Benefits Deals Drop but Desire Remains

Against headwinds, employee benefits firms look for growth opportunities even as their potential acquirers seek diamonds in the rough.

Mergers and acquisitions in the employee benefits (EB) and consulting sector continue to fall, though not for lack of interest in viable businesses.

Through April, 48 transactions have been announced this year for EB-only and multiline firms. That’s down from 60 deals during the same time period in 2025.

As consolidation in recent years has absorbed many scaled, independent employee benefits platforms, today’s market is characterized by constrained supply of EB-only sellers rather than muted buyer interest. This imbalance has reshaped transaction dynamics, making deals increasingly selective and strategic.

At the same time, the costs of health, pharmacy, and ancillary benefits continue to rise. EB brokers face demands for solutions that balance affordability with competitiveness, placing pressure on advisory firms to deliver more sophisticated strategies. Against this backdrop, many EB firms face a fundamental strategic question: whether to identify new, sustainable paths to growth or to seek a partner better positioned to support the next phase of the business.

For smaller and midsize EB firms, this decision is becoming more urgent. Challenges around generating consistent new business, ensuring adequate client-facing resources, and delivering services profitably are converging. The need to invest in expertise, technology, and infrastructure has raised the bar for remaining independent. As a result, fewer of these firms are successfully building those assets on their own, while more owners pursue a sale rather than attempt to scale up in an increasingly demanding environment.

These factors have contributed to a market where deal volume is down but intent remains strong. Sellers tend to be smaller firms seeking stability, resources, or succession solutions, while buyers are highly disciplined in evaluating fit, growth potential, and long-term sustainability.

At the same time, scarcity is driving value at the top end of the market. High-growth EB firms that demonstrate disciplined operations, scalable service models, and a clear growth engine— often supported by technology, data, or specialization—remain highly sought after by both strategic acquirers and private equity sponsors.

M&A Market Update

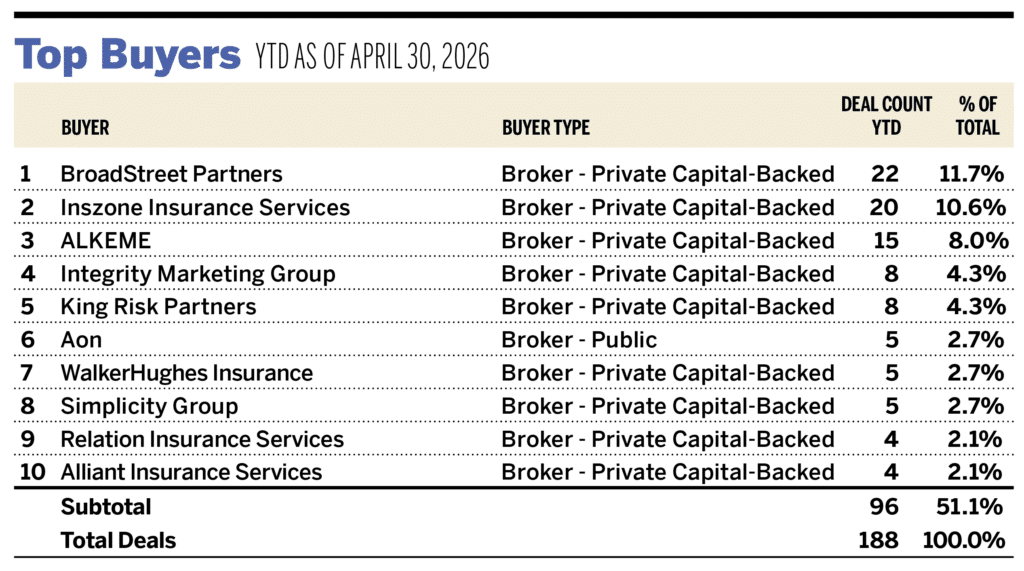

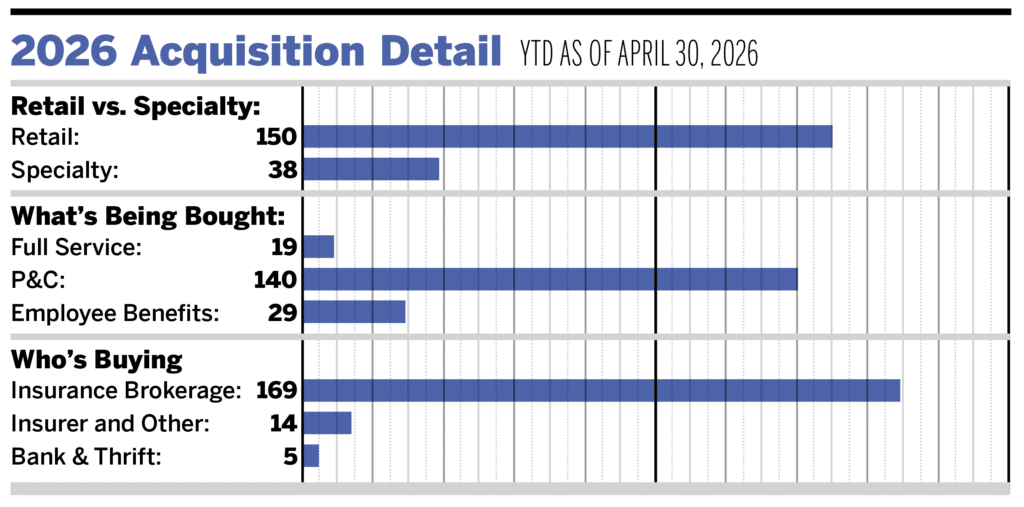

As of April 30, there were 188 announced insurance brokerage M&A transactions in the United States in 2026—down 4.1% from 196 deals announced last year at this time. Private capital-backed buyers accounted for 132 of the 188 deals (70.2%) through April. Independent agencies were buyers in 19 deals, representing 10.1% of the market. Bank buyers have announced five transactions to date this year. Deals involving specialty intermediaries as targets accounted for 38 transactions.

Ten buyers accounted for 51.1% of all announced transactions year to date, while the top three (BroadStreet Partners, Inszone, and ALKEME) represented 30.0% of the 188 transactions.

Notable Transactions

- April 14: Trucordia acquired the assets of JJL&W Insurance Consulting, a Baton Rouge-based employee benefits brokerage, expanding its presence in Louisiana and strengthening its benefits advisory capabilities. Founded in 2020, JJL&W provides consulting and brokerage services across medical, dental, vision, life, and disability benefits, along with support for funding strategies, compliance, and administration for employers and individuals. The firm also manages books of business and provides back-office support for other local agencies. MarshBerry served as advisor to JJL&W in this transaction.

- April 21: Inszone Insurance Services acquired Park ModelManufactured Home Insurance Services, a niche agency specializing in coverage for manufactured and modular homes, marking the launch of a dedicated mobile home division within its platform. Founded in 2017, the firm specializes in owner-occupied homes, rental properties, and specialized structures such as park models and stationary trailers. MarshBerry served as advisor to Park Model-Manufactured Home Insurance in this transaction.