Walking the Tightrope

Insurance brokerage M&A activity early this year modestly trails 2025’s pace. Caution appears to be the theme in an environment sensitive to national and global events.

After 2025 delivered insurance brokers their third-most-active mergers and acquisitions (M&A) year on record, with 854 announced transactions, the question is whether deal activity in 2026 maintains the same bumpy momentum.

The first two months of this year appear to be following the 2025 blueprint—a state of heightened economic uncertainty with sticky inflation, stillelevated interest rates, a slowing labor market, questions on trade policy, global unrest, and political crosscurrents. The early results are volatility in the financial market, the Federal Reserve holding the fed funds rate steady, and M&A activity feeling cautious.

On top of the global market disruption, the insurance industry faces questions on how AI might affect the traditional distribution model. The first ripples have been seen in the stark decline of stock prices of public insurance brokers. Collectively, the U.S. public brokers, as measured by the MarshBerry Broker Composite Index, dropped 8.9% on Feb. 9 after multiple news reports on AI’s recent foray into the insurance distribution chain set off an investor sell-off. The index remained down 5.2% through the end of February. While MarshBerry does not believe AI will disintermediate insurance brokers, it could disrupt the go-to-market strategy for personal auto and home and other standard priceled businesses that don’t offer many consultative, solutions-based services.

Together, these challenges are creating a more disciplined capital environment, tempering transaction volume and forcing buyers—particularly those reliant on leverage—to be more selective. Still-too-high capital costs may not dramatically alter M&A momentum or overall volume, but they could redefine who participates, at what price, and under what structure. Weaker balance-sheet buyers may be sidelined, even as valuations for high-quality brokerages remain elevated due to limited supply and persistent private capital demand.

Most dealmakers would gladly accept a 2026 that unfolds much like 2025 for the economy and M&A activity. But it’s a tightrope, and any missteps could dramatically change the outcome.

M&A Market Update

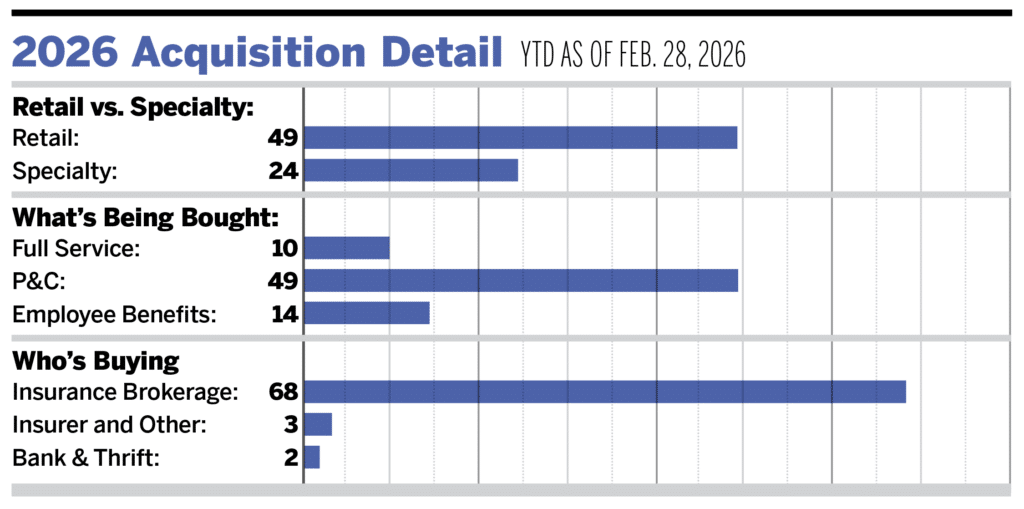

As of Feb. 28, there were 73 announced insurance brokerage M&A transactions in the United States in 2026—down from 85 deals announced last year at this time. Private capital-backed buyers accounted for 47 of the 73 deals (64.4%) through February. Independent agencies were buyers in 13 deals, representing 17.8% of the market. Bank buyers have announced two transactions year to date. Deals involving specialty intermediaries as targets accounted for 24 transactions.

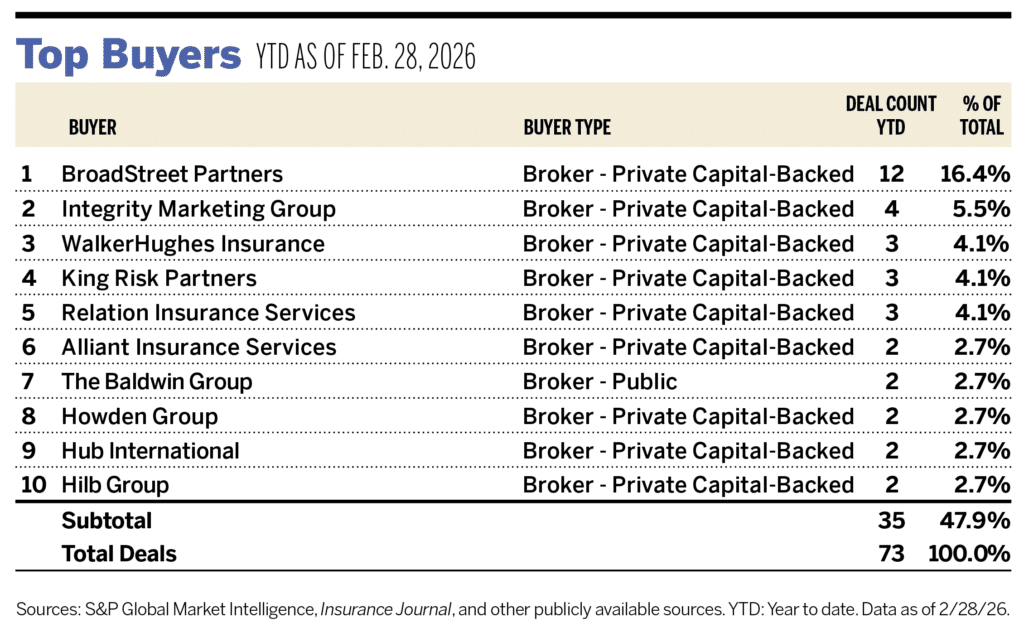

Ten buyers accounted for 47.9% of all announced transactions year to date, while the top three (BroadStreet Partners, Integrity Marketing Group, and WalkerHughes Insurance) accounted for 26.0% of the 73 transactions.

Notable Transactions

- Feb. 10: Revau acquired Triad Oilfield Underwriters, a Houston-based managing general agent and wholesale brokerage specializing in upstream oil and gas and marine risks. The transaction strengthens Revau’s North American footprint by expanding its technical underwriting and placement capabilities in complex energy and marine sectors. MarshBerry served as an advisor to Triad on this transaction.

- Feb. 23: The Vistria Group acquired Lumen Holdings, a Dallas-based, technology-enabled managing general agent, establishing it as a new platform investment within Vistria’s financial services segment. MarshBerry served as an advisor to The Vistria Group on this transaction.