Experience Mod Sleuths

Finding Major Client Savings in Inaccurate Workers Compensation Ratings

Many nonprofit organizations run on tight budgets.

So when Insurance Office of America (IOA) experience modifier specialist Kelly Lopez and IOA vice president and managing partner Bill Rush identified a six-figure carrier error in a nonprofit client’s workers compensation insurance rate component, it was a big deal. The error incorrectly classified the organization’s employees over a three-year period, resulting in a $250,000 overcharge.

Brokers and agents need the skills to detect errors in order to help clients with workers compensation premiums.

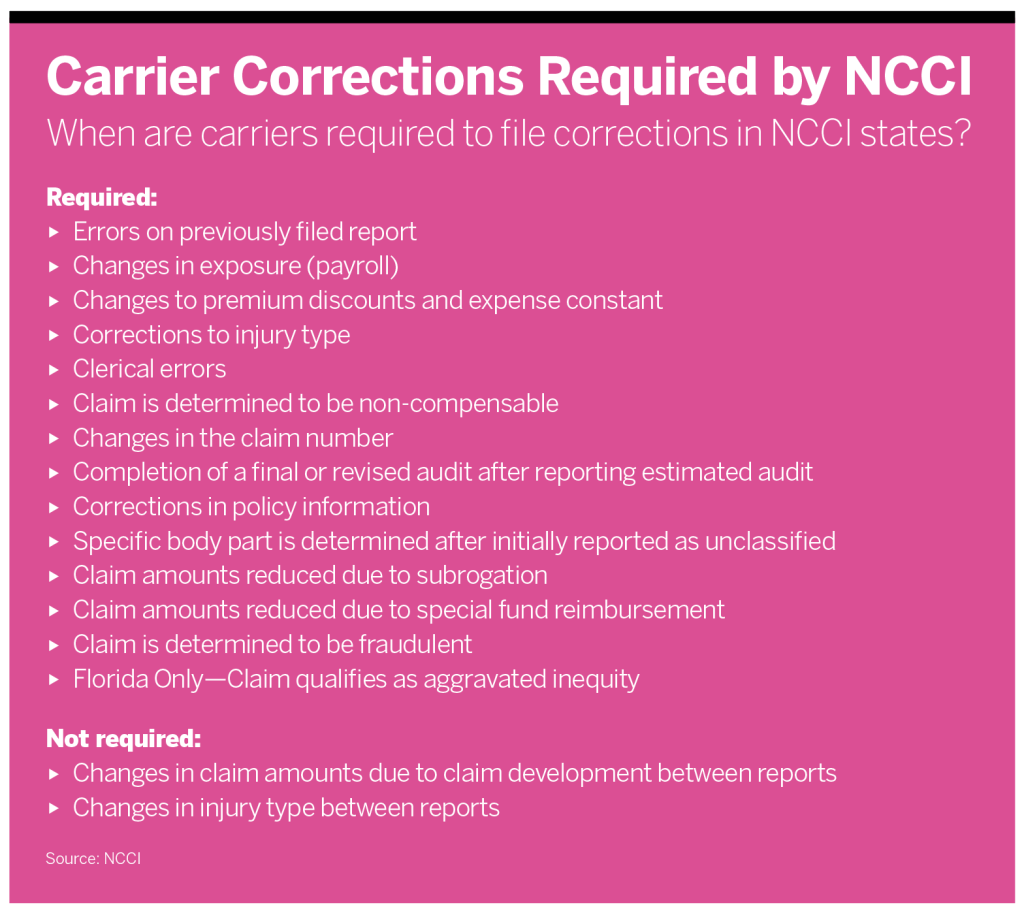

Carriers typically provide corrected data to the rating bureaus and then adjust premiums to remedy any overpayment.

Different rules in different states make the policing of experience mods a challenging process.

State workers compensation ratings bureaus use audited payroll and loss data provided by carriers to derive an experience rating modification factor (experience mod or ex mod), as one element in setting individual employer rates for their workers compensation premiums in cases where employers have a sufficient level of premiums and losses.

Lopez has performed thousands of experience mod rating audits over the last 25 years, and just since 2016 she has saved IOA clients $2.3 million. “We have a new client that had sold a business two years ago,” Rush says, “and the ratings bureau rules say when you divest the business, the experience rating disappears for the divested entity and is transferred to the acquiring entity. Because Kelly knew that and asked the question, we found out they had not removed the experience rating, so we petitioned the carrier to remove that payroll and losses, which reduced the experience rating from a 1.05 to 0.69, as well as subsequent modifications, resulting in over $200,000 in savings for the client.”

Brokers and agents serving employers with workers compensation policies can help their clients by detecting and correcting inaccurate experience ratings that result in premium overcharges—but only if they and their employees have the skills to detect and correct such errors.

Because it is mandatory coverage in almost all states, workers compensation insurance is heavily regulated. That heavy regulation translates into increased transparency regarding the calculation of rates, including derivation of experience mods. Brokers, on behalf of their employer clients, can and should use that transparency to challenge inaccurate ex mods that result in overcharges and persuade carriers to make corrections.

Ideally, brokers and agents also should be able to check for such data inaccuracies by comparing, for example, employer loss and payroll data provided to carriers to the data that carriers provided to the rating bureau, then tracking the data and how it is used by the rating bureau to compute the employer’s experience mod, says Marc Engel, property/casualty risk advisor at USI Insurance Services.

“It’s not an employer’s job to know this,” Engel says. “Their job is to run their company. So we’ll come in and complete a thorough review looking for things like, ‘It says you have $200,000 in payroll over here based upon these employees working out in the fields. But in reality, they’ve been working inside the shop all day and are exposed to a completely different set of risks. So you should not be paying the assessed $30,000 per year for these guys.’”

Generally, upon review and acknowledgment of errors that are caught and reported in a timely manner, carriers provide the corrected data to the rating bureaus and must then recompense or adjust premiums to remedy their overpayment based on that inaccuracy, Rush says. Sometimes errors may be brought directly to the attention of the rating bureau, too, which can inform responsive corrections, Lopez notes.

The Rating Bureau Landscape

What can make policing experience mods a bit challenging is that the rules governing ex mod calculations, data input, and the degree and manner to which they can be corrected vary state by state.

State rating organizations administer workers compensation experience mod calculations. There are 36 states that use the National Council on Compensation Insurance (NCCI) as their rating bureau but allow private carriers to provide insurance. There are four monopolistic states (North Dakota, Ohio, Washington, and Wyoming) that administer their own plans and rates whereby they exclusively provide workers compensation to employers in each state. The rest are independent rating bureau states that have their own state rating bureau, similar to what NCCI does, but allow private carriers.

Of the four states that have aggravated inequity rules—Florida, Massachusetts, Minnesota and Wisconsin—only Florida is an NCCI state. A fifth state, North Carolina, used to allow aggravated inequities challenges but repealed that provision in 2010. Aggravated inequity rules provide procedures for a comprehensive review of experience mod determinations if significant shifts in loss values are met but in a manner that also can limit correction of some errors to those that equal or exceed a certain threshold. The applicability of an aggravated inequities rule can matter a great deal, Rush says, because aggravated inequities challenges are by far the biggest money savers for IOA clients in Florida.

However, in many states, experience modifier challenges can be brought on a number of other grounds based on erroneous data or calculations.

States also have different rules for different types of errors regarding the period during which an experience mod rating error can be reported, how far back detected errors can be corrected, and how ex mod errors are corrected.

The Range Of Ex Mod Errors

Experience ratings recognize the differences among qualifying employers with respect to safety and loss prevention. They do this by comparing the experience of individual employers with the average employer in the same classification. The differences are reflected by an experience modifier based on individual payroll and loss records, which may result in an increase, a decrease or no change in premium. Under NCCI’s plan, the experience mod is derived by dividing adjusted actual losses by the adjusted expected losses. For example: $227,796 ÷ $227,320 = 1.00. This 1.00 is applied to the employer’s manual premium at the policy’s renewal. Experience mods below 1.00 generate premium reductions, while those above 1.00 generate premium surcharges.

Experience mod errors relate to the use of, misuse of or failure to use the right data from the two sets of carrier data that affect experience mods: audited payroll data and loss data. While such errors occur in only a small minority of all experience ratings, there are many types of experience mod errors that require corrections.

First, there are aggravated inequities, which provide for adjustment of rates when significant disparities arise between the rating bureau’s experience mod and the actual cost of claims.

In states with aggravated inequity rules, such an inequity is determined to have occurred when the calculated ex mod (based on reserves for open claims at the normal valuation date) is inaccurate by 5% or more compared to the actual cost of claims that closed between that normal valuation date and the next effective date of coverage. The rating bureau, upon written request from the insurance company or an authorized representative, is permitted to come up with an updated experience rating modifier using a revised unit report submitted by the carrier. The rating bureau then recalculates the ex mod, thereby lowering the experience rating for both the current year and the new policy year by the appropriate amount.

Regardless of whether or not a state has an aggravated inequities rule, the loss revision rules for most states allow challenges to various types of experience mod calculations errors, Lopez notes. Lopez and other sources described some of these types of errors.

- Payroll accounting errors are among the largest categories of experience mod errors that get identified. Sometimes payroll data are disputed or carriers fail to revise or submit revised data after an audit.

- Other errors relate to improper classification. Experience ratings for individual companies reflect, in part, the peer industry group to which they are related. When a carrier errs and rates an employer against companies from another industry, incorrect rates result.

- Sometimes incomplete information results in the use of a preliminary experience mod, but corrected data is not later supplied and the experience modifier is not altered as it should be.

- More pedestrian clerical errors can also creep in. Carrier duplication of claims, incorrect dates for claims, and instances when the originally reported claim is non-compensable as determined by the carrier but not removed from current or prior experience mods are some examples.

- One frequent mistake is inappropriate medical treatment billing for a particular injury. For example, if two conditions are treated and resolved in one procedure, there should be a single bill instead of two separate bills that could raise overall costs.

- Inaccurate subrogation recoveries is another fairly common error. Auditors can check if their client’s carrier is seeking reimbursement from a third party or second injury fund benefits, which should result in a revision to reported losses.

- Another inaccuracy type involves failure to properly account for deductibles. It can also be critically important to ensure that injured employees who are recovered return to the office. “There are two types of claims: medical-only claims and lost-time claims,” Engel says. “Lost time claims are the ones that really hurt you financially, as 100% of those claim dollars go on your mod for the next three years, whereas medical-only claims are reduced by 70%. So employers need a strong return-to-work program. Even if employees are just organizing the office or sweeping the floors, they need to be back at work and not out sitting on the couch on a lost-time claim. Typically, 72 hours is the threshold for getting an employee back to work before a medical-only claim becomes a lost-time claim.”

Lopez says, on average, 5% to 10% of the experience mods she audits have errors of some sort. Generally, she adds, the larger the client, the larger the potential premium reduction and the easier to justify the time to perform the audit.

There are other experience-mod-related issues that brokers may monitor through claims adjusters. Carriers sometimes forget to adjust reserves downward on individual claims, Rush notes. “At our agency,” he says, “we have licensed claims consultants behind us, agents who are calling the carriers and saying, ‘Hey, John Smith, claims just set reserves there for six months, and nothing has happened.’ And the carrier says, ‘Oh, I forgot to reduce that.’”

We have licensed claims consultants behind us,

agents who are calling the carriers and saying,

‘Hey, John Smith, claims just set reserves there for six months, and nothing has happened.’ And the carrier says, ‘Oh, I forgot to reduce that.’

Bill Rush, VP and managing partner, IOA

Helping Clients Improve Ex Mods

While experience mods are not public, some contractual partners may demand them. “It’s a number that qualifies what your level of safety is,” Engel says. “For example, a business partner in transportation or construction may not allow you to bid on a project if your mod is above 1.1 or whatever it may be. So it can really affect your revenue streams and how you are viewed by your customer base.”

That can lead to a quest for ways to lower a client’s mod, Engel says. “So if you come in and say, ‘All right, Marc, we need to be below 1.0 and we’re at 1.02. Is there anything we can do about it?’ Then we go look, and lo and behold we find that there’s a claim on there that was listed as open at $100,000 and it just closed two weeks ago at $30,000. We can get that filed for them and get them down below 1.0 so they can get that contract. That’s huge for a company, right?”

Working with clients and insurers to get claims closed also is a key to lowering experience mods, Engel says. “Sometimes claims tend to drag on, and they don’t get closed in a timely manner,” Engel says. “Our job is to look at that again, work with the client and insurance company, and ask, ‘What’s going on with this claim?’ By expediting the process and showing the claim is closed, employers will be better off come renewal in the eyes of the insurance company and receive potentially better rates.”

Stephanie McMullen, technical resources director for the mid-Atlantic region at USI, says ensuring good data is vital for a number of reasons. “Even if there’s a state requirement that doesn’t allow a correction for a particular item,” she says, identifying errors and improving future data accuracy “allows us to better highlight and show the client exposure and experience trends we are seeing in the claims history. It could also improve your loss history going forward if it helps clients avoid those claims in the future.”

While brokerages will not be placing policies in states with monopolistic funds, it still may be useful to know how experience mod analysis works there. “Washington provides several methods for employers to check the data used in the calculation of their experience factor,” says Herbert Atienza, a spokesperson for the Washington state Department of Labor & Industries. “The Claim and Account Center (CAC) is available online and allows the employer to review all the claims on their account.” The department, Atienza says, “can also provide an exhibit showing the calculation of the experience factor, which also lists all the claims and claim values used. Insureds who find inaccurate information can address those issues with their L&I account manager.”

Rush says IOA offers experience mod auditing services free of charge to clients, and Engel agrees that brokers and agents should be providing experience mod monitoring and correction services to clients as a matter of course.

Engel says USI assists in the process by providing claims analytics for clients and prospects, which can uncover errors and lead to deductible discussions and premium savings.

Training on the subject can be found. “We’ve got some great carriers, primarily workers-comp-only carriers in Florida, that give classes on how to look at an experience mod, how to calculate an experience mod, what the parameters are, and what the components are,” Rush says.

The NCCI website offers many training videos as well as a tool called Risk Workstation that is available for carriers and agents. Risk Workstation requires an account but allows agents to go look at their clients’ mods or access that information. Agents also may get that information from the employer clients directly because, in many states, notifications are sent to the employer when their mod worksheet has been produced. Or they could receive it from carriers because the carrier should be getting that same detailed mod worksheet information.