Specialty Insurance Revolution

Capital and talent are supporting a sea change in the insurance industry’s structure.

In its 30 years analyzing the property and casualty (P&C) industry, ALIRT Research has not witnessed such a furious pace of movement into and amid the specialty insurance sector as has occurred over the past five or so years.

There are several well documented reasons for the current surge of specialty insurance interest from both insurers and distributors, which include:

Insurance is specializing to maximize expertise and opportunity.

Big data used at a granular level supports this evolution.

Market share for excess and specialty continues to grow.

1. A persistent firm/hard rate cycle which has shifted certain risks from the admitted to non-admitted markets where specialty insurers, by definition, shine

2. The exodus of underwriting teams from large insurers to establish their own delegated underwriting units (MGAs, MGUs, program managers) where they enjoy more professional freedom as well as greater earnings potential

3. Continued insurtech innovation, including the use of larger data sets and data mining techniques to better target and underwrite risk as well as operations-focused technology that streamlines processes and connectivity, enabling more nimble operations than traditionally found at legacy insurers

4. The availability of capital eager to back new underwriting capacity as well as distribution teams

5. The willingness of AM Best to issue A- ratings for newly minted (or freshly acquired) insurers based on strength of management and capitalization.

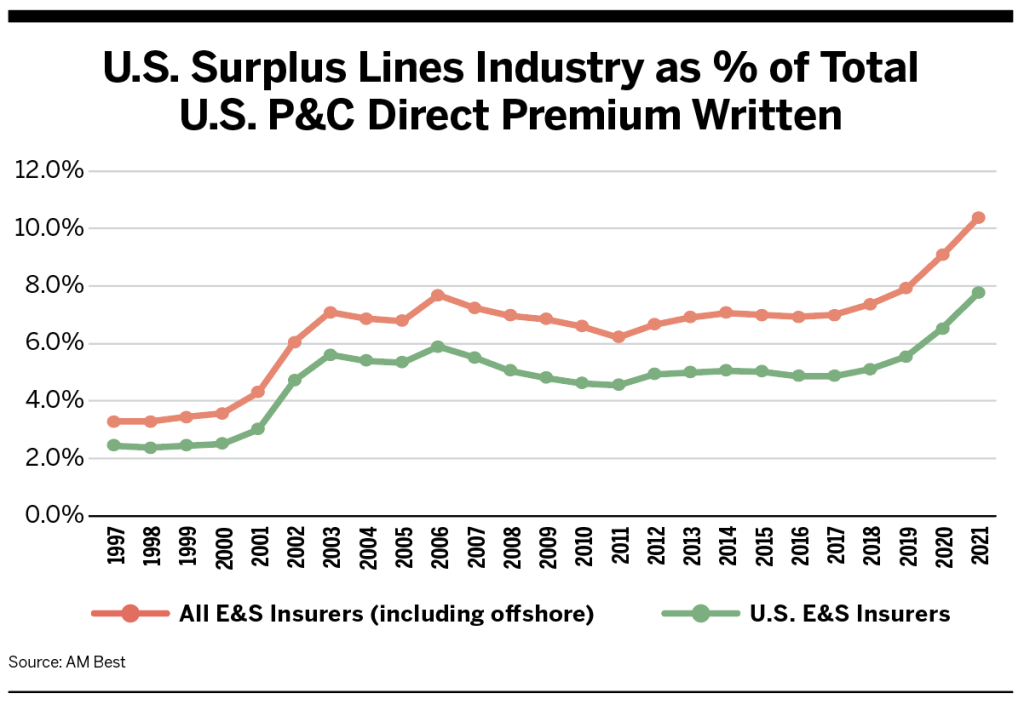

That specialty insurance is gaining a larger share of U.S. market premiums is clear from the growth of excess and surplus (E&S) lines business, as tracked by the annual AM Best/WSIA report. As shown in the surplus lines graph on the following page, this share grew from 7% of total U.S. premiums in 2017 to over 10% three years later (equating to almost 20% of U.S. commercial lines premium). While comparable figures are not yet available for full-year 2022, the 15 U.S. stamping and service offices recently announced a 24.1% increase in their aggregate 2022 E&S premium, which indicates yet another explosive year for this market sector.

The program administrators market, which includes admitted as well as surplus lines specialty business, is also reporting dynamic growth. The Target Markets Program Administrators Association (TMPAA) conducts a market survey every two years, with the latest in 2021 showing program business premium rising 33%, from $40.5 billion in 2018 to $53.8 billion in 2020. Such growth has almost assuredly continued given the burst of program administrator activity over the past two years.

The Specialty Players

ALIRT views the specialty insurance landscape through the lens of various insurer segments. The U.S. Specialty Insurance Ownership Categories chart to the right shows those insurance groups that have organization crossover within U.S. E&S lines, Lloyd’s of London, and large Bermuda (Class 4) markets. These include:

National insurance groups: These large organizations (mostly with domestic parents) write wide swaths of admitted insurance coverages. Each of these well branded insurers also offers differing levels of specialty capabilities, with several making a concerted effort to buy greater specialty capacity over the past five years (e.g., Chubb’s acquisition of Ace Ltd. in 2016, AIG’s acquisition of Validus in 2018, and The Hartford’s acquisition of Navigators in 2019).

Large U.S. specialty groups: These sizeable insurance organizations in the United States focus the greater part of their business on specialty insurance coverages.

Bermudans: Since the liability crisis of the mid-1980s, Bermuda has emerged as a global hub for specialty insurance and reinsurance. Additional “classes” of Bermuda insurers emerged in 1993 following Hurricane Andrew, in 2001 following the terrorist attacks of 9/11 (and soft market years 1997-2001), and in 2005 following Hurricane Katrina, each in response to a loss of market capacity.

Global reinsurers: In addition to their core global reinsurance business, these companies have acquired primary U.S. specialty insurance capabilities.

Others: The U.S. specialty insurance market is so fragmented that it’s difficult to capture all of its various permutations within the above four buckets. This group includes a number of Lloyd’s-based organizations, two U.S. super-regional mutuals, along with several others that have a sizeable specialty footprint (including two owned by Japanese parents).

The intersection of the U.S., Bermudan and Lloyd’s of London markets for these various specialty insurance groups is telling. As can be seen, each of the listed companies has interests in at least two of the three sectors, with most having underwriting capabilities in each. This is due in part to the desire of many of these insurers to access global re/insurance markets but also to the use of offshore vehicles (such as Lloyd’s syndicates) to write U.S. specialty business. In fact, the Lloyd’s of London marketplace remains the largest provider of E&S capacity in the United States, as most syndicates (and large Bermuda-based re/insurers) are included on the National Association of Insurance Commissioners’ “white lists” as approved alien carriers.

While an entire article could be written on the merger and acquisition activity among these three sectors over the past decade, it is instructive to consider only the repositioning of ownership in the Bermudan market from 2016 to 2019, when major Bermudans such as Ace (2016), Allied World Assurance (2017), Endurance (2017), XL (2018) and Aspen (2019) changed hands. In addition, Sirius and Third Point merged in 2021, and Argo Group recently agreed to be acquired by Brookfield Re. A similar spate of acquisitions has occurred within the Lloyd’s market, with a September release by ALIRT listing upwards of 40 syndicate ownership changes over the decade from 2013 to 2022. In short, the jockeying for broader specialty underwriting capabilities within these larger insurance groups continues apace.

But developments do not stop there. ALIRT has also tracked the rise of much smaller specialty insurers and—perhaps more important—the rapid expansion of “fronting” capacity over the past five years. There is substantial crossover between these two groups, which are largely backed by private ownership (including private equity interests), but also between various publicly traded companies that are not among the largest insurance groups.

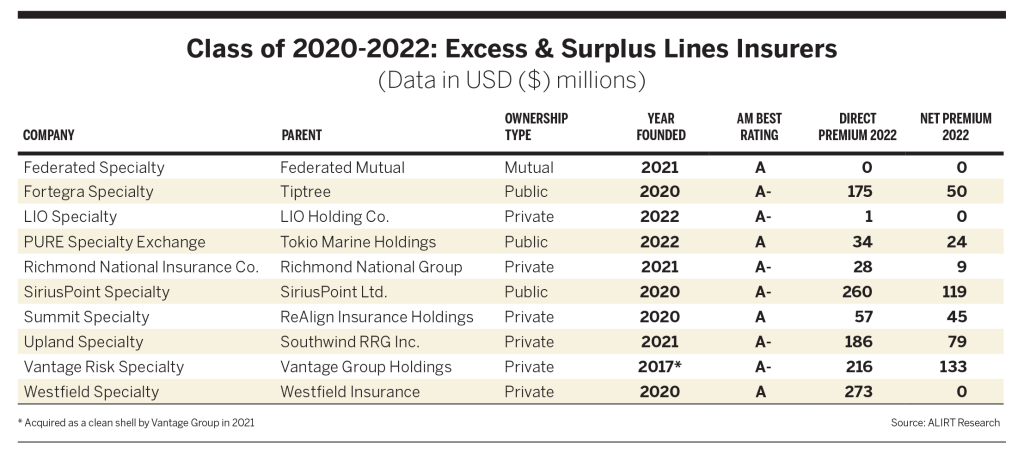

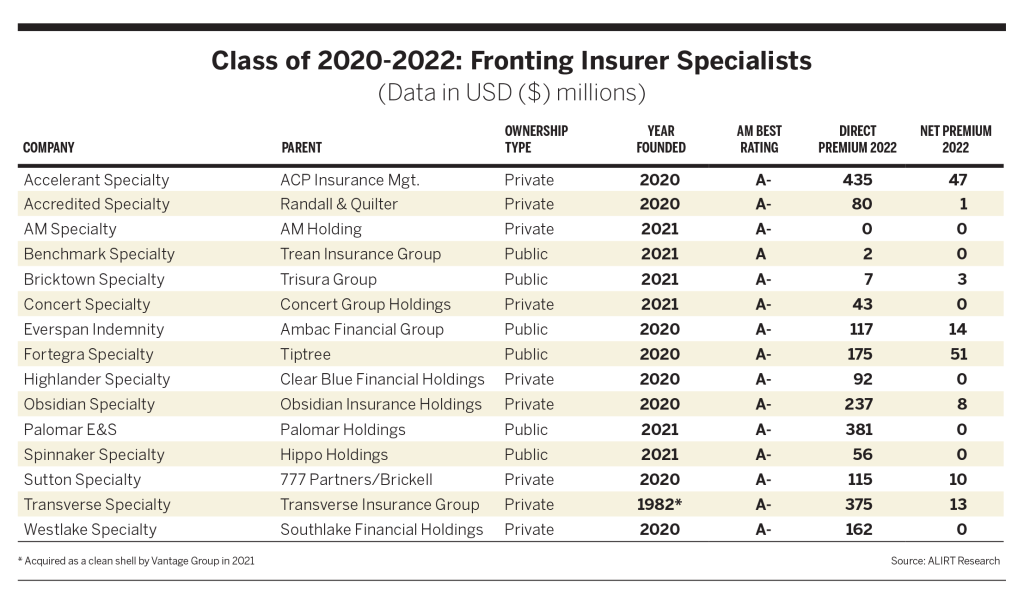

To give a flavor for the rapid emergence of this smaller specialty insurance capacity, we show below just the “Classes of 2020-2022” of these two groups. It should be noted that we are capturing here only the excess and surplus lines insurers for the various fronting and non-fronting groups and that new or recently acquired admitted paper is an additional source of specialty capacity, especially in the program market space. As mentioned, the willingness of AM Best to assign A- (or higher) ratings to these startups is crucial to their business model.

Especially impressive has been the surge in fronting insurer premium. ALIRT maintains a fronting composite which currently consists of 55 insurers that act as either “pure” fronts (reinsure all their business in exchange for a fronting fee) or “hybrid” fronts, which retain a portion of risk for their own accounts. In the five-year period from year-end 2017 to year-end 2022, the direct premium for this group rose 130%, from $6.4 billion to almost $15 billion. This was due to both new entrants in the space and organic growth. While there is admittedly some non-fronting business mixed in with these numbers, this is still an impressive run.

One reason for this growth is the rapid expansion of delegated authority business over the last five years, which has outstripped the insurer capacity traditionally available for partnering with MGAs or program administrators. This provides an opportunity for new and more flexible capacity to enter the market. With so much third-party capital available and willing to back insurance risks, the use of fronting companies to funnel premium dollars to (often) offshore reinsurance vehicles has expanded exponentially.

Credit Considerations

It has long been recognized that underwriting specialty risks—whether involving targeted insurance lines, occupations/businesses, or geographies (or a combination thereof)—can prove more profitable than focusing on commodity-like casualty or property risks. As the U.S. P&C industry’s returns on capital have been stuck, on average, in the 5% to 10% range historically, the push into specialty coverages brings the promise of enhanced profitability and, with those higher earnings, expanding opportunities.

However, specialty insurance business also comes with risks. While a more laser-like focus on specific risk characteristics (and assuming appropriate reinsurance protections) should in theory allow a good underwriter to outperform industry-level averages, the same concentration of risk can also lead to substantial losses in the event of improper pricing and risk selection.

This is not a problem for the largest re/insurance groups, as they tend to have well diversified mixes of other business (often distributed across extensive intercompany pools) where any adverse impact of specialty risks becomes “diluted.” It is in the small to midsize specialty groups that credit risks can rise considerably if underwriting falters. We have seen several examples of this over the past year, with Argo Group, GuideOne, Hallmark Financial, James River, and Topa all forced to retrench after underwriting missteps.

The aforementioned rise of the fronting model also requires closer credit scrutiny. The solvency of fronting insurers depends almost entirely on the ability/willingness of their reinsurance partners to pay claims, given that, as primary issuers of a policy, they are legally bound to meet those obligations. While fronting insurers, in theory, carefully vet the financial quality of their reinsurance partners—securing appropriate collateral where required—there is always the risk of non-payment or breaching reinsurance limits, which could quickly compromise their financial health.

Outlook Good for E&S

Overall, specialty insurance in the U.S. P&C market has seen material growth over the past several years. While certainly turbo-charged by today’s firm pricing conditions, it appears that consolidation/ownership changes in the global specialty sectors since at least 2015 came in anticipation of an underwriting environment more keyed to segmented specialty offerings. We also sense that, even as rates cool—as they inevitably will—the strides made in the specialty insurance arena will persist and that this subsector of the U.S. insurance industry will continue to maintain its current market share or even expand over time.

Our role as credit analysts is to understand these trends and monitor the balance sheet structures and underwriting behavior of the substantially different market participants, from the global re/insurers down through the fronting companies and many new, privately backed startups. If history is any guide, there will be both triumphs and stumbles along the way.