Doing Business in Digital Assets

Q&A with Glenn Morgan, Head of Digital Assets, Aon

As digital assets’ role in global finance grows, the insurance industry is getting involved.

Aon, for instance, for the first time recently accepted premium payments in stablecoins. Aon’s Glenn Morgan tells Leader’s Edge how the industry is using cryptocurrencies today, why stablecoins are an essential part of digitization, and how the global broker and the industry are proceeding with digital assets.

Q

How is the insurance industry today using cryptocurrencies?

A

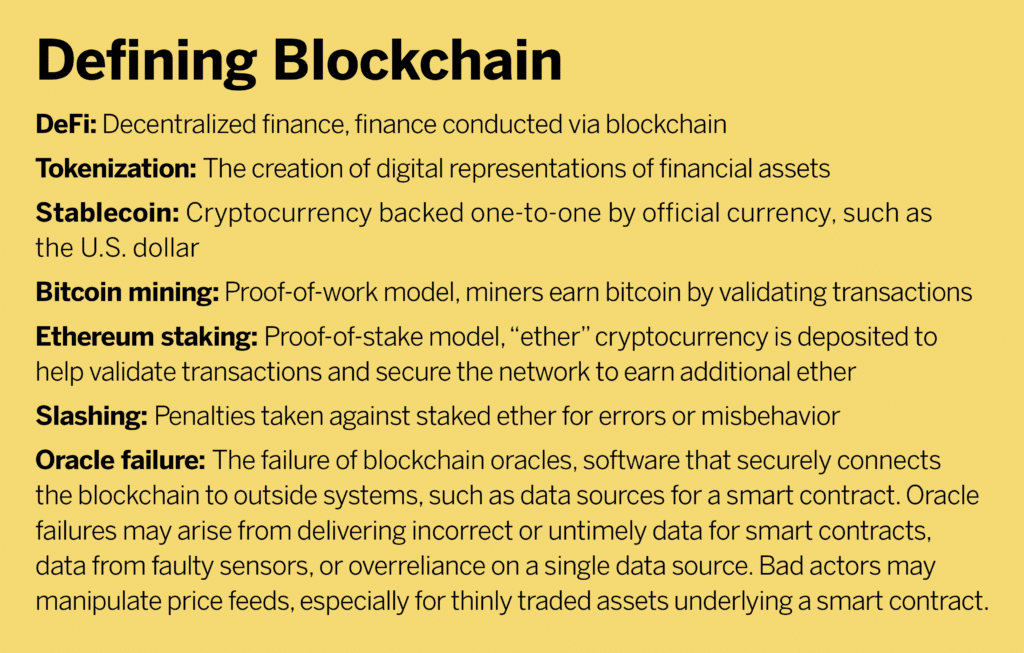

It’s very early innings for the insurance industry in terms of how cryptocurrency is actively being used. You saw from our pilot that cryptocurrency was used to pay for insurance policies. There are a number of insurers that specialize in the DeFi [decentralized finance] on-chain [blockchain] ecosystems. There are certain things that work well, that have an immediate product-market fit for insurance payment solutions backed by crypto. We see parametric products like travel insurance or crop insurance, where it’s dependent on certain weather patterns, where there’s not really much claims adjustment. An event happens and the policy pays, and it could be handled in that smart contract. Where we’re a lot more interested is where crypto can be used as a capital source now, specifically stablecoins or high-cap assets like bitcoin or ethereum, where some insurers will provide insurance natively in the currency that’s the dominant exposure. An example would be a bitcoin-denominated insurance policy for custody of digital assets, or for business interruption for a [bitcoin] miner. If they have something go offline, or they have a property event or loss of compute, the interruption to their business is the lost income in bitcoin that they’re not able to mine, then that asset-matching realm makes a little bit more sense.

Another one that’s getting more popular is ethereum-denominated staking policies. Staking insurance is used to protect you from downtime, missed rewards, and slashing instances [penalties] on proof-of-stake networks. Ethereum, obviously, is what’s driving a lot of the demand right now. If there’s a slashing incident, your loss penalty is denominated in ethereum on-chain. What some insurers are saying is, “Hey, we’ll write you a policy in the asset your losses are tracked to.” Where we could see a lot more adoption is certain regulatory jurisdictions that are accepting stablecoins and other crypto assets as collateral. Depending on what the strategy is, it gives people an additional utility for their digital assets as well as a way to scale capital to support risk that they’re having trouble matching in the open market.

Q

How do stablecoins differ from other cryptocurrencies like bitcoin?

A

You hear all the buzz about tokenization, where we’re putting assets on the blockchain. Stablecoins are effectively the killer app for tokenization right now. It is a real-world asset in dollars. In many cases, this is U.S. dollars, so we’ll use that as an example—U.S. dollars reserved in a bank account that don’t move and a tokenized representation of those dollars that are issued on-chain. They’re backed one-to-one by reserves that are held in bank accounts with large financial institutions, with all the typical safety and security there, and it is a claim to those dollars on-chain that can be trusted, minted, and burned [permanently removed from circulation] as reserves come and go, processed by the stablecoin issuer.

What the GENIUS Act [the new federal regulatory framework for stablecoins enacted in 2025] establishes is how this process can be done safely. It says who can issue a stablecoin. They’re called PPSIs for permitted payment stablecoin issuers. These are the folks that meet the criteria that everybody has agreed to, the guidelines that you need to follow in order to safely issue a dollar on-chain so that when people use stablecoins to interact with different on-chain environments, they can trust that that is pegged one-to-one to dollars that are held in reserve.

It differs from bitcoin, because bitcoin is a commodity. What market value it has fluctuates, whereas a stablecoin is always going to be worth whatever asset is backing it. The SEC [Securities and Exchange Commission] and CFTC [Commodity Futures Trading Commission] recently offered guidance to give a taxonomy between what is a security, what is a commodity, what is a token, how will regulators interpret different types of assets, which is something that we greatly needed. That gives people more official clarity, even though we still need rule makers to actually cement that guidance.

Q

Aon recently accepted the first premium payment in stablecoins from your clients (cryptocurrency platform Coinbase and tokenization firm Paxos). Tell me about that transaction and why it’s important.

A

There are insurers that have contracts, collateral, and other things in stablecoins, but Aon’s the first to natively accept stablecoin payments for premiums that get carried forward to insurers in fiat dollars. These programs involve a lot of different insurers, and what we wanted to focus on is making an easier avenue for our customers to have a payment option in assets that they’re trading in. Coinbase and Paxos are both industry leaders; they elected to pay us with different stablecoins, respectively USDC on the ethereum blockchain and [PayPal] PYUSD on the Solana blockchain. These are things that they’re already doing with other counterparties and something that we see as one of the future pillars of how people will transact value.

When you have an organization like Aon, risk management is at our core. We don’t take any of these things lightly. We have to make sure that we’re aligned from the executive team down through treasury, controllership, finance, accounting, legal risk, compliance, policy, information security. All of these teams were involved to make sure that we were doing this in a safe manner. It was a learning experience. Part of that is that we’re not viewing this [working in cryptocurrency] as an “if,” it’s more or less going to be a “when.” We want to be a leader in our industry segment, not a follower.

Q

What are the advantages of using stablecoins for payments?

A

There’s a whole host of benefits. One of the things that immediately gets cited is low transaction fees. You can make instant cross-border payments, [with] reduced FX [foreign exchange] risk, instant settlement outside of banking hours. So, the velocity of money just goes a lot quicker. There are also opportunities in certain jurisdictions to address trapped cash [funds held in foreign nations for tax purposes]. Being able to settle as quickly as we can and being able to move outside of banking hours immediately unlocks a lot of value. Receiving funds quicker from our clients, that’s always something that is going to open up more optionality for our firm. The other thing is the value add that it gives to our clients. There’s the ability to earn additional interest, the ability to park an interest for longer than you would if you were working inside of banking hours. To whatever ends that our partners are realizing benefits, being able to engage with them opens up another avenue for them to achieve efficiencies and to support and grow a healthy ecosystem.

Q

Looking forward, how do you see Aon working with digital assets?

A

Aon’s the largest broker for the digital asset industry, and we have the most comprehensive suite of solutions for the many unique risks and challenges that are faced by the industry. It’s been a long road, lots of education and stair steps of expansion, to be able to bring [insurance] markets to a commercially viable intersect with the [digital asset] industry, where we’re meeting their needs at reasonable rates and terms of coverage.

It doesn’t just stop with the policies that are off the shelf. There’s lots of policies that are needed specifically for the industry. We talked about certain custody programs, we talked about staking insurance policies, we also provide policies around smart contracts and DeFi vaults to protect against losses for oracle failures or smart contract manipulations, and the various risks that people are facing on-chain. We’re continuing to expand that product suite and opening up other avenues to support captive solutions where our clients are using digital assets as a funding source for various risks, depending on what the strategy in their captive is. Obviously, client service is our No. 1 priority, but all of these different financial tools and technologies that are starting to become more mainstream, that are more regulated, that are being used by larger trading partners, are things that we are interested in riding alongside, building and developing solutions to help manage risk and also solutions that can help drive efficiencies in our own business.

So, at scale, I think that you will see a lot more. These things are going to become a lot more commonplace in the insurance industry, for example, as funding sources for insurance-linked securities and reinsurance, when people become more comfortable with this.

The challenging part for insurers specifically is that they don’t get a lot of the upside that the [digital asset] industry gets, in that there’s a lot of headline risk and uncertainty around the crypto industry. That makes it a little bit riskier for underwriters to provide capital for certain types of risk. We’ve come a long way in overcoming some of that and a lot more of this is becoming commonplace. The institutionalization helps tremendously. When you see names like [asset managers] Franklin Templeton and BlackRock and Fidelity that are using this technology, it gives a lot more sense of comfort to the people who are looking at engaging with the technology, not only from an underwriting standpoint, but also from a business standpoint.

When you extrapolate away some of the technical aspects, it just becomes one more avenue of doing business, and that’s what you need to ultimately grow in scale: where people don’t get scared that this is a crypto-related offering, but rather this is just a way that we can save 50 basis points from a strategy that we’re already deploying. That’s when we’re going to see a lot of this stuff take off.

From the high-level point of view, we’re leaning in heavily to this industry because we see a very big impact in an addressable market where there is risk that’s getting brought into the system through a new technology, and there are solutions and strategies to address it. It’s not all with insurance. A lot of it is with other risk controls, regulatory controls, counterparty due diligence. But as more institutions start to come into this space, there is a changing risk profile from the way that things have conventionally been thought of, or structured from an insurance standpoint or from the internal enterprise risk management standpoint. It’s just important to understand what incremental changes you’re making to your business and work with the right advisors who are able to help and guide you to level things up as the risk comes along.

Tech vs. Nature

As tech companies rush to build data centers to meet soaring demand for artificial intelligence, they may face an underappreciated risk from natural catastrophes, especially convective storms. Swiss Re estimates that more than a quarter of U.S. data center capacity may be in areas prone to more than three large hail days per year, and 40% in significant to very high tornado-day zones. That risk is compounded when groupings of data centers are built in relatively small areas, such as Northern Virginia and Abilene, Texas. A regional catastrophe can impact multiple sites within a 20-mile radius. Tornadoes and associated flying debris can hit separate structures in the same campus.

Servicing Space

The global space economy is expected to triple to $1.8 trillion by 2035, McKinsey projects, but orbital debris and inactive satellites accumulate alongside the growth. Starfish Space is attracting serious investor interest for its satellite servicing and de-orbiting technology. The Tukwila, Wash.-based company raised $100 million in a Series B funding round this spring, bringing the total raised to date to more than $150 million. The company’s Otter space servicing vehicle performs life extension missions for geostationary satellites and disposal missions for low Earth orbit satellites. Starfish has conducted three demonstration missions in orbit and has future missions under contract with the U.S. Space Force, NASA, and other organizations.