Optimism in the Face of AI’s Existential Threat

Five reasons to feel good about the future of insurance brokerage, no matter what the market says.

Insurance brokers have received plenty of investor love over the past several years, sending their stocks steadily upward through much of this decade.

But, as we all know, investors can be fickle. Last summer, as softening property and casualty rates caused broker growth to decelerate, their stocks declined sharply, ending the year down 20%–30% from early 2025 highs.

Then, on Feb. 9, our industry had its own “Black Monday.” A sharp sell-off of public broker stocks was triggered by the announcement that Insurify had launched an app enabling consumers to compare and purchase auto insurance within ChatGPT’s AI platform. By day’s end, the five largest public brokers lost an average of 9% of their market value.

Industry observers were stunned. Why would the market punish public brokers over a personal auto app? Don’t investors know the public brokers cover an inconsequential amount of personal auto, focusing mostly on larger, complex commercial risks and large-employer benefits programs?

The “shoot first and ask questions later” reaction was demoralizing, but it was emblematic of market psychology. So here we stand in early 2026, with broker stocks down 30%–50% from their 12-month highs. After a tough year, many broker leaders are waiting for the other shoe to drop.

Brokers—don’t let the negative momentum of today’s market get you down. It is at the bottom of the market, when accumulated negative sentiment peaks, that psychology is most poised to turn. If history is any guide, moments like this often look obvious only in hindsight. But today’s market may actually offer a unique buying opportunity for public broker stocks.

There are at least five good reasons for optimism:

- Brokers occupy prime real estate in the insurance value chain;

- The broker’s position is well fortified against disruptors;

- As complexity intensifies, professional brokers become more valuable;

- The insurance brokerage model is uniquely durable; and

- AI may be creating a once-in-a-generation opportunity to attract premier young talent.

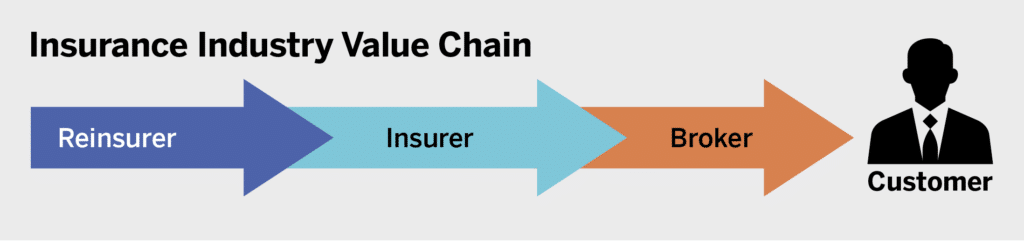

Brokers’ Position in the Insurance Value Chain

Every industry has a unique value chain comprised of players that partner to provide a good or service to the customer. In many industries, the most valuable position in the value chain is closest to the customer. That is especially true in insurance.

Being close to customers allows brokers to understand what clients actually need to manage risk within their organizations, rather than only what they say they need. Clients don’t always fully explain their problems, and they often don’t know exactly what they require until something goes wrong. Through regular contact, real conversations, and involvement in day-to-day decisions, brokers catch small signals early. That leads to better risk management and better client service.

Proximity also builds trust. When clients trust their broker and feel understood, they’re more honest, more patient, and more loyal. When losses happen, and they always do, clients prefer to deal with someone familiar rather than start over with a stranger. Across industries, trust lowers sales friction, improves problem-solving, and significantly improves client retention.

The Broker’s Position is Well Fortified

Because the broker’s position is so attractive, it is constantly under competitive attack. Over the past decade, a steady stream of highly confident, venture-backed insurtech startups have attempted to disrupt the traditional insurance broker.

One of the most outspoken disruptors of its day was Zenefits (circa 2013) and its CEO, Parker Conrad, who promised to revolutionize employee benefits brokerage through its technology. Zenefits attracted enormous attention and capital before running into regulatory and growth challenges and being acquired by TriNet.

Zenefits’ example is one of many that demonstrate the difficulty of dislodging battle-hardened brokers. In fact, a familiar pattern has emerged among aspiring disruptors: they discover that broker-client relationships are stronger than anticipated. With typical retention around 90%, the average broker-client relationship lasts about nine years, making it extremely difficult to penetrate. A nine-year relationship is typically built not just on technical competence, but on trust and often friendship. More importantly, it is reinforced by a broad set of client-facing capabilities.

But today’s concern about broker disruption is more dramatic: it’s not simply a tech-enabled startup, but rather artificial intelligence. Will AI destroy the traditional broker-client model?

Investors spooked by the Feb. 9 ChatGPT announcement seemed to assume this was just the first wave in a new competitive battle. Yet it’s worth noting that broker stock valuation declines to date this year are roughly half those endured by other professional services firms in the legal, accounting, and management consulting sectors. The question investors are wrestling with—industry by industry—is simple: will AI function primarily as a resource or as a competitor?

Across sectors, industry-leading incumbents are working hard to signal that AI will be a resource. For instance, about two weeks after brokerage Black Monday, Hub International publicly detailed that its entire workforce of about 20,000 employees had been using Claude AI since the end of 2025, and that it was already increasing efficiency in select uses. Expect more of these announcements from brokers in the months ahead.

For brokers, the critical question isn’t whether AI boosts productivity—it undoubtedly will. The question is what leaders do with that reclaimed time. Will they reinvest it into deeper relationships, greater specialization, and better client outcomes? If so, AI will likely reinforce the broker’s position rather than weaken it.

That leads directly to the next point.

Complexity of Risk Management Is Growing

The risks facing insureds are becoming harder to understand and manage.

Consider a contractor with 50 employees. Ten years ago, the owner could usually describe the basics of the firm’s insurance program to an accountant or attorney. Today, that’s rarely true. There are more risks, they interact in less obvious ways, and the cost of mistakes is higher.

What has changed isn’t just the volume of risk, it’s the nature of risk itself. Issues that once sat at the edges of the business—cybersecurity, contractual risk transfer, and employment-related exposures—now surface quickly and often without warning. At the same time, as the nature of these risks grows increasingly complicated, most organizations have less internal capacity to step back and think holistically about how to manage them.

As risk continues to outpace clients’ internal capabilities, brokers who combine judgment, specialization, and smart tools will become more important, not less. Artificial intelligence can be part of the broker tool set, but only if used thoughtfully. At its best, AI helps teams absorb information faster, reduce routine work, and support more consistent analysis. The real benefit isn’t efficiency alone, but what efficiency enables: better preparation, deeper specialization, and more informed client conversations.

Brokers’ growing importance is reinforced by the underlying economics of the brokerage model itself.

The Brokerage Model Is Uniquely Durable

Over the past 20 years, a wide range of investors—private equity firms, family offices, and sovereign wealth funds among them—have poured into the insurance brokerage industry. When funds have exited investments to achieve liquidity, many have quickly reinvested in another brokerage.

The reason for such intense investor interest is straightforward. Brokerage economics check nearly every box investors care about: recurring revenue, strong margins, variable expense structures, consistent cash flow, no inventory, no underwriting risk, and resilience across economic cycles and inflationary environments.

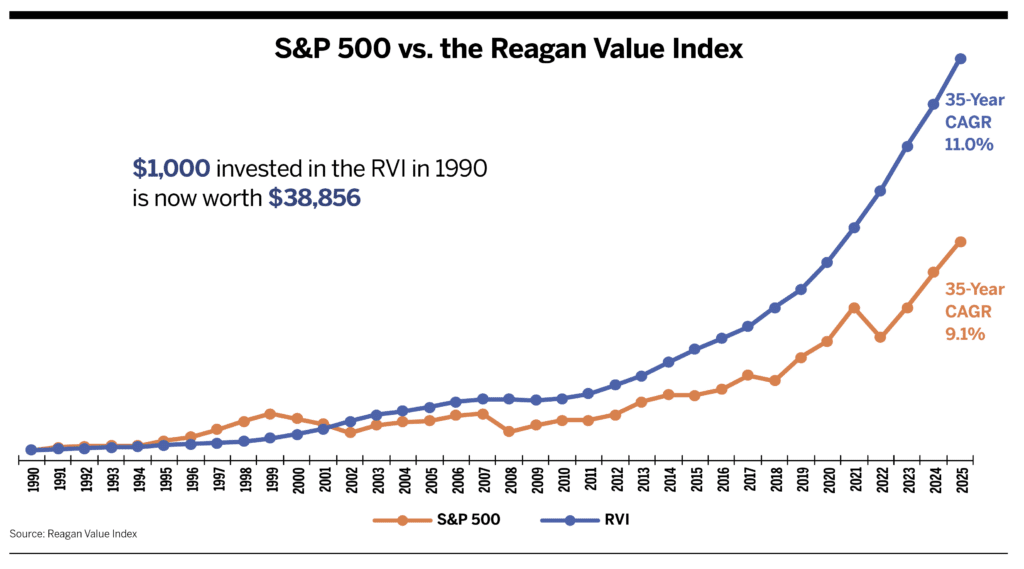

These attributes help explain the industry’s remarkable performance. Private insurance brokers’ average share value has grown at an 11.0% compound annual rate over the past 35 years, versus 9.1% for the S&P 500. While a 1.9% extra return per year might not sound like much, 35 years of compounding makes it enormous. One thousand dollars invested in the S&P 500 35 years ago is today worth $20,957. That same $1,000 invested in the Reagan Value Index—a group of approximately 30 privately held insurance brokers we value annually—is worth $38,856, or nearly twice as much.

But in any case, durability alone doesn’t guarantee future success. Growth also depends on people—which brings us to an opportunity for brokers that is, ironically, being fueled by AI.

AI Presents a Generational Hiring Opportunity

College graduates are struggling to find jobs. According to the National Association of Colleges and Employers, today’s entry-level hiring market is unusually weak—not because of a recession, but because AI has reduced employers’ appetite for “learn on the job” roles. New graduates are competing with midcareer professionals displaced by AI.

At the same time, the insurance industry faces an aging workforce and a long-standing need to attract younger talent. Historically, many young people have favored “sexier” industries like technology or financial services over insurance.

In 2026, the weaker job market for college graduates gives brokers the opportunity to recruit a higher caliber of young talent than at almost any time in memory. But capitalizing on this moment requires more than recruiting to open positions. Brokers must get better at articulating a compelling vision for long-term career growth and professional development.

Many firms have already invested heavily in college internship programs and are beginning to see returns. Those firms are best positioned to benefit from this unusual moment.

A Time for Optimism

There are good reasons to feel optimistic about the future of insurance brokerage— at least for firms willing to invest in themselves. The industry’s core strengths remain intact: durable economics, deep client relationships, and a growing need for judgment as risk becomes harder to understand and manage.

AI doesn’t change that. Used well, it can give brokers back something they’ve been losing for years: time. Time to think, to develop people, and to be more present with clients. The technology itself matters less than how leaders use the capacity it creates. That choice will matter. Some firms will allow productivity gains to disappear into cost cuts or busyness, while others will reinvest in specialization, talent, and growth. Over time, that difference will show. The real risk isn’t sudden disruption, it’s standing still while expectations quietly move on.