The New Class of E&S Insurers Is Picking Up the Pace

New surplus lines providers are now generating nearly $22 billion in direct premium written, but they have yet to show self-sustaining capital growth.

The rapid expansion of the excess and surplus lines (E&S or surplus lines) sector in the U.S. property and casualty (P&C) industry over the past decade has been impossible to miss.

Perhaps less apparent is the emergence of a new class of E&S insurers during this period and their increasing role in market growth.

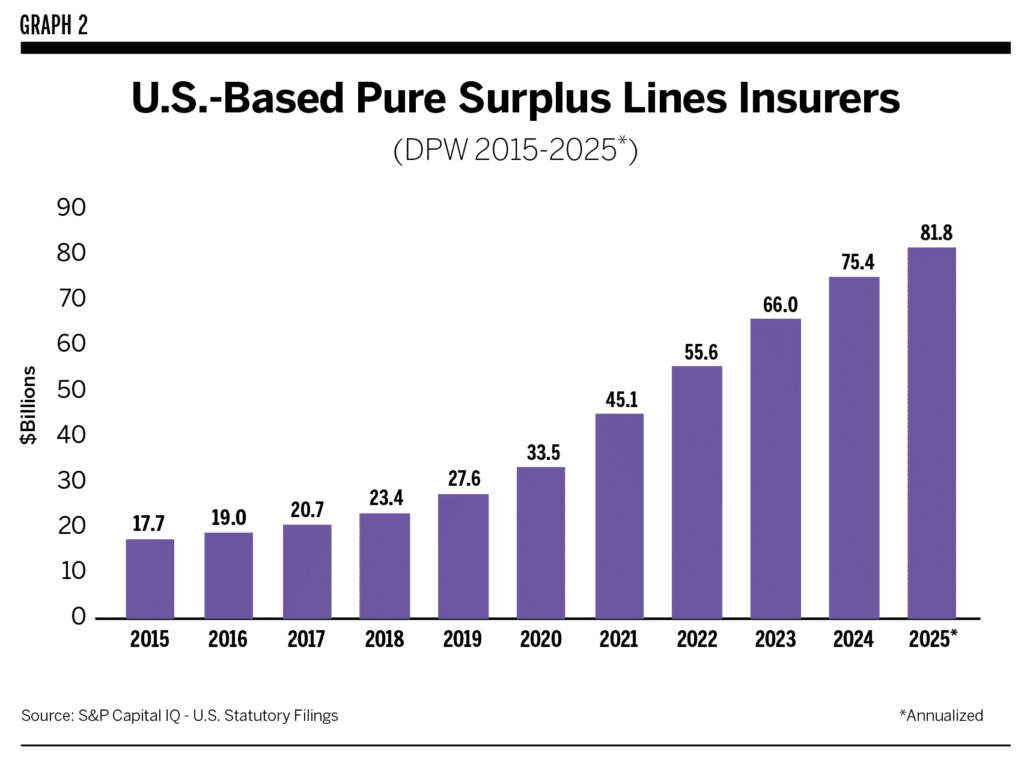

ALIRT estimates that direct premium written (DPW) generated by U.S.-based, dedicated surplus lines insurers (a targeted subset of the carriers represented in the annual AM Best surplus lines report) has grown from just under $18 billion in 2015 to $75 billion in 2024 and an estimated $82 billion in 2025. That growth rate exceeds 4x over the last decade, compared to slightly less than 2x growth reported by the full P&C industry.

The U.S. property and casualty excess and surplus lines segment has grown rapidly over the past decade, from less than $18 billion in direct premium written in 2015 to over $80 billion in 2025. Today, that growth is driven particularly by E&S insurers established since 2016.

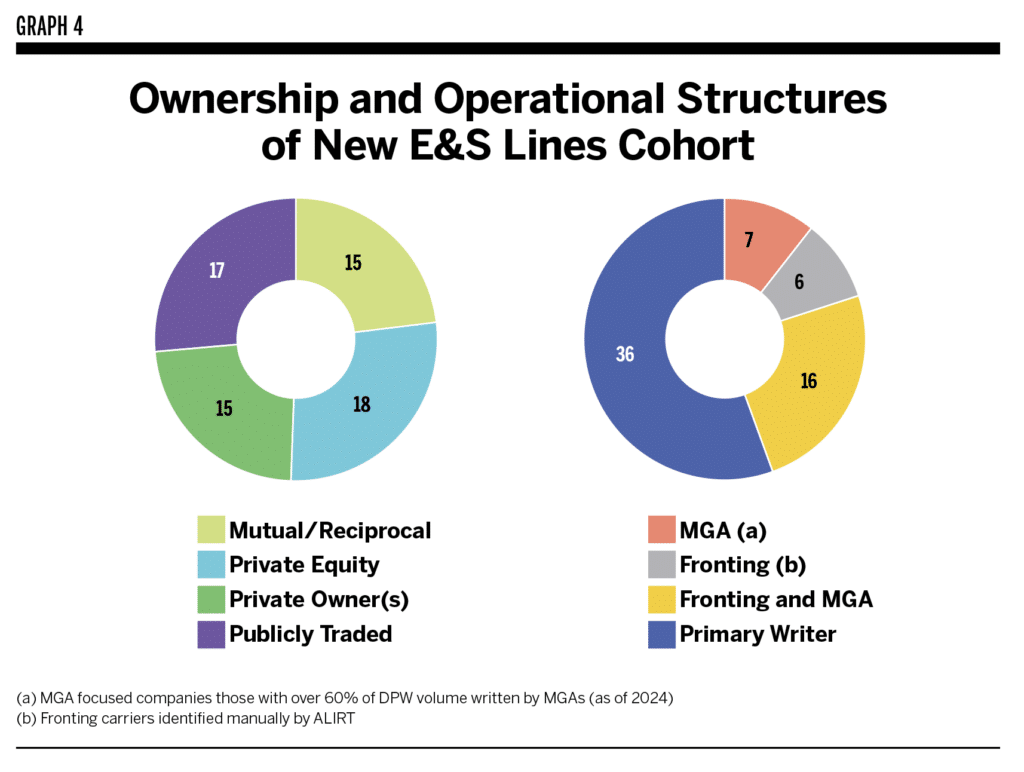

Ownership or financial backing for 65 of these new specialty insurance companies is divided roughly evenly between public and mutual/mutual-type organizations and private equity investments or other privately sourced funding.

The new E&S insurers have not matched their more established competitors’ operating returns, reflecting the impact of rapid growth on earnings and surplus. While they achieved operating profitability in recent years, these newer businesses remain reliant on parent companies for upward of 90% of their surplus.

This explosive growth occurred amid extended hard market pricing in conjunction with a rising number of wholesale specialists (managing general agents and managing general underwriters) often backed by private investment interests eager to put an expanding pool of funds to profitable use. In short, the ongoing need for new and existing insurance coverages abandoned by admitted markets coincided with innovative distribution strategies to supercharge E&S lines growth.

From 2015 to 2019, this expansion was driven by surplus lines insurers that were largely either part of large insurance groups or had been in operation for at least a decade. However, starting in 2016 a new wave of E&S insurance companies entered the market to meet the rising demand for non-admitted coverages. ALIRT isolated 65 new specialty insurance companies that either formed or began operating as E&S-focused insurers over the past decade (the “New E&S Insurer” cohort). This class of E&S insurers’ premium production has accelerated at an astounding rate.

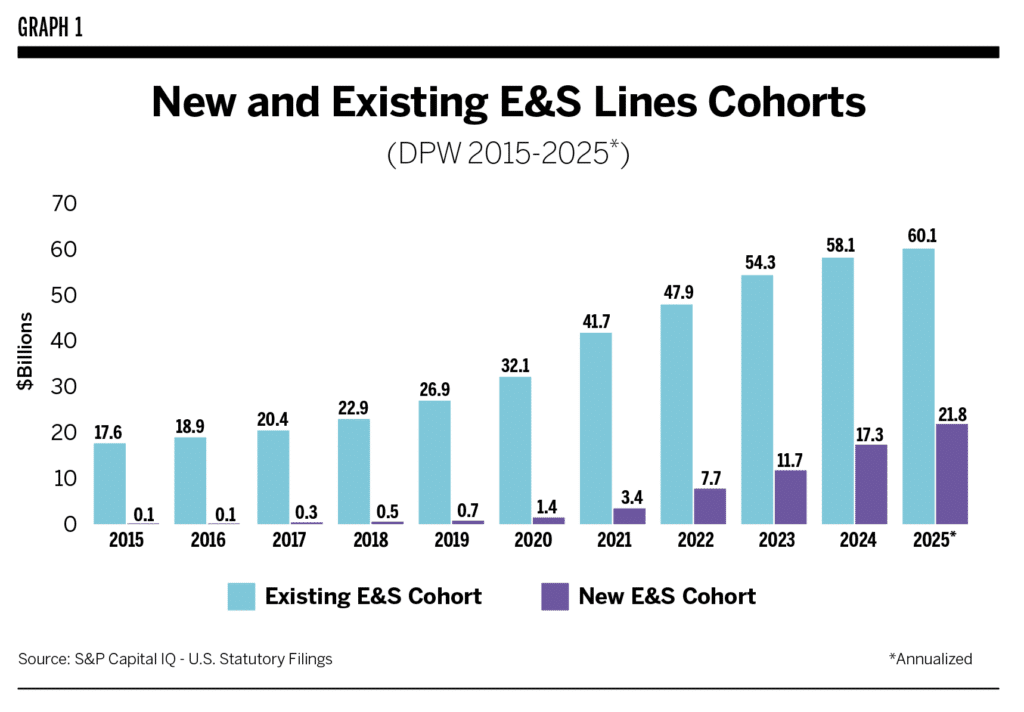

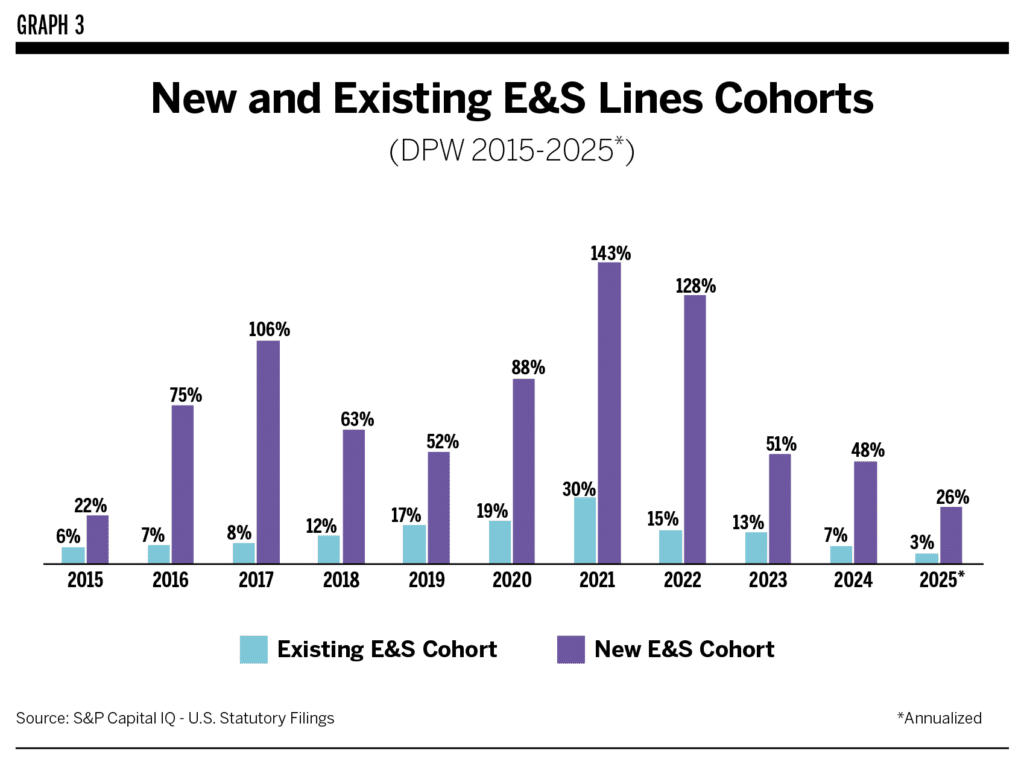

As shown in Graph 1, surplus lines insurers formed prior to 2016 (“Existing E&S Insurers”) accounted for the lion’s share of DPW growth in this market from 2015 to 2019, with the newcomers accounting for roughly 6%. Afterward, the share of business generated by the New E&S Insurer cohort expanded exponentially, from $146 million in 2016 to $1.4 billion by 2020 and $17 billion as of 2024. What’s more, through the third quarter of 2025, new E&S entrants’ DPW was on pace to reach nearly $22 billion—this in a decelerating surplus lines market. (Fourth-quarter 2025 figures were not available at press time.) Put another way, the New E&S Insurer cohort’s share of the total surplus lines DPW has risen from under 1% in 2016 to 26% as of third-quarter 2025.

The dramatic growth is even more pronounced when focusing on more recent trends. Since 2020, this young class of insurers has accounted for 42% of total new surplus lines premium growth. These carriers were on pace to account for nearly 69% of total surplus lines DPW growth in 2025.

Given their increased prominence, it is worthwhile to understand these new E&S insurers and what they mean for the future of the U.S. surplus lines market.

Who’s Who in New Surplus Lines Carriers

Public and mutual/mutual-type organizations are owners, in approximately equal shares, of half of the New E&S Insurer cohort. The other half has been funded by privately sourced money, comprised of traditional private equity (PE) investments and other non-PE funding sources (with the two often overlapping via co-investments). Both are drawn by the potential for premium growth in business lines that require more flexibility on rates and terms and conditions.

The publicly traded parents do not include any of the national U.S. groups, most of which have long owned established E&S lines carriers. Instead, these “new” public parents are primarily represented by either Bermuda/London-based specialty groups or smaller niche U.S. specialty operations.

Of perhaps greater interest is a new ownership trend by mutual or mutual-like organizations such as mutual holding companies (MHC) or reciprocal exchanges.

Several of the largest national mutual groups, including Nationwide and Liberty Mutual, have for decades had a substantial surplus lines presence, but 10 specialty or regional mutual/ MHC organizations added surplus lines capacity over the past 10 years. For instance, Westfield went all in with specialty operations beginning in 2021, including a Lloyd’s syndicate acquisition in 2023.

Five of the New E&S Insurers are reciprocal exchanges, an ownership structure that has grown in popularity over the past decade and is increasingly focused on difficult coastal property insurance markets. Reciprocals have traditionally been admitted carriers, so this is a trend to watch.

No discussion of new E&S lines trends is complete without mentioning the central role played over the past decade by managing general agents/ underwriters (MGA/MGUs), program managers (PMs), and insurers specializing in fronted business.

As shown in Graph 4, a full third of new E&S lines insurers under discussion are fronting specialists— carriers that serve as primary issuers of business but then cede all or a vast proportion of that business to reinsurers. These fronting specialists regularly work closely with MGA/MGU/ PMs that facilitate the reinsurance programs (often based offshore) that ultimately assume the risk.

New U.S. MGA/MGU/PMs have proliferated over the last five years, driven in part by investors attracted by the fee-based model of insurance distributors at a time of hard market pricing and increased specialization in P&C underwriting. While MGAs and MGUs continue to rely largely on legacy third-party carriers to write business, they have found creative ways to directly fund or co-partner with these new specialist insurers to gain greater access to and control over their books of business.

Business Mix

At first glance, new surplus lines insurers’ business strategy mimics that of existing players in the market.

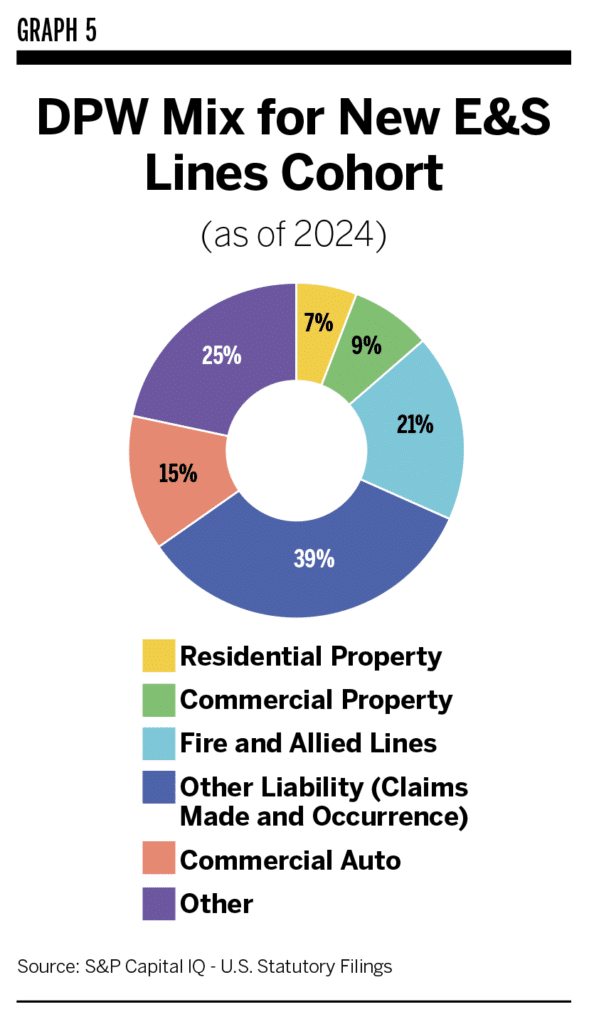

Residential and commercial property coverages, including fire and allied lines, and other liability insurance with a greater mix of occurrence policies than claims-made policies, accounted for 76% of 2024 DPW for New E&S Insurers. Existing E&S Insurers, meanwhile, reported 80% of 2024 DPW in these two segments.

This makes sense as adverse inflationary trends, rising costs of secondary perils, and population growth in high-risk areas are driving upward demand for non-admitted property insurance coverages, especially for high-net-worth individuals and catastrophe-prone regions such as California and the Gulf Coast.

The other liability segment includes a broad swath of commercial policies encompassing general liability, cyber, directors and officers, errors and omissions, and excess casualty. As liability risks become more complex and social inflation trends drive loss costs, the appetite for non-admitted liability coverages in this segment grows.

In 2024, commercial auto represented 15% of New E&S Insurers’ DPW, compared to just 4% for Existing E&S Insurers. The bulk of this premium volume was in liability coverage, with a handful of carriers reporting most premiums. Commercial auto remains among the most beleaguered lines in the commercial lines segment, so a growing opportunity for non-admitted alternatives comes as little surprise.

Financial Performance and Credit Quality

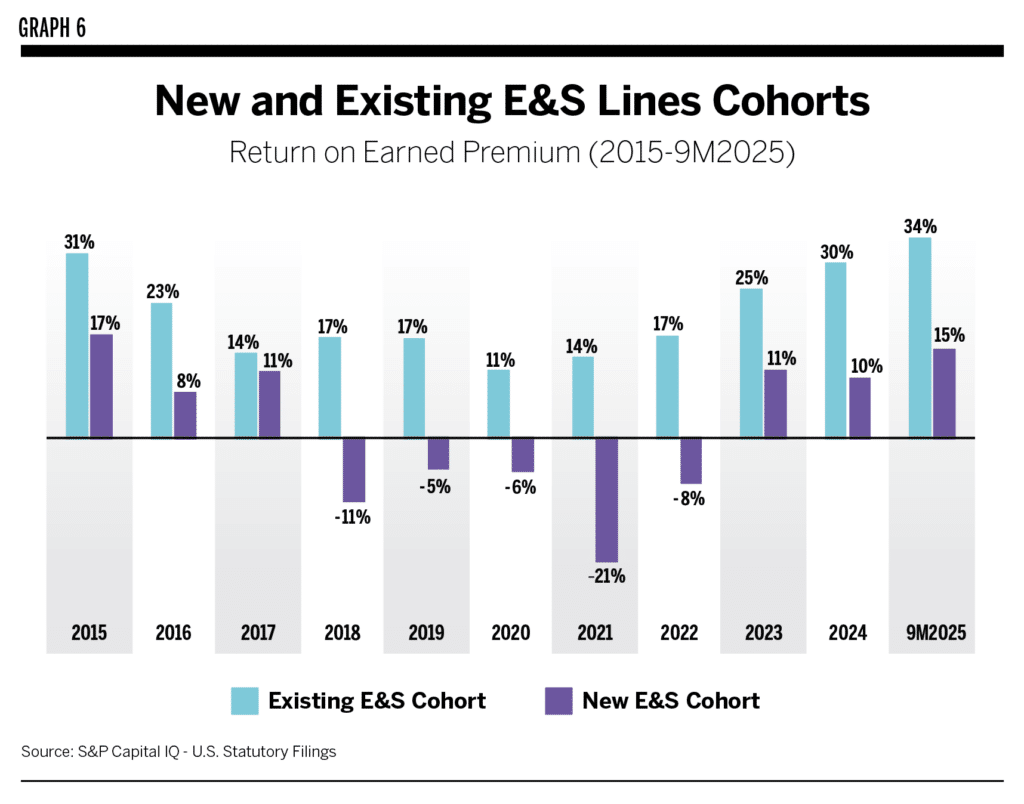

U.S.-based surplus lines carriers have generally reported strong underwriting and operating returns over the past decade, including a dramatic uptick in profits in recent years and the first nine months of 2025. However, as shown in Graph 6, Existing E&S Insurers have reported the strongest results, while the New E&S Insurer cohort has reported substantially lower operating returns.

This reflects their generally weaker underwriting results, especially from 2018 to 2022, in part due to these newer entrants’ rapid growth, which strained earnings and surplus.

Still, new entrants returned to operating profitability in 2023, 2024, and through the third quarter of 2025, suggesting the cohort is maturing.

However, even with improved underwriting and operating earnings, almost 90% of surplus through Q3 2025 for these new E&S lines carriers represents funds contributed by parent companies. These outside capital commitments have been crucial for new E&S businesses to maintain adequate capitalization and credit ratings.

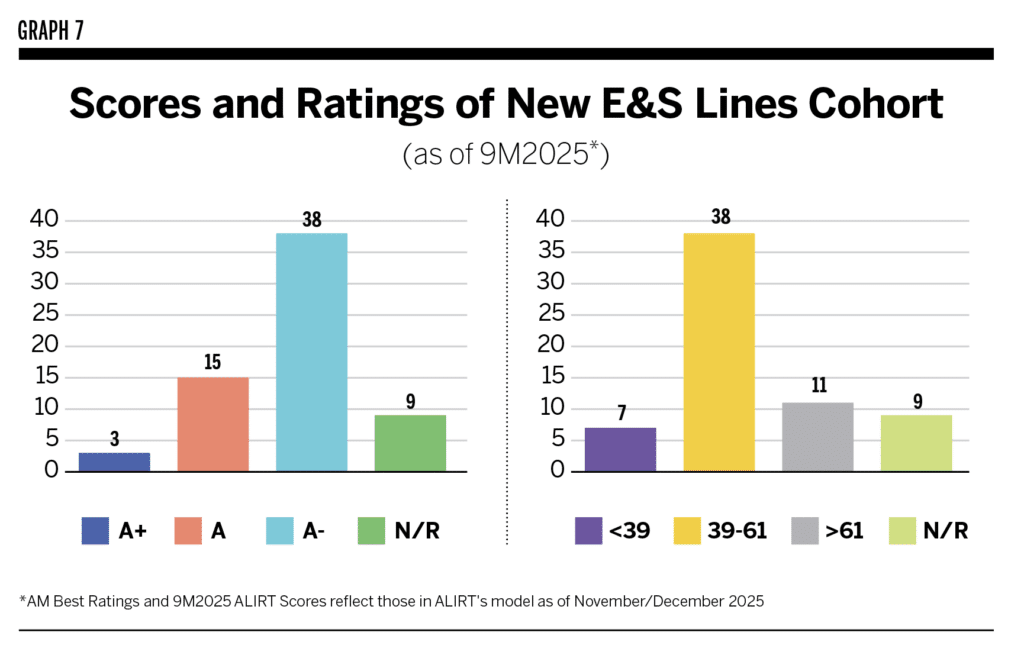

Largely favorable financial results since 2023, continued outside capital infusions, and seasoned management teams have generally resulted in positive credit ratings for the new E&S lines cohort, with the vast majority rated A- or higher by AM Best.

The New E&S Insurer cohort on average scored 49 and 51, respectively, at year-end 2024 and third-quarter 2025 on ALIRT’s credit analytics. These scores are well within ALIRT’s historically normal score range of 39–61 and relatively close to scores reported by existing E&S carriers in both periods (56 and 55).

All told, this new cohort of surplus lines carriers remains financially sound but has yet to consistently grow capital in a self-sustaining manner.

Here to Stay

Several years ago, a commercial lines market head at one of the country’s largest brokers told us that he “needs another new, A- rated specialty insurer like a hole in the head.” While said (mostly) in jest, his comment reflected the difficulty distributors were having in digesting the spate of new entrants to the U.S. surplus lines arena. Brokers and agencies have sought for at least a decade to reduce the number of carrier markets they work with. The rise of smaller niche insurers, often writing programs producers “just need to have,” has instead forced them to expand their list of partners.

This new class of surplus lines insurers is a phenomenon that no retail agency can ignore given the ongoing fragmentation of the P&C market into ever more finely targeted underwriting niches. In sum, the reshaping of the E&S market over the past decade is here to stay.

That said, this reshaping occurred under specific conditions: an easy money environment combined with an extended hard market and record property insurance losses. Arguably, these conditions have eased and, in theory, the number of future surplus lines entrants should slow dramatically.

Data bears out this trend. For example, according to a recent ALIRT study, only two fronting specialists launched in 2024 to 2025 versus 25 in 2020 to 2021. Over half (34) of the new surplus lines cohort under discussion were founded from 2020 to 2022, versus just 12 from 2023 to 2025.

The industry is now likely entering a period of consolidation during which these new carriers will look to scale to a point where they no longer depend on outside sources of capital to support growth. In addition, look for a shuffling of ownership as larger organizations (both insurance groups and distributors) buy instead of build and private equity interests seek investments exits. We are seeing evidence of this already in recent mergers and acquisitions, including FM’s 2025 deal for Velocity Specialty Insurance and Zurich’s pending ownership of Beazley.

In the meantime, these new surplus lines insurers will continue to refine their underwriting models in hopes of further improving operating earnings in an era of slowing growth. Technological innovation and entrepreneurial spirits, extensions of the insurtech space, may continue to favor new entrants over their legacy E&S lines peers.