Closing the Insurance Gap

Q&A with Jonathan Gonzalez, CEO and Founder, Raincoat

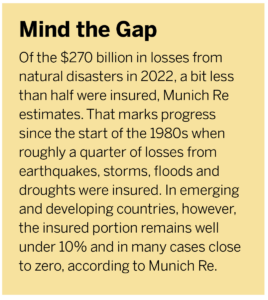

Insurance covers only a fraction of the damages caused by natural disasters in developing countries. Puerto Rico-based parametric startup Raincoat, a winner of Verizon’s Climate Resilience Prize, is enlisting insurers, financial institutions, nonprofits and governments to close that gap.

Q

The cost of natural catastrophes continues to climb, yet many areas lack the financial protection that insurance offers wealthier countries. Why does this coverage gap persist?

A

Sometimes coverage gaps have to do with there not being capacity, there not being risk takers. This is the case, for example, for what’s happening in the U.S., where you have specific insurance companies leaving the market, you have reinsurance capacity drying up in certain sectors.

A much larger gap, significantly larger than that, is just simply the amount of things that are completely unprotected from any type of natural disaster. The unfortunate reality is that most people fall into that. Most losses after a disaster are uninsured across the board, not necessarily because there wasn’t an insurance company willing to take that risk but there might not have even been a product that could even be offered to protect that person.

When people think about natural disaster or climate insurance, the very first thought that comes to your mind is property insurance. In the case of Puerto Rico, more than half of the population doesn’t own property; they rent. There’s no product for that. If you rent and you get impacted by a hurricane and you can’t go to work and the business that you rely on is completely shut down for many, many months, which is the case after Hurricane Maria, there is no insurance product that will protect you against that. That is really where the gap is. It’s going to vary by market. There are certain markets like Latin America, where insurance penetration is sub 1%, so we’re talking about 99% of the population has no insurance.

Q

Hurricane Otis caused enormous damage to Mexico as did Hurricane Maria to Puerto Rico. Do you see a growing vulnerability to such storms, particularly in poorer areas?

A

Absolutely. We see that growth in two ways. We see it in the way where, unfortunately, you have population migration to regions that are highly exposed to climate. For example, if you look at Florida, there has been a lot of immigration into Florida, and Florida is highly exposed. That naturally will increase the overall vulnerability. Just in general, there is a trend when it comes to coastal cities and locations that are exposed to climate of having more wealth and more people, and when there is more wealth and more people, there are also more losses and more vulnerability.

That’s one big factor, and the second one is that these things tend to compound, unfortunately, where those with the least resources are disproportionally affected—much more than those with resources. Not only does that have an implication on actual losses but also on recovery. Because, sure, if you’re a wealthy individual, waiting a year for a claims adjuster to process a claim, you can do that. You have the financial liquidity to do so. But if you’re a very poor person that really needs the insurance payment to be able to recover and you have to wait a year to get a response on that, that can put an insane amount of pressure on that individual and on that family. That’s one of those unfortunate realities.

Q

A number of startups have launched microinsurance efforts to help with climate disasters from drought to hurricanes. Can this be an effective solution to underinsurance?

A

It’s an important solution. The important thing here is that it is a multivariable problem. Underinsurance and the protection gap have a lot of components; not all of them have to do with product. For those that have to do with a lack of product, then microinsurance is a very effective solution. Naturally, I’m biased toward that, because that’s what we do. But part of addressing the coverage gap is developing new products and categories where there wasn’t a solution before. I think that’s how you truly address the gap. Very often people talk about microinsurance within the context of traditional insurance, like, “Oh, if I have a traditional cover, I can add an additional cover,” but that doesn’t do a lot to address the fundamentals of the gap, which is individuals that have no protection whatsoever—zero. Building better products and embedding those products in channels that reach these people, I think, is a legitimately powerful strategy to address the gap.

Q

What role is parametric insurance playing?

A

Oftentimes, there are two challenges that you find in the insurance space when it comes to addressing the gap. One of those challenges is how to build an insurance model that is sustainable. From a risk-taker’s perspective, it’s how much do I have to deploy, can I quantify this risk, and how well can I quantify it. There are all these aspects that have to do with product. The second challenge is related to the customer experience. There are a lot of situations where velocity matters…where getting money in the first week after a disaster versus getting it two years later is a big difference.

In both cases, parametric can really help. It quantifies risks very well. With very little information, I can determine what the probability of a certain type of event is, and I can guarantee that when that event happens I can execute a payment in as fast a way as possible with as little red tape as possible to get to the end beneficiary quickly. That is a very powerful component that helps you address the gap.

Q

How is Raincoat doing that?

A

Shortly after Hurricane Maria, Raincoat was inspired by my own challenges and my family’s challenges dealing with insurance and the lack of protection in general. One of the things we quickly stumbled upon was the potential of parametric insurance, but the big question mark that we had was if parametric insurance was so well known—and it has been used for at least two decades and the potential was there—then why weren’t we seeing products in the category. As a consumer, I had never seen a product. This wasn’t being embedded anywhere. Governments weren’t using it.

When we started meeting with the insurance sector to try to understand why that was the case, there were three problems that kept coming up in conversation. The first was the difficulty around developing a product that could work at a granular level, a product that would actually function well when you brought it down to individuals.

The second challenge was the complexities of integrating all the data. Once you start integrating different data sets—satellite imagery, dealing with machine learning and AI, and all these aspects that come into that—it starts to become a really challenging software problem that comes with its own infrastructure challenges.

The last component was that, even if you have the product—and let’s say you could nail the data sets—automating the full cycle was a challenge because a lot of the legacy systems used to process claims and used to manage policies assume that there is this very traditional claims process involved. In the parametric context, it’s a little different. In the parametric context, you can execute the whole cycle in minutes. That requires automation. That requires retrofitting systems and a lot of development, and that was also a big challenge.

We saw that there was an opportunity to overcome those barriers and work with these established entities to be able to deploy the product. We focus on all these software challenges, help develop these products, and then help support the partner so we can have a successful deployment and then monitor that deployment once it’s live, making sure that everything is operating as expected.

Q

Where is Raincoat active?

A

Right now, we have live deployments in Puerto Rico, Jamaica, Mexico and Colombia and have a ton of new countries in the pipeline that should be coming up online very soon.

In the parametric context, it’s a little different. In the parametric context, you can execute the whole cycle in minutes. That requires automation. That requires retrofitting systems and a lot of development, and that was also a big challenge.

Q

What perils are you providing insurance against?

A

I divide the world into two types of perils. We either deal with catastrophic perils, which include hurricanes, earthquakes, wildfire and floods, or we’re talking about agricultural perils, which include drought events and rain events and complex perils that might not fall into either category but affect yield, affect crops. We see the universe as those two components. We’re either talking about general catastrophic or we’re talking about general agriculture.

Q

What’s ahead for Raincoat?

A

For us it’s growing the category. We’re in a very new category even though parametric insurance has been around for a couple of decades. The reality is that the type of products that we develop and the types of integration and deployment, where you see those products, are very new. There is a lot of iteration at the product level and iteration at the channel level—what is the right way to embed these products into specific channels, whether those are insurance companies or banks or governments or communities. For us it’s really about elevating the category to the next level.

Smart Money

Insurers and reinsurers have been playing a growing role in insurtech investment as technology venture capitalists reconsider. Rather than chasing the next unicorn, however, the industry money is seeking deals that boost performance.

For instance, Travelers is acquiring Boston-based Corvus Insurance, founded in 2017, for about $435 million. Travelers was attracted by the cyber insurance managing general underwriter’s $200 million-plus book of business with reasonable loss ratios and its AI-driven cyber risk platform. Travelers, which has existing cyber capacity arrangements with Corvus, said it will use its technology to improve the loss profile of its existing cyber portfolio.

Allstate and Allianz have made a $265 million strategic investment in Next Insurance, which says the money will accelerate its path to profitability. With Allstate, Next gains access to a broad distribution network and will co-develop commercial auto products for small businesses. The deal with Allianz provides a multiyear reinsurance commitment for California-based Next. Founded in 2016, Next has more than a half million small business customers covered by its general liability, commercial property, workers compensation or other policies.

Berlin-based Wefox raised $55 million in funding from Deutsche Bank and UniCredit in a convertible debt financing deal. The new funding deal follows the $110 million it raised earlier in 2023 in two deals. Wefox was founded in 2015 and is now valued at $4.5 billion.

Overall, global insurtech funding rose nearly 20% to $1.1 billion in the third quarter from the prior quarter, driven by a 25% surge in P&C investment, according to the Gallagher Re Global InsurTech Report. This marked the first quarter-on-quarter increase in funding and deals together since the fourth quarter of 2021, but average deal size fell to a six-year low. Still, the quarter saw two mega-rounds as homeowners platform Openly and cyber risk company Resilience both raised $100 million in Series D rounds.

Broker Focus

BrokerTech Ventures’ accelerator program has seen a strong success rate for participating startups. BTV says 46 of the 48 participating startups so far are still operating or have been acquired. The collective valuation of the first four cohorts of participants to date is approaching $1 billion, and the startups have raised more than $250 million since joining the program. On average, participating startups have seen their valuations double since their enrollments.

“These outstanding outcomes validate the effectiveness of our accelerator program and underscore the vital role that insurtech startups play in driving innovation within the insurance industry, while also working to identify risks sooner and drive down costs faster for our clients,” Dan Keough, Holmes Murphy CEO and BTV co-CEO, stated in the press release.