It’s one thing to read about raging wildfires in California and quite another to experience the possibility of such a catastrophe.

In early August, our secondary home in Idyllwild, a small town nestled in the San Jacinto mountains, was imperiled by the Cranston fire, just one of the many wildfires burning throughout the state. The blaze was started by an arsonist, and all 3,000 residents of Idyllwild were evacuated.

For five nail-biting days, we waited, fearing mostly for our neighbors’ primary homes and their pets left stranded when the roads to the town were closed. A friend in the California Highway Patrol snapped a picture of a giant plume of smoke from our front fence line. It was a half-mile away. Winds blew westerly, not a good sign.

And then our prayers were answered. The ground and aerial firefighters who arrived by the hundreds to battle the blaze finally got it under control. Although the fire consumed more than 13,000 acres, the town and all but a half-dozen homes were spared. Other municipalities throughout California have not been so fortunate. The largest wildfire in state history burned for more than a month and encompassed more than 400,000 acres.

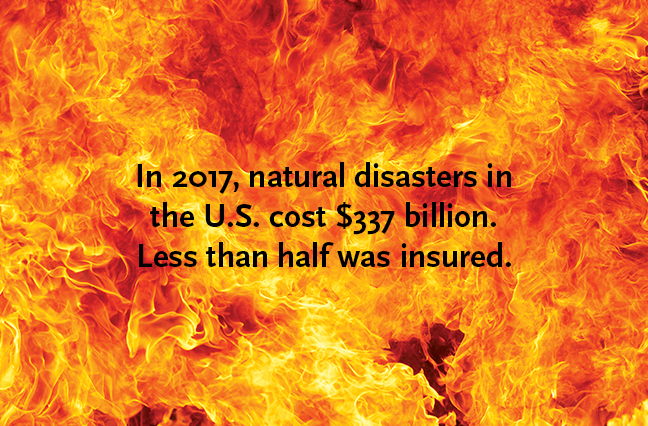

The costs of such natural disasters are borne by all of us—in our taxes and our insurance premiums. That cost was made clear in 2017. A study by the Swiss Re Institute found the economic damage caused by natural disasters last year totaled $337 billion, the second highest on record—of which $144 billion was insured, the highest on record. Three hurricanes that year—Harvey, Irma and Maria—ranked among the five worst hurricanes in history, in terms of financial costs. Insured losses from all wildfires in the world totaled $14 billion in 2017, the highest ever in a single year. In the United States alone, more than 9.8 million acres burned in 2017, costing $18 billion—triple the annual wildfire season record. Among these wildfires was the Thomas fire, California’s worst fire in history at the time in terms of acreage burned.

For businesses, natural disasters represent a serious risk management issue. Many surveys of large and midsize companies rank natural catastrophes among their top three risks. For small companies, such disasters are an even greater threat.

In the years ahead, diverse structures in regions vulnerable to natural disasters are bound to experience substantial property damage and destruction. Large companies will endure significant supply-chain disruptions, delays in business operations and reduced revenues. Many smaller businesses will fail.

What is being done to prepare for this dystopian possibility? The paradoxical answer is: quite a bit but not enough.

For example, in ZIP codes designated by the Federal Emergency Management Agency as susceptible to natural catastrophes, 40% of small companies experienced natural-disaster related losses that curtailed business operations.

Only 17% of them had business interruption insurance, according to a 2017 study by the Federal Reserve.

Leaving aside potential causes, more than 97% of climate scientists in peer-reviewed studies in notable scientific journals concur that the planet is warming. And more than 80% of climate scientists in studies conducted by groups supported by the oil and gas industry affirm that climate change is happening.

“The evidence is unequivocal that the planet is warming, with literally thousands of studies using all sorts of evidence to draw what are pretty rock-solid conclusions,” says Richard Black, director of the Energy and Climate Intelligence Unit, a U.K.-based nonprofit that publishes on energy and climate change issues.

What does this mean for natural disasters? It depends. Among the scientific community, some potential effects are generally agreed upon, while others have less consensus.

Hurricane Flooding

As the planet warms, ocean levels rise for two reasons: thermal expansion (water expands as it warms) and the flowing of melting land-based ice like glaciers into seas. “We can measure sea levels year by year and have seen gradual increases that may accelerate in the future,” said Robert Muir-Wood, chief research officer at catastrophe risk modeling firm RMS.

When hurricanes form, they create an additional abnormal rise in sea level—called a storm surge. The greater the rise in sea levels, the higher the risk of extreme flooding along coastal areas, given the expanded volume of water.

“There’s no doubt that hurricanes will inflict heavier damage due to rising sea levels caused by climate change,” says Michael Oppenheimer, a climate scientist and professor of geosciences at Princeton University. “That’s a no-brainer. The flooding will be greater and will extend more inland from coastlines.” That said, 90% of Harvey’s insured property losses derived from inland flooding and not hurricane wind intensity.

Climate change also is a factor in higher precipitation events, such as the 60 inches of rain that engulfed the greater Houston area during Hurricane Harvey. “As temperatures rise to warm oceans, water evaporates [faster] and produces more moisture content,” Oppenheimer explains. “On that, we climate scientists can agree.”

Muir-Wood shares this opinion. “There’s pretty good evidence to suggest we will have more intense rainfall resulting in extreme flooding events like we saw with Harvey,” he says.

Another factor in hurricane flooding is duration of the storm. Hurricane Harvey lasted 16 days—from August 17 through September 2. According to the journal Nature, climate change affects what scientists call “translation speed”—the speed at which a hurricane travels forward. This speed is slowing, indicating that storms may linger longer in a particular geographic area, increasing the risk of flooding.

“There’s a theory that shows a warming planet stalls atmospheric circulation patterns like trade winds and the jet stream, stalling storms in one place for longer periods,” Oppenheimer says. “But there is no scientific consensus yet that this is explicitly caused by climate change.”

The changing climate might also explain why scientists expect more Category 4 (130 mph to 156 mph winds) and Category 5 (157 mph or higher) hurricanes. That’s because hotter oceans provide more energy, fueling wind intensity.

“We may even need to create a new Category 6 to take into account more intense winds,” Oppenheimer says. “But most scientists are not willing yet to say that the observed change in wind intensity is due explicitly to climate change. Again, we’re not at a point yet to nail this down.”

If there is a silver lining in these dark clouds it is this: more frequent hurricanes generally are not anticipated, with some climate experts predicting a potential decrease in the overall number of future hurricanes, based on models involving warming temperatures. According to the National Oceanic and Atmospheric Administration’s Geophysical Fluid Dynamics Laboratory, three or four small hurricanes might merge into a single large hurricane, although the organization acknowledges uncertainty on this subject.

Droughts and Wildfires

Last year was the second-worst year on record for wildfires in the past 60 years, with 10 million acres burned, exceeded only by 2015, when about 10.1 million acres went up in flames. This year is well on track to break the record. (See sidebar: A Terrible Tally.)

Prior to the 1970s, wildfires in the United States received little attention from the government and the public, as they were generally smaller and sporadic and occurred in mountain regions with scant habitation. Then all hell broke loose. According to the Union of Concerned Scientists, between 1986 and 2003, wildfires burned more than six times the land area, occurred nearly four times as often and lasted almost five times as long as wildfires reported between 1970 and 1986.

More recent statistics indicate that wildfire seasons were 84 days longer on average from 2003 to 2012 than they were from 1973 to 1982. Large wildfires also are taking more time to contain, burning an average of more than 50 days between 2003 and 2012, compared to six days between 1973 and 1982.

Is climate change the cause of all this misery? “It’s a complicated peril, with a lot of actors in play,” Muir-Wood says. “You must take into account the previous history of drought and extreme heat waves.”

He’s referring to the fact that our world has seen weather like this before. Ancient Egypt was lost to one of history’s most withering droughts, and the United States’ most protracted drought occurred during the Dust Bowl years from the 1930s to the 1950s.

However, we do know that the increase in air temperatures due to climate change does cause drier conditions, such as decreased soil moisture and increased evaporation of water from lakes, rivers and other bodies of water—all of which can exacerbate drought conditions.

“Another factor is natural weather occurrences like El Niño events that cause year-by-year variability in drought potential,” Oppenheimer says. “What we do know is that future conditions will be progressively more favorable to these kinds of fires in many areas. The reasons are complicated, but the science is getting close to nailing it down.”

The Human Factor

While climate change can be blamed in part for the recent scourge of natural disasters, human folly contributes to much of the economic impact. First, too many people (myself included) continue to live in coastal areas and mountain towns, regardless of the known dangers. Second, those of us living in these regions downplay the risks and do little to reduce their impact.

“Despite all we have learned about the impact of hurricanes, wildfires and other natural disasters and how to protect ourselves and our businesses from their impact, we’ve actually done very little to reduce the material losses from these events,” says Howard Kunreuther, a professor of decision sciences and public policy and co-director of the Center for Risk Management and Decision Processes at the University of Pennsylvania’s Wharton School.

In his book (written with Robert Meyer) The Ostrich Paradox, Kunreuther contrasts human behavior negatively with the behavior of an ostrich presumed to bury its head in the sand when danger approaches. “The reality is that ostriches stick only their beaks in the sand, but their eyes see everything around them,” Kunreuther says. “People have their entire heads in the sand. The uncertainty associated with future sea level rise and the nature of hurricanes often leads us to hope for the best rather than fear the worst.”

He attributes this reaction to myopia, amnesia, optimism and inertia, which combine to make us always expect the best, even when bad things are blatantly obvious. “People have a tendency to think when they move to coastal areas in a hurricane-prone region that the worst won’t happen to them, despite all evidence to the contrary,” Kunreuther says.

Muir-Wood expressed a similar sentiment. “In most cases, the risks of a hurricane or wildfire are greater than how people perceive them,” he says.

Given all we know, scientifically and economically, about natural catastrophes, the related costs continue to rise, in large part because of our collective tendency to downplay their significance. “Following a wildfire or a hurricane that interferes with people’s lives, little if anything is done to prepare for the possibility of it occurring again,” Kunreuther says. “The thinking is that we will be spared next time around. We have very short memories when bad stuff happens.”

By doing little if anything to reduce the potential impact of a natural disaster, when the next one arrives the aggregate damage losses are higher than they otherwise could have been. A study by insurer FM Global affirms this connection. The multinational property insurer/property loss prevention specialist company evaluated its losses from Hurricanes Irma and Maria, comparing the data of clients that had taken loss prevention actions based on its recommendations with those that hadn’t taken these actions.

“We were surprised to learn that the companies that took these actions experienced losses five times lower than those that didn’t,” says Katherine Klosowski, FM Global’s vice president of special projects. “We had expected a difference but not that magnitude.”

This is good news, indicating that losses can be contained. Such losses run a gamut wider than just property damage to homes and buildings. “There are arrows that go from climate change to things like food security, geopolitical stability and economic growth, all of which create risk management implications for companies,” Kunreuther says.

In fact, according to one study, as much as 95% of fresh produce is perceived to be at risk because of climate change. Livestock health is also at risk, as warming temperatures cause heat stress and increased demands for water that may not be as readily accessible.

“More needs to be done to assess these risk interdependencies,” Kunreuther says. “And insurers are in a prime position to undertake these assessments.”

Fortunately, there are many smart ideas circulating on how homeowners and businesses can reduce their risks of property damage, including water runoff systems like dikes to contain flooding, spraying homes with fire retardant prior to a wildfire and hurricane-resistant doors and windows. For more information, check out FEMA’s online hurricane preparedness and wildlife planning toolkits.

Government Action

When people fail to take actions to limit their exposure to property damage, governments generally don’t intervene on their behalf. “We’ve seen a perpetuation of poor public policy decisions, in which people and businesses are allowed to locate anywhere they want in structures that are inappropriate given the climate risks,” says Will Dove, CEO and chairman of new reinsurer Extraordinary Re. “This guarantees that catastrophe claims frequency and severity will only get worse.”

“We need the political will of the federal government to say that it will no longer encourage risky zoning and land-use rulemaking on the part of local governments, since it is local government that authorizes permits for construction activities in climate-vulnerable areas. Local building codes must reflect the actual risks, which are well understood.”

Princeton’s Oppenheimer also took local municipalities to task for not upgrading their building codes. “They need to get them up to modern standards that reflect reality and then enforce them stringently,” he says. “And the federal government flood insurance program must follow through with rates that are sound but also sensitive to the investments that people make to protect their property.”

If this were the case, more homeowners might buy flood insurance. Only two in 10 homeowners had either private or federally provided flood insurance to absorb losses from Hurricane Harvey, according to an estimate by the Consumer Federation of America. “People without insurance expect the government to bail them out, which is often the case,” Dove says. “In effect, the government bailout takes away the financial responsibility from the individuals affected. When this occurs, the taxpayer ends up footing part of the bill.”

Part of the problem is the National Flood Insurance Program, which is deeply in debt and nearly insolvent, in part due to repetitive claims for property damage by the same homeowners. “NFIP is in need of reforms,” Dove says.

“FEMA flood maps are outdated and don’t reflect current reality. There are no incentives to rebuild structures to accommodate the actual risks, resulting in repetitive loss properties. Coverage limits are stripped down in many cases, with no business interruption insurance for small businesses out of commission for longer than a month.”

Congress is now studying common-sense reforms to NFIP, like improved flood mapping and the identification of properties filing repetitive damage claims. But even with such enhancements, unless flood insurance is mandatory in vulnerable regions, not everyone will buy the insurance. Kunreuther proposed the idea of offering all homeowners and businesses financial incentives, like lower premiums and affordable loans, for structural improvements they undertake to reduce storm-related damage risks.

“A reason why people don’t invest in mitigation measures is because they perceive the cost as too high relative to the benefit,” he explains. “But if the government offers them long-term loans at affordable rates, there’s a better chance they’ll see value in making needed improvements. And if their insurance carrier simultaneously reduces its premiums for taking out the loan, the incentive for the business or the individual is even greater.”

Private Market

It’s not just a government problem, though, and there is a lot the private insurance market and other businesses can do to help encourage mitigation. And the private insurance market is growing for flood. Several reinsurers like Swiss Re are partnering with primary carriers to offer the coverage. Altogether, carriers wrote more than $623 million in business in 2017, a 51.2% increase in premiums over the previous year. Nevertheless, this is a pittance compared to the NFIP’s $3.5 billion in 2017 premiums.

As far as encouraging mitigation goes, Oppenheimer has some ideas. “Frankly, the U.S. insurance industry could do a lot more to fulfill its social responsibility by making sure people properly manage the risks to their properties,” he says. “A rate structure that gives people credit for building and maintaining resilient homes and premium rebates when someone does something good to make the property more resistant to damage are big steps in the right direction.”

Lenders also can do their part. “Banks can require businesses and homeowners in vulnerable areas to buy flood insurance as a condition of loans and mortgages,” Dove, of Extraordinary Re, says. “Many lenders already do this if the region is in a one-in-100-year flood zone. But the flood maps that define many areas are very dated and have not been updated to reflect current climate conditions. Certainly, no one expected that Hurricane Harvey could produce 60 inches of rain in a matter of days. Some regions that were not perceived as a one-in-100-year flood zones in the past may very well fall into this category now.”

Insurance brokers also can help tip the scales. “Too many policyholders are confused about what is and isn’t covered when a natural disaster strikes and are surprised when something they thought was covered wasn’t,” says atmospheric scientist Marla Schwartz, from reinsurer Swiss Re.

An example is mudslide damage and destruction. A few months after the Thomas fire was finally contained, heavy rainfall in the affected region resulted in massive and deadly mudslides that destroyed multiple homes. Although property insurance policyholders did not have mudslide insurance, which is unavailable in California, the state’s insurance commissioner instructed insurers to honor claims for mudslide damage, commenting that the fire was the “proximate cause.”

The decision was contentious, but Schwartz says, “It’s a good sign that regulators are up to date on links between fires and mudslides. But it would be better for insurers to recognize this link in their policies and reflect the risks accordingly in their premiums.”

Taking the Lead

Some believe the global property and casualty insurance industry can play a more influential role in understanding, managing and insuring future natural disasters. “There is no single set of people other than the actuaries at insurers and reinsurers who are better at understanding these risks and calculating their frequency and severity,” Black, of the Energy and Climate Intelligence Unit, says. “Companies like Swiss Re and Munich Re are just brilliant at this for obvious reasons—they’re bearing a good part of the cost. They and others should have louder voices in informing the public and policymakers of what is really going on and what needs to be done as a result.”

An unambiguous “voice” may well be needed. Every time the United States suffers a shocking disaster like Hurricane Katrina, Superstorm Sandy or the California wildfires, the inevitable hue and cry that follows eventually subsides—until the next big disaster arrives.

“The challenge in the future will not be lack of risk-bearing capital to absorb catastrophic losses,” Muir-Wood says, “but whether insurers are allowed to charge for the underlying cost of risk based on their technical arguments.” If they can’t charge for the actual cost of risk, he says, insurers might need to pull back coverage or pull out of markets entirely.

“Certainly, the world is not helped by a U.S. administration that doesn’t accept climate change as a reality, making the chances of support for infrastructure and building adaptions at the federal level currently nonexistent,” Black says.

“But insurers and reinsurers accept reality. They can be expected to tell it like it is.”

Oppenheimer contends time is of the essence. “Human beings have done a pretty good job saving more lives from natural disasters,” he says. “Fewer people die worldwide from hurricanes and wildfires than in the past. But on the property and business interruption side of things, the record stinks.”

Banham is a Pulitzer Prize-nominated financial journalist and author. [email protected].

The Cost

Aided by technology, new players and the capital markets can step in.

Natural disasters across the United States caused $337 billion in estimated damage in 2017, but less than half that amount, about $144 billion, was insured. The remainder was borne by Uncle Sam. Can insurance companies and reinsurers help fill this gap to reduce the financial burden on taxpayers? The answer seems unclear.

But let’s assume municipalities enact building codes and zoning regulations that reflect realistic climate change threats and regulators approve homeowners insurance rates based on insurers’ actuarially derived premiums. In that scenario, would the industry have the will to risk more capital on something as uncertain as the potential impact of climate change?

“Climate change affects trillions of dollars of property at once, assuming there were multiple simultaneous events producing losses,” says John Seo, co-founder and managing principal of Fermat Capital Management, an investment management company specializing in structuring catastrophe bonds. “The challenge is the ability of the insurance and reinsurance markets to absorb the resulting losses, which would amass into the hundreds of billions of dollars.”

Seo cites the example of a major property catastrophe happening in a coastal metropolis. “The equivalent amount of capital required would be the equivalent of 10 million cars colliding at once, which is extremely unlikely and would be considered uninsurable under current insurance frameworks,” Seo says. “The traditional industry will not risk this amount of capital on a single event.”

Even if it had that kind of money, the industry wouldn’t bet it all on one gargantuan risk. “The total amount of capital for a major property catastrophe that all the insurers and reinsurers in the world can take on in a single location like Miami or Tokyo is $30 billion to $45 billion,” Seo says. “We know this estimate from their public filings. Maybe they can take on a few billion more, but nowhere near $60 billion, much less a couple hundred billion dollars.”

Nevertheless, more risk-bearing capital is available from the capital markets to narrow the gap between economic damage costs and insured losses from the capital markets. “Our expectation is that a significant amount of the payouts made by federal, state and local governments in the aftermath of a natural disaster can be borne by insurance-linked securities,” Seo says.

He’s referring to catastrophe bonds, which have been around for more than three decades but have matured rapidly in the intervening years. In 2017, the cat bond market endured its largest losses to date from Hurricanes Harvey, Irma and Maria. Yet in the first quarter of 2018 the market snapped back to tally a record $4.24 billion in new catastrophe bonds issued across 17 separate transactions.

Generally, investors in cat bonds include pension funds and hedge funds looking to diversify their investment portfolios with a new asset class that does not correlate with the risks of other investments. Sponsors range from insurers and reinsurers to large multinational corporations and governments seeking to spread the risk of loss from natural disasters.

Cat bonds function much like reinsurance contracts structured over several years. When the sponsor’s property damage losses exceed a specified financial indemnity trigger like $3 million, the bond activates to absorb a layer of risk up to a stated limit. Other catastrophe bond losses are pegged to parametric triggers like hurricane wind intensity.

Seo is confident that insurance-linked securities can complement traditional insurance and reinsurance in picking up more of Mother Nature’s tab. “The capital markets have more than $100 trillion in play, giving it the potential to be effectively the largest and most efficient insurer in world history,” he says. “I can also see governments and state agencies acting more like private market insurers, while shifting the financial burden away from taxpayers.” Rather than dig into government treasuries to bail out affected businesses and homeowners, the bond would trigger to make the needed payouts.

Seo is not alone in this prognostication. “There is a role for capital market capacity to step in through the issuance of insurance-linked securities or other kinds of structures like ours,” says Will Dove, CEO and chairman of Extraordinary Re, a new reinsurer about to unveil a trading platform run by Nasdaq, on which investors will trade assets tied to insurance liabilities.

Like cat bonds, the unique platform presents investors with the opportunity to diversify their portfolios outside traditional stocks and fixed-income assets—albeit with a couple twists. Other property and casualty risks besides property catastrophe exposures can be invested in and traded like liquid securities, such as aviation, marine, workers compensation, terrorism and even life and health insurance risks. An investor can sell an interest in one risk and buy an interest in another.

Another novel startup is Jumpstart, launched in June, which has created a parametric-triggered renters insurance policy absorbing earthquake risks in California. “Nine out of 10 people in California don’t buy earthquake insurance, and half of them are renters,” says founder and CEO Kate Stillwell. “We’re offering a one-size-fits-all insurance policy for $20 per month on average to absorb up to $10,000 of losses, completely reinsured.”

Stillwell notes the insurance doesn’t just pick up the cost of damaged or destroyed personal contents like furniture and laptops. Other compensable losses include an inability to get to work because streets are closed. The parametric trigger is based on U.S. Geological Survey reports measuring peak ground velocity, a fancy way of saying ground shaking. If the earth moves 30 centimeters per second and more, the insurance kicks in.

Let’s hope it doesn’t.

A Terrible Tally

How bad has the weather been in recent times? Really bad and really costly. Natural disasters caused $337 billion in damage across the United States in 2017, the second costliest year on record for such activity. According to the National Oceanic and Atmospheric Administration, 16 natural disasters last year caused more than an estimated $1 billion in damage each. A sampling of Mother Nature’s wrath:

- Hurricane Harvey, a Category 4 storm, produced an unprecedented volume of rainfall, estimated at nearly 60 inches. Flooding in the greater Houston area exceeded all other known U.S. flooding events. Harvey also produced the highest storm surge level in the Houston area since 1961. Nearly 200,000 homes and business structures were damaged or destroyed.

- Hurricanes Irma and Maria, both Category 5 storms. Irma’s 185 mph winds lasted for 37 hours, the second longest duration on record. Maria’s 175 mph winds devastated Puerto Rico, which was woefully unprepared for a hurricane of such magnitude. Maria ranks as the second deadliest hurricane in U.S. history, consuming more lives than were lost in Hurricane Katrina in 2005. It was the first Category 5 hurricane to strike Puerto Rico.

- In October 2017, northern California’s wildfires burned at least 245,00 acres as high winds raged across eight counties. The fires incinerated 8,900 buildings, claimed 44 lives and caused $9.4 billion in damage. Two months later, the Thomas fire in southern California burned more than 282,000 acres, causing $2.1 billion in damage.

- This summer in California the Mendocino Complex fire consumed more than 400,000 acres, the Carr fire burned nearly 230,000 acres and the Ferguson fire burned more than 97,000 acres. Total economic damages are still being tallied.