AI Companies Top Insurtech Funding

Q&A with Andrew Johnston, Global Head of InsurTech, Gallagher Re

AI is the hot theme for insurtech investment deals as insurers and reinsurers step up funding in the sector.

In this interview, Johnston discusses what industry investors are looking for in startups and the outlook for larger deals, acquisitions, and IPOs.

Q

Looking back over insurtech investments in 2025, what trends did you find?

A

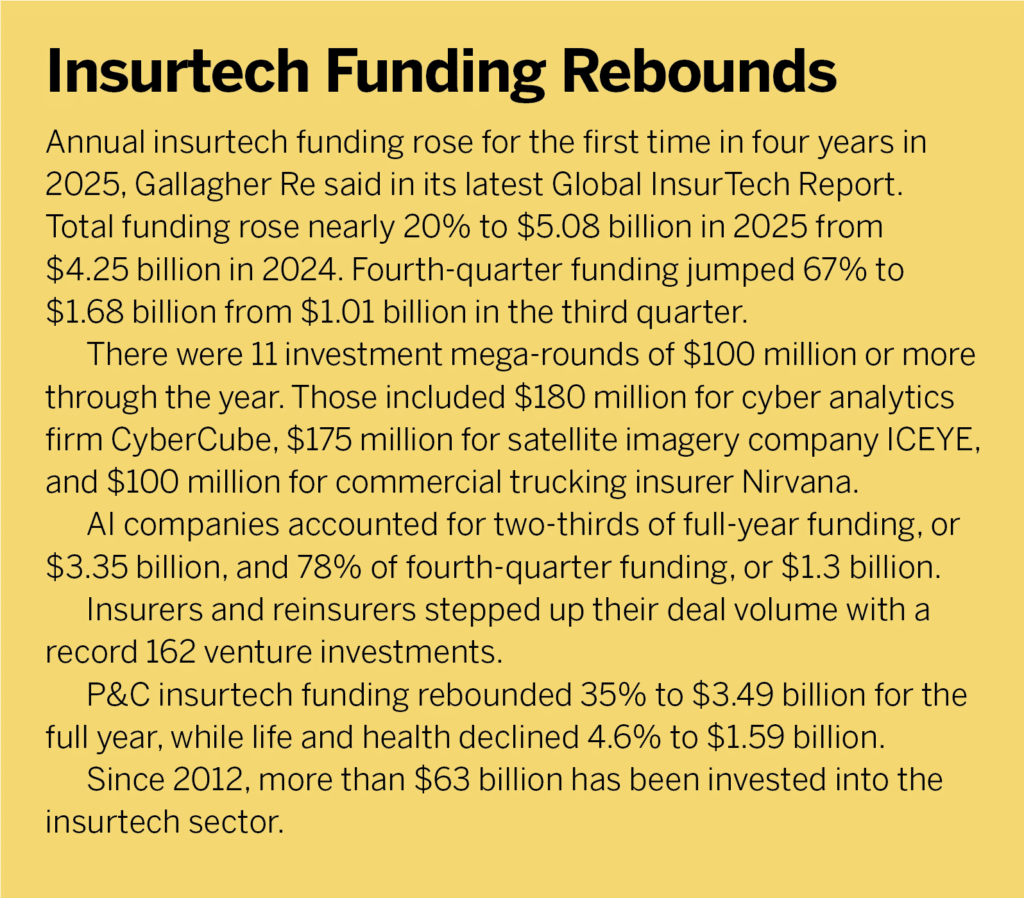

Certainly, the trend for the first three quarters was a continuation of fairly consistent levels of funding around the $1 billion mark [per quarter]—although Q4 was significantly higher. (See sidebar: Insurtech Funding Rebounds) Now, whether that marks the end of a trend, or is just a single quarter that may have a number of deals that added to that overall growth in number, is yet to be seen.

The other two major trends are the levels to which insurers and reinsurers invested during 2025, which was an unprecedented high, which speaks to the confidence that insurers and reinsurers now have in making those sorts of investments, and one step further, even potentially selecting long-term growth partners for them, where businesses or business outcomes are aligned.

Then, there is just the proportion [of] investment dollars going into companies that identify as AI firms. About 80% of last year’s [fourth-quarter] funding went into AI companies, or at least into insurtechs that identify as AI companies. That’s potentially slightly misleading. These are, in many cases, the same business, but they now have adopted the label of AI. They probably did have AI capability but never felt the need to say it, but also, as it’s a very invoked term at the moment, it does help valuations, candidly. On average, a company that says it’s AI is worth about 20% more, so there’s a lot of logic to adopting the label, but I don’t want to give you the impression it’s a brand-new class of companies that are attracting this capital. In some cases, it’s insurtechs that have been raising capital for the last decade that have adopted the label.

Q

What’s behind the rise in insurer and reinsurer investment in insurtechs?

A

Confidence is a big part of it. We’ve been at this [the industry investing in insurtech] now since 2012, and insurers and reinsurers have a much better handle on what’s adding value [and] which companies are likely to be long-term partners where there is a long-term opportunity for both companies. Individual businesses are valued more cheaply, so it’s potentially more of a bargain to invest in some of these companies than it was, say, three or four years ago.

On the insurtech capital-raising side, there is also probably more of a demand now from the individual businesses wanting capital from insurers and reinsurers because of all the expertise that they can bring, because of the business acumen, the business partnership that they can bring, the distribution opportunities that they can bring. There’s both a push and a pull that we’ve just probably never seen to this degree before.

Q

What are industry investors looking for in AI?

A

The insurers and the reinsurers are really looking to solve known problems. These are tackling those kinds of highly predictable, menial, rote, labor-intensive processes, where the idea would be that AI could come in and massively speed up an operation.

To throw a cold bucket of water on things, most of what we’re seeing could be classed under the label of automation. Most AI is automation at this point. We aren’t seeing huge amounts of creativity around human-like outputs, like we are seeing in other industries, not at scale at least. But anything that is highly predictable, very voluminous, where answers can be categorized into a slim number of boxes, is where most of the attention is focused, whether that’s data capture at scale, whether that’s deploying large language models at scale, whether that’s assessing sentiment at scale, whether that’s processing claims files at scale, using various kinds of OCR [optical character recognition] technology, that’s really the sorts of things that we see companies being interested in investing in, which is interesting, but it’s not necessarily cutting-edge stuff.

The industry has learned that there’s not as much competitive advantage to being a first mover as people probably think, and technology, by definition, is designed to scale and be reused. So it might behoove companies to wait a minute and see how experiments play out before they themselves begin to invest. Another part of that learning curve over the last 15 years has been to work as an industry, to kind of share notes, and see what’s working and what’s not.

Q

There was a rebound in megadeals, bigger than $100 million, but they seemed very diverse in terms of the insurtechs involved. Is there any pattern?

A

Probably not. Megadeals are generally a fortuitous coincidence. Of the handful of megadeals that were done last year, they are likely to be companies that are around for a long time. The quality of the underlying company is incredibly high. Similarly, we saw a few companies go public last year, where we have had a dearth of that for the prior three or four years. And again, the companies that have gone public are particularly high quality, certainly compared to some of the businesses that were doing mega-round funding in, say, 2020, some of which no longer exist. I don’t tend to read too much into those individual deals because, despite capturing the funding headlines, they’re not actually very indicative of the broader insurtech scene underneath, which are many hundreds of companies.

But I do think it’s interesting that there is still clearly appetite to write some very big checks. And so, if nothing else, we can see that as a bellwether to the industry’s bullishness on the long-term value of some of these companies deploying tech appropriately in our industry.

Q

Why are investors favoring companies that supply stand-alone technology rather than the tech-enabled brokers and MGAs?

A

A little bit is the sheer capital requirement. If you can stand up a great tech solution that you can license to multiple entities versus create a company that requires all of the investment that any company requires, it makes sense to offer that kind of software-as-a-service vendor model, because it makes the most of the inherent ability for technology to scale. Spending a ton of money on technology that is only then used by one company, it can take a lot of years to realize that investment return. Whereas if you create the same solution and license it to 30 companies, you might realize the return on your initial investment in year one. If you look at the sheer number of costs associated with starting up a business that is looking to essentially win business away from an incumbent broker, or an incumbent insurance company, or an incumbent reinsurance company, in some cases, it is prohibitively expensive, and the value of having a tech platform that, over time, might lower your op-ex, is often not realized in the first couple of years. So, it’s just a less risky hedge. But it also celebrates the inherent value of scalable, transcendental tech. And I don’t think that’s a trend that we can see reversing.

Q

We’ve seen some large insurtech acquisitions over the last year—NEXT, Boxx, Cytora, CAPE Analytics. What are you seeing in insurtech M&A?

A

It’s definitely picking up. Again, part of that speaks to prices coming down and people having a better understanding of where two and two can equal five. CAPE Analytics is a particularly interesting one because they really are supporting the core business of [new owner] Moody’s. We will probably continue to see a healthy stream of M&A. A lot of it will be large insurtechs partnering with other large insurtechs. We’ll still see the occasional insurer or reinsurer buying an insurtech. But these are businesses now that, in some cases, have been around for 10-plus years and are demonstrably successful, and the owners may decide that they want to do something else, or there may be a deal that’s presented to them that just makes a lot of sense.

There are some natural marriages now that are finding each other in the market. But much like the mega-round deals, we are talking about a very small proportion of the overall landscape, and I would estimate it’s probably 3,000 insurtechs on Earth at the moment. But I do think that M&A will be a consistent feature. Are we going to consistently see more than 10 [acquisitions] a year? Maybe, but I don’t think it’s going to be 100 a year.

Q

What’s happening with insurtech IPOs?

A

They’re very high-quality companies—obviously, Neptune [flood insurance], incredibly good business; Ethos [life insurance technology], incredible business. If we compare them to some of the IPOs that happened in 2019, 2020, you could argue that they are businesses that benefited from just having a couple more years under their belts and that the market conditions have changed somewhat. But I don’t see these as fad ideas. They are businesses for which it is the right time to go public and it’s the right thing for their business model.

Q

What do current investing trends mean for the industry?

A

The three main trends are consistency of funding, AI capturing most of the funding headlines, and insurers and reinsurers participating so actively at the moment. These are all very positive signals. These are all clear signals of a very maturing, very sustainable, long-looking investment thesis that stands our industry in really good stead.

You could say that 15 years is a long time to get there, but actually, we’ve done a great job of quickly getting to this space. What we’ll probably end up seeing now is just, year on year, a gradual increase in total investment, whether that’s driven by inflation and [interest rates], or a renewed interest, I don’t know yet.

But the industry is incredibly well positioned for the long term. AI has presented some challenges along with the opportunities, not least understanding its true value. Some insurers and reinsurers are still grappling with where the long-term value of AI is going to be. But if we work as an industry, we’ll undoubtedly get there.

Dealmaking Hot to Start 2026

Insurtech deals got off to a strong start this year, with a big initial public offering, a notable acquisition, and some robust funding.

In January, Ethos Technologies’ IPO raised about $200 million and valued the life insurance technology firm at about $1.2 billion. In February, Ethos reported full-year 2025 revenue growth of 52% to $388 million, with net income of $71.2 million. The company said it expects revenue growth of around 32%, to $510 million to $514 million, for the current year.

In February, U.K.-based insurer Admiral Group announced it would acquire digital commercial fleet platform Flock for £80 million ($108 million). Flock uses AI-driven risk models to improve safety and lower premiums for good risks. Flock, which had partnered with Admiral’s venture arm, Admiral Pioneer, becomes Admiral’s telematics-based fleet insurance platform.

Among first-quarter fundings, Swedish digital pet insurance startup Lassie raised $75 million in a Series C round, Bermuda-based AI insurance technology company mea Platform raised $50 million in equity funding, and AI-driven medical professional liability platform Indigo raised $50 million in a Series B round.

LatAm Shift

Amid a sharp increase in funding, Latin America’s insurtech sector is shifting focus from digital distribution to building enabling technology in partnership with insurers and reinsurers, according to a report from Spain-based global insurer Mapfre and Digital Insurance LatAm.

More than half of current insurtechs in the region are categorized as technology enablers working with insurers and reinsurers, just edging out those focused on digital distribution for the first time.

In 2025, funding for Latin American insurtechs more than doubled to $199 million from $92 million in 2024. The total marked the third-highest level behind $215 million in 2022, which included a $125 million raise by Chilean insurtech Betterfly, and $425 million in 2021.

The number of Latin American startups rose 7% to 536. Chile moved into third place with 100 startups, behind Mexico at 139 and Brazil with 214. Nearly one in five insurtechs operate in more than one country.

About one in 12 insurtechs shut down over the year, a mortality rate of 8%. Over the last four years, nearly half of the region’s insurtechs have disappeared, but 330 new companies have started up.