, plus 16 “other” types of capital-backed buyers, such as investment firms and private-capital backed insurance companies. That was a slight reduction from 52 unique brokerages and 18 “others” in 2022, but there is still a relatively tight concentration of buyers compared to the total number of transactions.

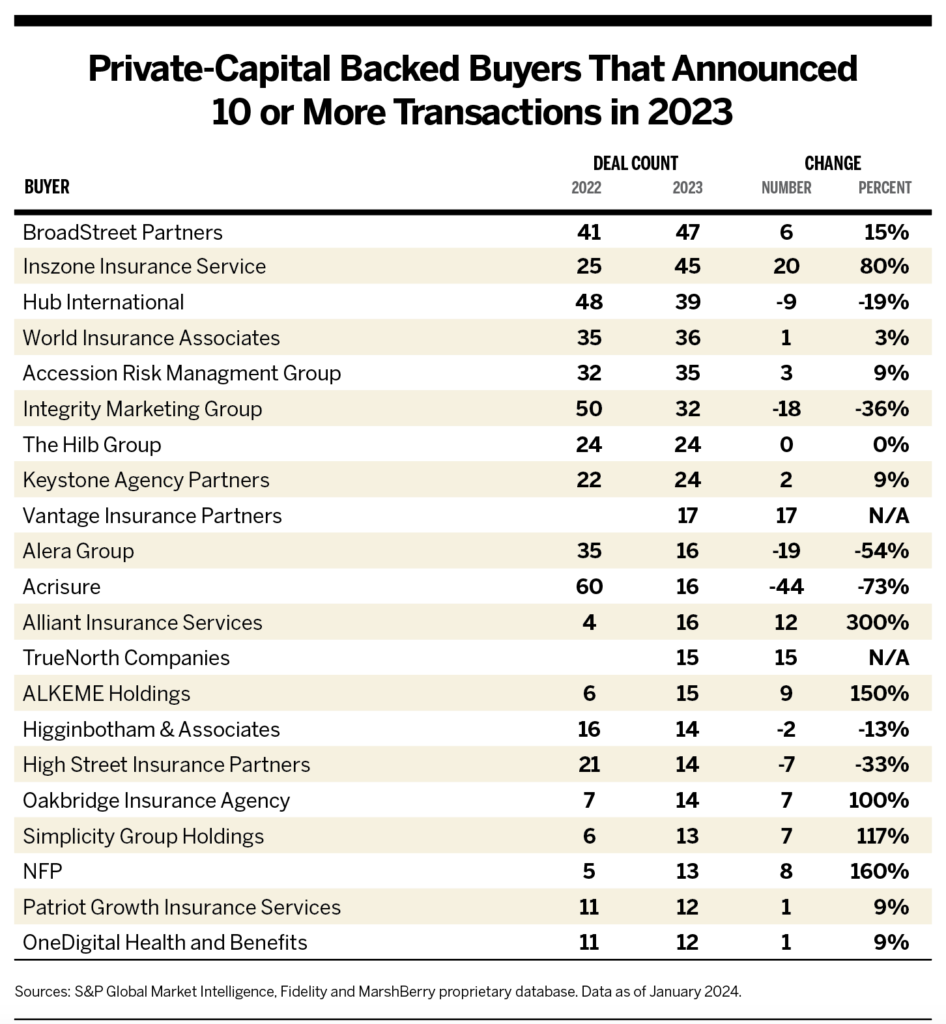

There was a shift in buyer concentration: 21 private-capital backed firms completed at least 10 transactions during the year, compared to 19 buyers with 10 or more deals in 2022. Among those 21 buyers, only six firms announced fewer deals in 2023 than in 2022.

Experienced Buyers Stay on Pause

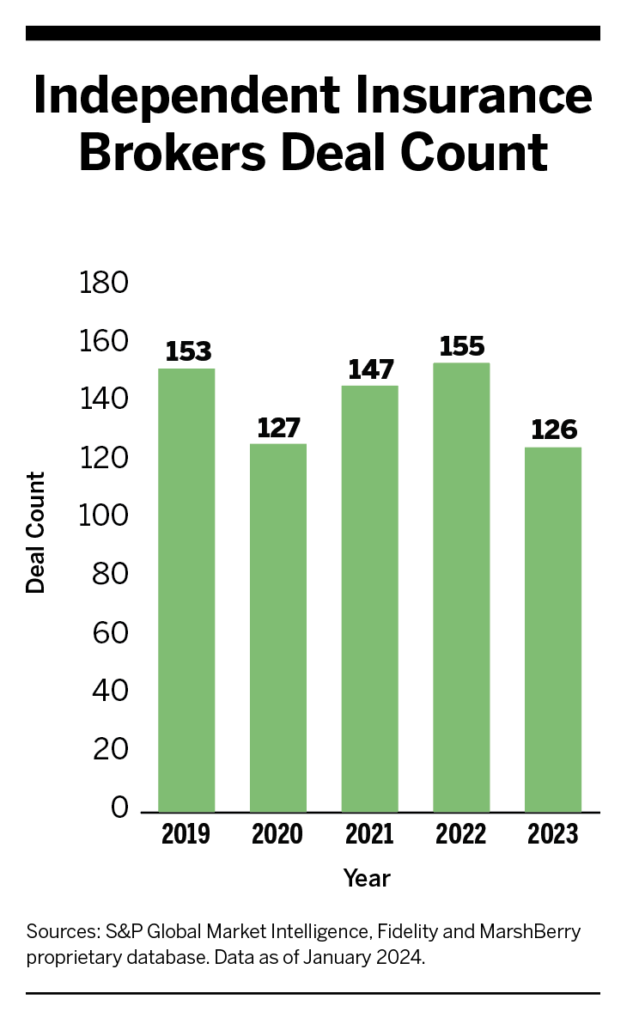

In 2023, 171 buyers announced completing at least one transaction, a significant decrease from 211 buyers in 2022, 212 in 2021 and 224 in 2020. The number of firms that completed two or more transactions dropped from 81 in 2021 to 68 in 2022 to 67 in 2023. This could mean that experienced buyers remained less active in the market in 2023 after taking a slight breather in 2022 due to the challenging macroeconomic conditions following a record-high year in 2021.

However, the financial community still sees insurance brokerage firms as a great investment, and demand remains high. While 2023’s overall deal count decreased by 11% from 2022, it was still the third most active year on record and on par with the five-year period prior to 2021.

U.S. Buyers Continue International Expansion

U.S.-based buyers also remained active in Europe, growing their deal activity on the continent at a 37% CAGR from 2019 to 2023. Expanding their insurance-brokerage footprint into new territories represents a large component of these firms’ growth strategies.

Independent Firms Are Least Active

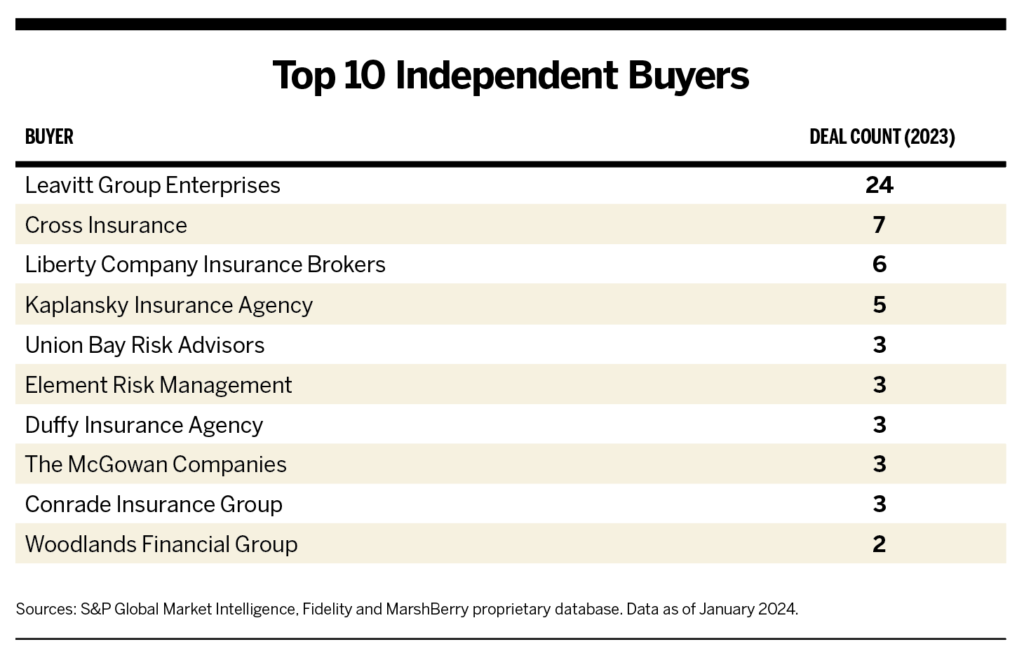

Alongside this sector’s smaller cut of the overall deal count in 2023, 71 different independent firms without known private-capital backing announced transactions last year, compared against announcements by 90 firms in 2022. Ten of the 71 independent acquirers accounted for 60 announced transactions—47.6% of the total buying activity for this segment.

In 2023, 56 independent buyers completed only one transaction, compared to 73 single-transaction buyers in 2022 and 75 in 2021. This could indicate a trend of lower deal activity among independent firms, which conceivably are less able to compete on price with their private-capital backed and publicly traded counterparts, as multiples remain high for quality companies. However, there have been hundreds of buyers in this segment during the last 10 years, and it’s likely that the number of transactions is much higher than publicly known, as many local deals are not announced.

Banks Retreat from Insurance Brokerage

The pullback of transactions by banks—from 25 in 2021 to 18 in 2022 to nine last year—showcases a 15-year trend of reduced bank interest in buying insurance brokerages. In 2007, these transactions represented approximately 21.7% of total announced insurance brokerage M&As. That percentage dropped to 6.4% by 2012 and to just 1.1% in 2023. In fact, last year there were more divestitures of insurance brokerages by banks (11) than acquisitions (nine).

With increasing insurance brokerage values over the last decade, coupled with the recent pressure on bank balance sheets due to Federal Reserve tightening of credit and increases in the discount rate, regional banks are looking more closely at the role insurance plays in their business. Additionally, banks have looked to increase capital as Fed credit-tightening and rising interest rates pressured their investments.

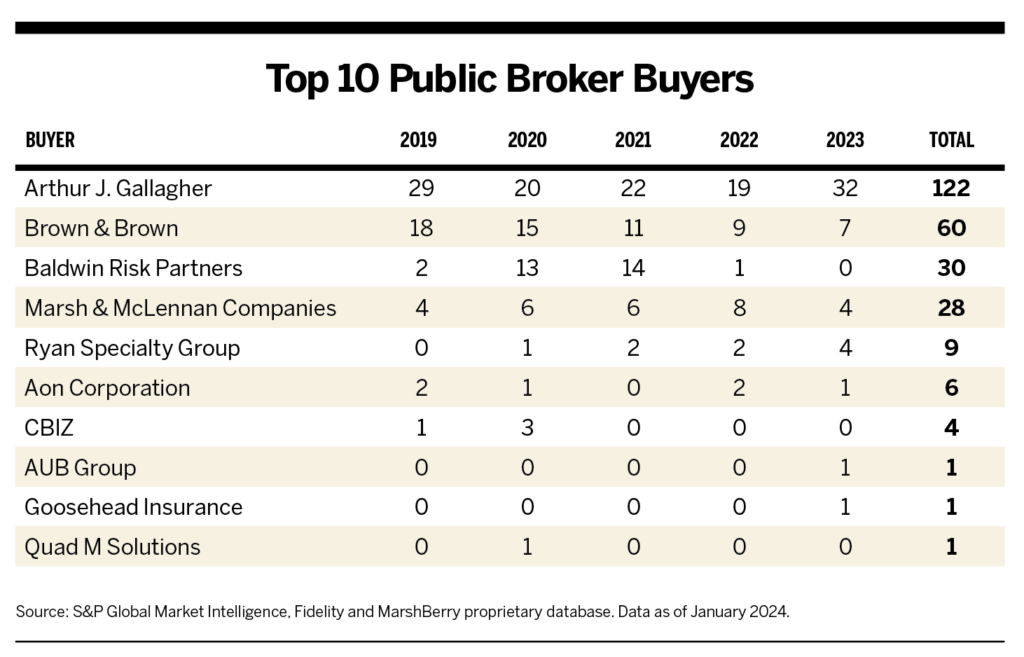

Public Brokerages Drive Growth Through Acquisitions

Public brokerages announced 50 deals in 2023, roughly 6.2% of the total transaction count for insurance brokerages (versus 4.5% in 2022 with 41 announced acquisitions).

As in 2021 and 2022, Gallagher was the most active buyer; its 32 deals comprised 64% of the announced transactions from this group. Gallagher chairman and CEO Patrick Gallagher cited “a very strong merger pipeline” during the company’s third-quarter 2023 earnings call, noting around 45 term sheets signed or being prepared.