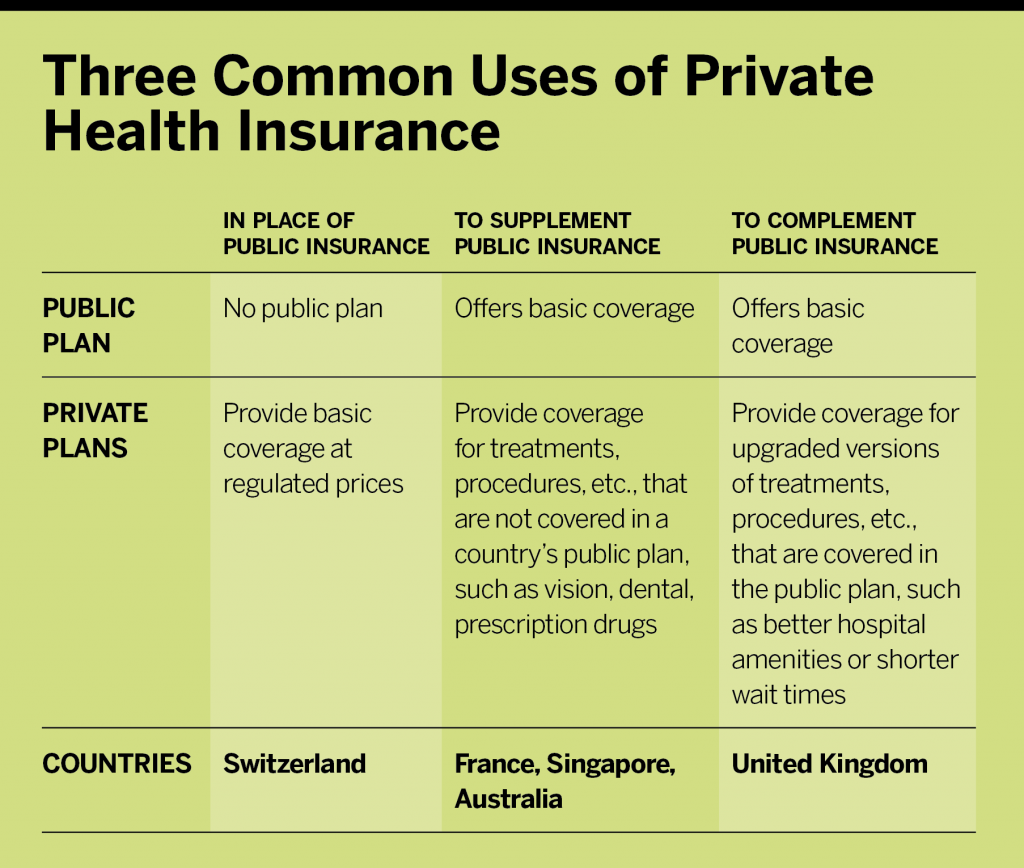

Does Complementarity Work?

While public/private hybrid health insurance may provide basic care, employer coverage brings the perks.

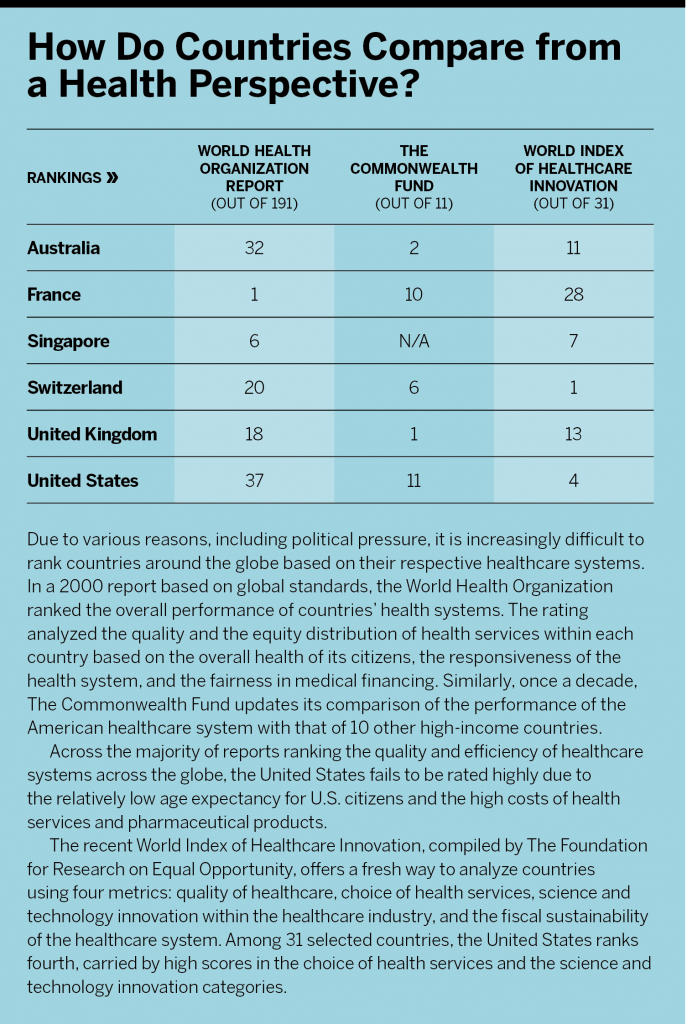

The United States’ healthcare system is often compared with those of other countries that have mandated universal health coverage, and the system’s efficiency (or lack thereof) has long been a topic of debate in national and international forums.

A comparison of healthcare systems across the globe shows the efficiency (or lack thereof) of the American model.

Singapore’s healthcare system is often considered a model for balancing universal healthcare with a competitive private market.

In Switzerland, most employers do not provide health insurance, though it’s a common practice among multinational companies based there.

In the United States, says Jeffrey Capone, principal of global business solutions at Mercer, “the traditional employee benefit market continues to evolve, in part due to the consolidation of major health systems. With fewer options, employers and those individuals who buy their health insurance on a direct-pay basis have limited options in many parts of the United States. This consolidation also challenges health carriers in their pricing negotiation efforts with these health systems.”

Are other countries more effectively providing for the health of their people? We took a look at how five other countries—Switzerland, France, Singapore, the United Kingdom, and Australia—fund and regulate healthcare to see where they land in terms of cost, quality and access to care.

Switzerland’s Rising Insurance Premiums

Unlike many European countries (but similar to the United States), Switzerland has left a large portion of the health insurance sector under private enterprise. The government does mandate, however, that residents purchase basic health insurance coverage from private insurers. If an individual fails to purchase the mandated health insurance within a three-month deadline, the local authority signs that person up for a plan that might charge higher premiums.

When it comes to the mandatory insurance, the Swiss government is strict on regulating the market. For example, coverage requirements are set by law (and are thus identical across all providers). Benefits include 80% to 90% of medical costs, including most physician visits, hospital care and pharmaceuticals. Also, by Swiss law, health insurers must accept all health insurance applications for the mandatory insurance regardless of an applicant’s age or health risks and without stipulating any conditions or a waiting period. Insurers are also required to offer a minimum annual deductible of $334 (CHF300) for adults and a minimum deductible of zero for children up to age 18. Finally, insurers are not allowed to make any profit from the sale of the basic health insurance, though they can profit from supplemental coverage.

In addition to the mandatory health coverage, insurers can offer supplemental plans for services that are not covered by the basic health insurance, to secure greater choice of physicians, and to ensure better hospital accommodations. Given the country’s focus on individual health coverage, most employers do not offer health insurance coverage for their workforce, though it’s a common practice among multinational companies with foreign workers based in Switzerland. Such employer-sponsored plans generally offer additional employee perks.

Despite the Swiss government’s regulatory control, insurance premiums for the basic health insurance coverage can vary from one insurer to another based on deductibles, place of residence, and the degree of supplementary benefit coverage chosen.

Worryingly, however, the cost of healthcare services in Switzerland continues to increase drastically. According to a 2017 report from SantéSuisse, the country’s healthcare costs rose by 4.9% in 2016. According to EY research, Switzerland’s healthcare costs are expected to grow by 60% by 2030 due to drivers including advances in medical technology, an increasing incidence of chronic diseases, and an aging society. EY notes these factors are creating an unsustainable healthcare system in which many won’t be able to afford the required coverage. The research calls for insurers to work within their means and use technology to develop preventive care and other tools to help people get and stay healthy. As the cost of healthcare continues to climb, so does the cost of health insurance. Since the introduction of basic health insurance in Switzerland in 1996, the average premiums have increased by 4.6% per year.

France Balances Public/Private Market

The French healthcare system, similar to many European countries, offers mandatory national health insurance coverage, which allows French citizens and residents to be covered—from 70% to 100%—for most hospital, physician, long-term care and prescription drug costs. The public insurance system is primarily funded by payroll taxes (paid by both employers and employees), a national income tax, as well as taxes levied on tobacco, alcohol and pharmaceuticals.

Differing from its neighboring countries, however, France also has a well-developed private insurance market that was built to supplement the national healthcare system. In fact, 95% of the population is covered by private medical insurance on top of the country’s national health insurance. Private plans cover co-payments as well as treatments not included in the national health insurance, such as dental, hearing and vision care. Private, for-profit insurers mostly offer this supplementary insurance. Not-for-profit mutual insurers (called mutuelle) also operate in France, mainly providing complementary insurance to the national plan that is not the main basis of support for the system.

Health insurers and brokers are flourishing within the French market, thanks to the country’s recent health reforms. Five years ago, the French government passed the Employment Security Law, requiring all employers to provide private medical insurance to their employees. The law increased both supply and demand, leading to the drastic expansion of private medical insurance in France. Despite this growth, the market for private medical insurance remains under the watchful eye of the French government, which is very involved in maintaining a balanced and affordable public/private healthcare system that remains accessible to all who reside in France.

Since the mandate in 2016, the French government has continuously updated the regulations for the employer-sponsored health insurance market. Failing to comply with these regulations is a large risk within the country, and so are the constant regulatory updates, which lead to less innovation within the market.

In France, says Juliette Kolb, employee and benefits consultant at Verlingue, a French-based insurance brokerage, “the change in private health insurance regulation has limited our product creation. However, we have managed to be even more innovative in order to enable our corporate clients to implement their social strategy. We have built multiple solutions to offset the regulatory requirements. We have developed new services, such as digital tools for HR managers and employees, short- and long-term disability data analysis, prevention measures and many more. We constantly have to adapt our range of services.”

Singapore Focuses on Low Cost Care

Singapore’s healthcare system has often been proposed as a model for balancing universal basic healthcare with a competitive private insurance market. The universal health coverage in Singapore is achieved through a mixed financing system based on three mandatory programs: MediSave, a national medical savings scheme funded by personal and employer salary contributions (8% to 10.5%) for out-of-pocket expenses; MediShield Life, a universal basic health insurance for large hospital expenses funded via the MediSave account; and MediFund, a government-funded safety net for low-income citizens who cannot cover out-of-pocket expenses via MediSave.

Private health insurance in Singapore is available from different health insurers. The most common coverage is through Integrated Shield Plans, which include the MediShield Life component as well as additional coverage from private insurers. These types of plans are approved by the government and can be paid for using MediSave. Patients can also purchase private insurance offered by for-profit insurers, but private plans cannot be integrated with MediShield Life or paid for with MediSave. Because of the many insurance options available, however, the combination of MediShield Life, personal health insurance and employer benefits results in varying degrees of coverage duplication.

We have built multiple solutions to offset the regulatory requirements. We have developed new services, such as digital tools for HR managers and employees, short- and long-term disability data analysis, prevention measures and many more. We constantly have to adapt our range of services.

Juliette Kolb, employee and benefits consultant, Verlingue

The Singapore government is very active in maintaining affordable insurance premiums, reducing out-of-pocket costs, and holding down the cost of prescription drugs through government subsidies. For example, to keep drug prices low, the Ministry of Health publishes an extensive list of drugs that the government believes to be cost-effective and essential. Those drugs are provided at subsidized rates to patients and can be bought with MediSave funds. Drugs that don’t appear on the list may still be available but at prohibitive prices. The government also has strict pricing transparency rules in place, such as including all costs and fees in the total headline price to eliminate drip pricing and mandating fair pricing comparisons.

Given the government’s tight grip on the healthcare system, insurers and brokers in Singapore are limited in terms of prices, which can affect company returns. In fact, according to Statista, underwriting profits of health insurance companies in Singapore have been largely negative since 2014. For example, underwriting profits for health insurers were negative SGD44.2 million (US$33.4 million) and negative SGD11.2 (US$8.5 million) in 2018 and 2019, respectively. Only in 2020 did Singapore’s health insurers make SGD17.9 million (US$13.5 million) in underwriting profit, which may be the effect of COVID-19 on delaying elective and non-emergency services. Thus, innovation and increased efficiency are likely the only routes to gaining a competitive advantage.

UK Public System Crowds Out Private Players

The United Kingdom has one of the largest public sector healthcare systems in the world. Through the National Health Service (NHS), all U.K. residents are automatically entitled to free public healthcare, which includes hospital, physician and mental health care. The majority of NHS funding comes from general taxes as well as payroll taxes paid by both employers and employees.

The private medical insurance market in the United Kingdom is small due to the country’s large investment in the public healthcare system. Private insurance in the country is complementary, offering upgraded options to the public plan including more rapid access to care, choice of specialists, and better hospital amenities but not services. However, only around 11% of the population actually purchases private medical insurance. Of those, only two thirds are covered by health insurance purchased by their employers. In addition to the low demand for private health insurance, the number of health insurers providing cover has fallen over the last 10 years. In fact, according to a 2014 investigation by the British government, four insurers accounted for 87.5% of the private insurance market in the country, with small companies making up the rest. An updated report, released in 2019, showed the top four health insurers in the United Kingdom making up almost 94% of the private health insurance market.

Australia Taxes Employer-Sponsored Health Insurance

Australia also has a universal public health insurance program, called Medicare, which is financed through general tax revenues. Australian citizens, who are automatically enrolled in their country’s Medicare program, receive free public hospital care and substantial coverage for physician services and pharmaceuticals. Similar to France, dental and vision services are not covered by the public health insurance system, so Australians purchase private supplementary insurance to cover those costs as well as expenses from private medical facilities.

Supplementary medical insurance is not widespread, however, as just over half of the population owns any private insurance coverage. “Offering private medical insurance in addition to core funded benefits of group life, disability and income protection is not common when we look across all employment sectors in Australia,” says Michael Atta, head of employee and benefits sales at Honan, an Australian-based insurance brokerage. “Generally, this is offered as a funded benefit by multinationals operating in highly competitive sectors such as technology, pharmaceutical and high-end finance sectors. We are witnessing some increased enquiries due to COVID; however, it still tends to be these primary sectors where cover is offered.

“From a price perspective, private medical insurance is a major expense for individuals and as such is highly valued as a funded benefit. The biggest deterrent to more companies’ offering funded private medical as a core benefit is the high cost of cover due to the government’s fringe benefits tax, which adds significantly to the cost.”

The Australian government, in fact, has a 48% tax on the cost of such products and services for employers that provide fringe benefits to employees because of their employment. Unfortunately for insurers and brokers, paying for an employee’s private health insurance is considered a fringe benefit in Australia.

ESI Leads Private Market

When looking at healthcare systems across the globe, employer-provided health insurance seems to be the most predominant player in terms of private insurance regardless of the presence of universal health insurance coverage (although the presence of a public system generally dampens the employer market). Nevertheless, the heavy regulatory oversight of local governments continues to limit health insurance providers and brokers. In most countries, in fact, health insurers and brokers have little room for differentiation when it comes to insurance solutions and prices, a situation that tends to stifle innovation and competition. In some countries, however, the regulation has served to keep costs affordable for consumers.