IoT Success Stories Are Emerging in Commercial Lines

Brokers have an opportunity to better serve clients and help prevent risk.

Billions have been invested in insurtech over the past few years. Nowadays, we have startups listed with stellar multiples, as well as incumbents showing the ROI of their insurtech initiatives.

Back in late 2018, I wrote the book “All the Insurance Players Will Be Insurtech,” suggesting players in the insurance arena use data and technology as key enablers for achieving their strategic goals. And while there has been much talk of intermediary disruption, I strongly believe agents and brokers are here to stay—both on the personal and commercial insurance business levels—but they must embrace data and technology to do their jobs better.

We have read hundreds of articles over the past 14 months that have narrated the colossal insurance customer shift to digital channels due to the COVID-19 impact, in the luckiest cases supported only by a customer survey. This complex topic—which we will discuss in-depth during the Global Risk and the Post-Pandemic Future panel at the 2021 Global Insurance Symposium—is finally getting some grounding in data. As actual 2020 business figures come in, this “colossal shift” seems to be missing. Two datapoints to back up this assertion:

- Progressive is one of the champions of digital distribution in the U.S., however a material part of their business is still being done by independent agents. On personal lines their direct distribution has grown faster than the independent agent channel for many years. The direct channel quota, reported in their annual reports, was 49% in 2017, 50% in 2018, 51% in 2019, and 52% in 2020. This reflects a structural long-term trend, without any pandemic impact. If there had been a digital shift in the U.S. insurance market due to the pandemic, it would have impacted the book of a major player such as Progressive.

- According to the Italian auto insurance market consolidated data published by the Italian Association of Insurers (ANIA), the online channel represented 5.8% in 2017, 5.9% in 2018, 6.4% in 2019, and 6.4% in 2020. This shows no impact on insurance online sales due to the pandemic.

Traditional insurance distribution channels have demonstrated their resilience, but it is vital to explore how these channels can leverage technology trends as we go forward.

IoT-Based Risk Prevention

With more and more data available in the current hyperconnected world, even more actionable information is available, such as the information surrounding specific claims. Using this data makes incident prediction possible, which can lead to risk prevention. IoT-driven risk preventions are at an early stage of maturity in insurance. As analysed by a recent Geneva Association paper “From Risk Transfer to Risk Prevention: How IoT is reshaping business models in insurance,” the knowledge about these approaches is limited to a few people and the companies in an experimental stage. However, a handful of successful stories are emerging at an international level in all insurance lines.

Reducing risk for insureds can be either achieved directly—through real-time risk mitigation solutions when IoT data indicates that a client is getting into a risky situation—or indirectly, promoting safe behaviour over a longer period. Loss prevention and minimization activities have always been present among insurers’ activities, however IoT allows it to be done better.

Current property risk initiatives represent some of the most common approaches to direct risk mitigation. Actions triggered by a risky situation—such as the detection of low temperature on a pipe and the warning dispatch to the client or even an automatic shut-off valve—allow damage to be avoided. At the same time, timely containment actions enabled by constant IoT-based property monitoring—such as the leak detection done by a simple water sensor—allow minimization of the consequence of an incident that has already happened. This prevents the insured from often arduous recovery, or reconditioning, and prevents the insurer from expensive claim payments.

The indirect prevention option, promoting safer habits, intends to guide toward a long-term and lasting change in behavior that will reduce expected deaths, injuries, property damages, and other insured events. The creation of safety culture and awareness have always been part of the insurance sector’s role in society, and it starts from the evidence that the expected losses can be modified by human behaviors – from smartphone-distraction on auto risks to the type of management on commercial liability.

In commercial lines IoT-based approaches are more recent; however, behavioral change aspects have been an integral part of the recent wave of IoT-based innovation. These approaches can target two different levels: corporate and employees in the field who are responsible for behaviors.

Loss control teams can use IoT-based insights not only to leverage objective and more detailed information in their current activities, but also to provide digital tools that give corporate clients a better awareness of the causes of losses so they can implement adequate managerial actions. IoT-based loss control solutions also allow for this approach to be delivered to smaller corporate clients and remote locations.

Employee reward programs, similar to the rewards frequently used in personal lines, are also emerging. This trend is starting in the commercial auto business where drivers’ safer behaviors within a fleet are rewarded.

All the success stories at an international level—both in personal and in commercial lines—have been characterized by the usage of one or more of the above use cases to create economic value and to share part of this value with the relevant stakeholders. The value is mainly shared both with clients (e.g., discounts and cash back) and agents/brokers who distribute the product (e.g., additional commissions).

Engaging Brokers on IoT Programs

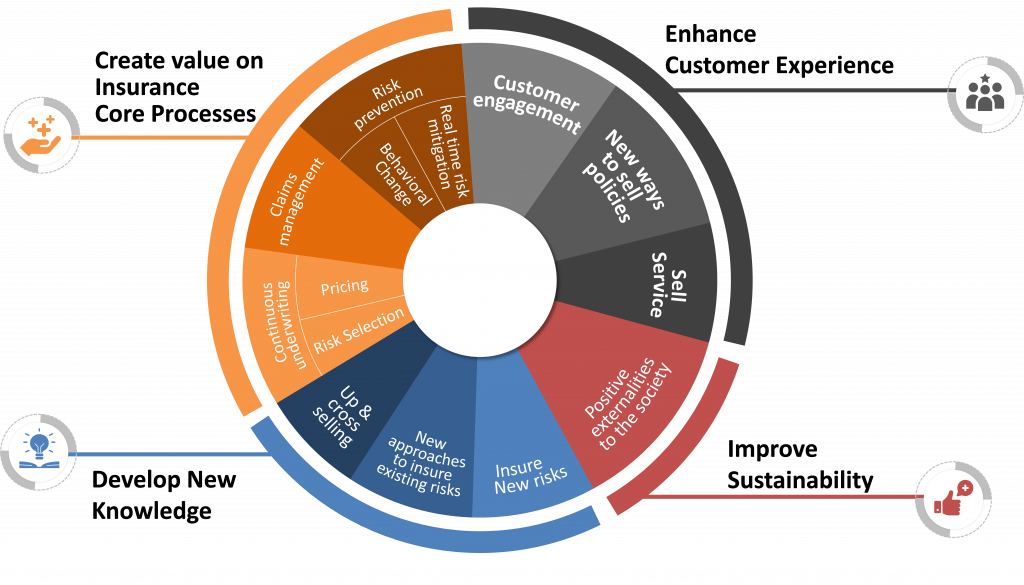

IoT solutions that connect insurers with policyholders and their risk allow for an improved customer experience, value creation on core processes, new knowledge deployment, and improved sustainability in the larger society.

Looking at insurers’ experiences in different business lines, four key aspects are emerging as best practices in engaging brokers with the go-to-market of IoT insurance programs:

- Share with brokers the vision about the IoT program, including a specific focus on the benefits for them such as the retention increase seen in many of the successful IoT-based insurance initiatives.

- Create processes which valorize the broker role in curing the client, e.g. sharing IoT-based insights about the risks which allows the broker to provide better advisory along the risk lifecycle.

- Design the go-to market around the broker needs, removing all the unnecessary frictions and providing the necessary support tools for the sales process.

- Adequately remunerate the new activities requested.

Nothing happens overnight in the insurance sector; some insurers will take a while to define their vision about the usage of IoT in commercial lines and their journey will take years from the first pilots to the scale-up.

This represents an opportunity for the most dynamic brokers in the market. Brokers with deep knowledge of their clients’ business and risks can develop their own vision about the usage of IoT data. They can find the tech players necessary for executing it and partner with an insurer to build an insurance program which rewards the presence of the IoT solution with better conditions and price for clients.

This is not a theoretical scenario, but something that has already happened in the U.S. market. A few of the most interesting IoT-based insurance initiatives—both in commercial property and general liability—were introduced by brokers with an adequate innovation culture and a specialistic knowledge about the risks they were insuring.

Matteo Carbone is founder and director of the IoT Insurance Observatory; NED and chairman of the Innovation Advisory Board at Net Insurance; and Global Ambassador of the Italian Insurtech Association (IIA). He will be a featured speaker at the 2021 Global Insurance Symposium (June 28-30).