Save Yourself

With few traditional plan levers left to pull, employers and their brokers are forging individual paths to reduce healthcare costs.

Unsurprisingly, healthcare costs are expected to rise again in 2026.

Surveyed by Mercer, more than 1,700 U.S. employers projected a 6.5% average increase in the total health benefit cost of every employee this year. That would be the highest since 2010 and the fourth straight year of significant increases, including 4.5% in 2024 and 6% in 2025. Between 2013 and the COVID-19 pandemic, healthcare expenses rose between 2% and 4% annually, according to Mercer data.

Employer healthcare costs continue to rise, with one report projecting a 6.5% average increase per employee in 2026. In this environment, organizations are seeking their own paths to reduce expenses without undermining their workers’ care.

Options include reducing pharmaceutical costs by contracting with pharmacy benefit managers that commit to transparency and directing insureds to biosimilar versions of name-brand drugs. There is also growing interest in direct contracting with healthcare providers.

One insurance company found that clients can lower costs by 20%–30% through these types of measures. Sources caution, though, that they must fit with an employer’s culture to prevent potentially disastrous results.

The cost of healthcare has become a major pain point for employers and employees alike. In response, employers are raising prices on products and postponing wage increases, while employees are forgoing medical treatments and skipping necessary prescription medications. Both tactics can decrease health outcomes and often cause greater spending down the line when health conditions deteriorate.

For many employers, there’s no clear fix to the spending surge. Traditional plan options to lower expenses have netted only limited benefits. High-deductible health plans push the cost to the employee; wellness programs have low uptake and little data supporting their efficacy; value-based care is difficult to implement; and pharmacy costs continue to rise even with the growth of transparent pharmacy benefit managers (PBMs).

Instead of passing more costs on to employees, some employers are charting their own path forward to contain costs. They are rewriting vendor contracts, overhauling prescription drug plans, and contracting directly with local healthcare providers. While these cases are anecdotal, they could point the way for other businesses to save themselves and their workforces money.

“We’re seeing the highest year-over-year increases in about 15 years, and no one is immune; no one has really been able to avoid it completely,” says Kevin Baker, principal and head of the actuarial group at brokerage Brown & Brown. “There’s not a lot of runway left on the plan side, employers have used all of their options there. We have 800 different vendor partners to use on any client to create a mosaic [of healthcare solutions] specifically for an employer. This takes effort, coordination, and data movement. That is the price of poker if you want to reduce costs.”

Another Day, Another Dollar

According to a 2025 report by Imagine360, a healthcare solutions provider for self-insured employers, healthcare services use rose 47% from 2010 while prices grew by 31%. Among employer plans, price is the main driver of cost growth. For hospital care, which accounts for a large portion of medical spending, employers pay an average of 254% of Medicare rates for inpatient and outpatient services. That means some pay much higher percentages. According to KFF, the average cost per inpatient hospital day in the United States in 2021 was $2,883; by 2024 (the most recent year for which data was available) it had grown by 14% to $3,297.

“We actually don’t see utilization driving the majority of spending increases on the commercial side— it’s much more about the prices being charged, especially in hospital settings,” Roslyn Murray, assistant professor of health services, policy, and practice at Brown University, said in the report. “Even when utilization stays flat or only goes up slightly, overall spending continues to rise because of the negotiated rates.”

Pharmacy spending accounted for 27% of employer-sponsored healthcare costs in recent years, the Imagine360 report said. (The remainder of spending was for inpatient and outpatient services, with outpatient accounting for roughly 50%.) UnitedHealth Group said in a separate analysis that the annual prescription drug cost per insured individual rose by 134% between 2014 and 2024, from $694 to $1,626. Most of the increase was due to the rising cost of drugs, not an increase in prescription volume. Should this trajectory persist, prescriptions could account for 32% of employer health spending by 2030 and 38% by 2035, the report’s authors estimated.

Specialty drugs represent more than half of prescription spending, but employers’ newer fear is outside the specialty realm: glucagon-like peptide-1 (GLP-1) agonists. Use of GLP-1s, which manage blood sugar and are used to treat diabetes, obesity, and heart disease, increased from 5.9% of employer pharmaceutical spending to 16.5% between 2021 and 2023. Employer coverage of the drugs grew by 8% from 2023 to 2024 and three of the top five drugs responsible for rising employee costs were GLP-1s, according to the Imagine360 report.

The Pricing Fallout

Cheryl Larson, president and CEO of the nonprofit Midwest Business Group on Health (MBGH), says about 27% of its members report higher-than-expected increases in healthcare costs this year. The rise in costs is causing pain for employers and plan beneficiaries.

Companies are making cuts that impact employees and customers to offset these healthcare expenses. In a 2026 survey of CFOs, Mercer found that more than one-third of their organizations reduced spending on other benefits and tapered wage growth in the preceding two years due to healthcare cost increases. Another 26% increased prices for products and services while about one-fifth slowed hiring or laid off employees specifically because of growing healthcare expenses. Only 21% of the CFOs in the survey said their organization could sustain more than 5% to 6% growth in costs over the next three years.

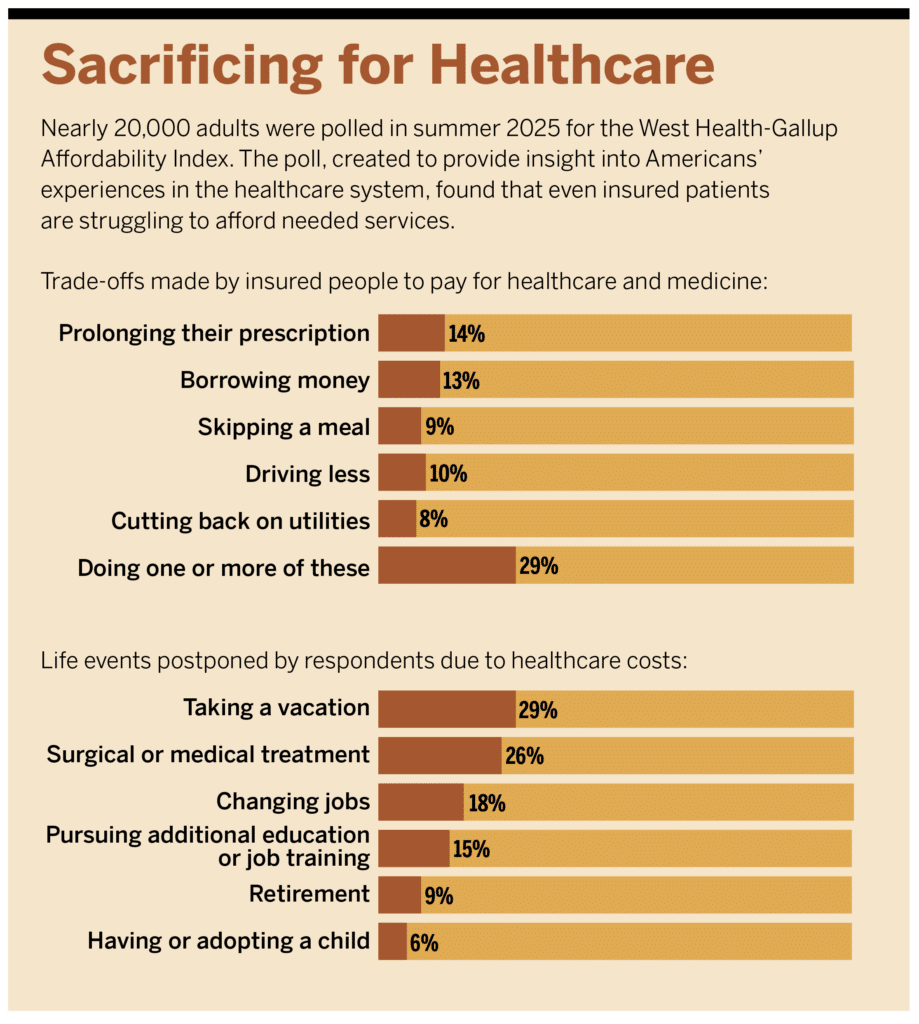

Employees are also struggling to manage their own healthcare spending. An April 2026 report by KFF said 43% of U.S. adults acknowledged not taking medication as prescribed in the prior year due to cost. About one-third used an over-the-counter medication instead of a prescription, 27% didn’t fill their prescription, and 19% cut pills in half or skipped doses to make the drugs last longer. Roughly one-third of those surveyed also said they skipped or put off getting care because of the cost, and about the same percentage worried about affording their monthly insurance premiums.

It’s difficult to pinpoint exact data on the effects of medication non-adherence—when someone does not take their medication as prescribed—but it has been estimated to account for at least 125,000 avoidable deaths each year and $100 billion annually in preventable healthcare costs.

Vendors Under Review

In this environment, some employers have begun to eschew traditional options and revamp their entire health plan environment. That means evaluating all partners in the ecosystem, including brokers.

In a 2025 McKinsey Employer Health Benefits Survey of roughly 1,900 employers, respondents cited the need for a broader range of solutions and lack of proactive help with managing costs as two of the top three reasons for switching brokers.

Dave Chase, co-founder and CEO of the nonprofit organization Health Rosetta, recommends that employers reevaluate their benefit consultant relationship every couple of years, including reviewing their contracts.

Chase recommends employers write an ideal contract and compare it with their existing broker contract. Employers can then pick and choose the points to focus on based on where they think they can save the most money.

Baker says it’s the employers’ fiduciary responsibility to ensure all plan funding is used appropriately. Most savings are found in carrier and PBM contracts, but broker contracts are also included in that consideration. Brown & Brown is fully transparent regarding its fees and does not use a billable-hours structure. Instead, the brokerage has a set fee with clients and rarely tell businesses that any service is “out of scope.”

Many Brown & Brown clients have become increasingly tactical about a range of contracts, including carriers, stop-loss, and PBMs.

“They are going out to the market to get the best pricing terms, not just renewing as-is with their incumbents,” Baker says. “We see roughly one-third of our clients with their PBM out to bid and the other two-thirds strongly considering it in the next one to two years. So, it is top of mind for practically every client. We recommend evaluating the market every two to three years for PBMs.”

Indeed, nearly three-quarters of respondents (73%) to a 2026 employee benefits survey conducted jointly by McKinsey and The Council of Insurance Agents & Brokers said that their employer clients are either actively trying to consolidate vendors or considering consolidation.

Baker has also begun auditing clients’ vendors frequently. He says Brown & Brown evaluates new vendors for their potential and pulls the plug on underperforming businesses instead of “putting them in place and wishing for the best.”

“Vendors are on a short leash because it’s harder to justify spending money if they [employers] are not getting that return relatively soon,” Baker says. “They have about two to three years to show their value.”

Going Direct

One strategy that is gaining steam is direct contracting. A 2021 MBGH survey of larger employers found just 9% had direct primary care contracts in 2021 and 17% were considering the model. In 2024, a wider survey showed that 75% of employers were in some kind of direct contract model. Among those using direct contracts, about 60% were companies with fewer than 5,000 employees.

When Russell DuBose, vice president of human resources at Alabama screening and fabric manufacturer Phifer, analyzed the company’s healthcare plan, he recognized the need for greater employee use of primary care. In 2016, fewer than 40% of Phifer’s 2,700 covered lives (including about 1,200 employees) had a primary care provider. With a traditional PPO plan, a disproportionate amount of its healthcare dollars were spent on expensive specialty care—40% of spending was for primary care and 60% was for specialty treatment.

“Our entire healthcare plan was reactionary,” DuBose says. “There was nothing going on that was preventive. Without evaluating our plan, I don’t know how long it would have taken us to stumble on the revelation that primary care was largest missing piece in our plan design, and we had no real remedy in our approach to fix that.”

To fix its primary care dilemma, Phifer constructed an on-site health center where it now offers primary care, urgent care, occupational health, a chiropractor, physical therapy, behavioral health, and a lab. The company supports remote employees through direct primary care—a model where the employer pays a primary care provider directly, often through a monthly membership fee, and plan members pay nothing to use that provider. Through this model, the number of Phifer plan members with a primary care provider doubled to 80% in 2025.

This approach generally excludes insurers from the process and can earn employers discounts based on volume of patients sent to the direct providers.

Beyond primary care, Phifer has 30 direct contracts with what DuBose calls a second level of care, encompassing imaging and specialists such as dermatologists, orthopedists, and cardiologists. When plan members go to these preferred providers, there is no cost share.

DuBose says direct contracting shaves about 20% off the cost of every procedure; Phifer saves $1.2 million annually for both primary and specialty services. All direct contract services are fully paid by the plan; members save an average of $1,200 annually by not paying out-of-pocket costs. The company provides nurse navigators to assist members with accessing these services.

Employees save money when using these providers because there is no copay. Employers lower costs when they can negotiate good rates, often a percentage of what Medicare pays for services. In the 2024 MBGH survey, 47% of employers said they think direct contracting can control rising costs.

Direct contracting hasn’t always been available for smaller businesses that don’t have enough employees to negotiate with providers. It’s also been a non-starter in rural markets (and others) with limited competition or where providers won’t budge on prices. But use cases have demonstrated that this approach is not for only large companies or ideal markets.

St. Louis-based insurance provider Level Health contracts for all its 150 employers through aggregating these clients, most of which are small businesses. St. Louis has three major health systems, which compete for market share. Outside the city, in rural areas, Medicare and Medicaid cuts have providers seeking to bring in more commercial payers.

“The value proposition is for all parties involved: hospitals give us a better set of rates because we can direct care to them, get them out of the collections business, and pay them promptly,” says Level Health founder and President Adam Berkowitz. “In turn, employers receive better premiums and employees enjoy health plans with zero-dollar deductibles.”

Level Health provides level-funded insurance plans—self-insured hybrid plans where employers pay a monthly amount for healthcare services and are shielded from high costs by stop-loss coverage. The organization contracts directly with providers by evaluating service lines of local hospitals and other providers. Level Health builds a contract with a scope of service and sets fees on which employers and providers agree. The plan guides members toward these preferred providers by lowering or eliminating copays for their services. By aggregating its book of small businesses, Level Health can bring some bulk to a negotiation with local hospitals and lower the price of services.

Level Health contracts with Saint Francis Medical Center in Cape Girardeau, Missouri. The cost for services is less than twice the Medicare allowable rate, where traditional PPOs would pay at least 300% that rate, Berkowitz says. Level Health also contracts with Mercy, a major Catholic health system in St. Louis, to receive the hospital’s most competitive commercial rate, which Berkowitz says is between 20% and 50% of the organization’s commercially contracted rates with other insurers. This direct contracting model translates to lower spending for clients like Schaefer Autobody, a 200-employee company that saved $3.5 million in healthcare costs over three years.

“Our goal is to have fewer vendors and less touchpoints in the system; cleaner models of payment and benefit design,” Berkowitz says. “Thirty to 50% of what we pay is just bloat in the system, so if we can work with local doctors and providers and find an efficient way to pay for those services, we all win.”

A 2023 report compared the cost of bariatric surgery, major joint replacement, and spinal fusion under traditional insurance and direct payments from self-insured employers. The differences in costs for the procedures in traditional versus direct payments were: $26,509 and $24,909, $38,821 and $31,678, and $100,178 and $71,014, respectively.

Some hospitals are seeking out opportunities to partner with employers, showcasing what they do better than their peers in the market, says Jeff Bak, president and CEO of Imagine360. Having a vast network of providers is great for access but bad for cost control, according to Bak.

“What we see are inflated inpatient and outpatient costs and employers who don’t have a good handle on the cost differences between hospitals in a certain geography,” he says. “There can be a two- to three-fold variance in cost for different procedures. And that unit cost challenge is material.”

Imagine360 tries to partner with one quality system in an employer’s market. When direct contracting with one high-quality system in a market, a competitive rate is secured, and members are steered to utilize the contracted healthcare system.

In markets where Imagine360 does not have direct contracting partnerships, it uses reference-based pricing with facilities. With reference-based pricing, Imagine360 uses the hospital’s published charges plus a 12% margin or Medicare fees plus 20% (which often ends up being about 140% of Medicare’s rates). These rates protect employers from high-cost claims, which Bak says are common in many traditional plans. Hospitals have become more amenable to this pricing over time, Bak says. About 15 years ago, about 85% of providers accepted that reimbursement and 15% fought for more. Today, about 97% accept it and he has to work “around the edges on the 3% with other tactics” to reduce employers’ costs.

Many employers that use direct contracting allow employees to see providers who are out of that network. Patients who go outside the contracted organizations just pay more for their care.

“A lot of folks say they are never going to change their doctor, but when something is free and something else costs more, it’s amazing what they choose,” Berkowitz says. “But we don’t want to disrupt someone’s relationship with their pediatrician or obstetrician. At the end of the day, that’s not where the high cost is. What we want is, if they need surgery or end up in a hospital, we want them to choose the lower-cost providers.”

Rethinking Prescriptions

About 51% of MBGH’s members use one of the big three PBMs (CVS Caremark, Express Scripts, and Optum Rx, which together process nearly 80% of all prescription claims in the United States), Larson says. But in surveys, the organization found that 48% of members are looking for a change.

In the 2026 McKinsey–Council benefits survey, respondents chose PBM contract optimization as one of the top three cost containment levers used by their clients, and 58% of respondents noted that it offered either a 3:1 (34%) or 4:1 (24%) return on investment.

MBGH is now selecting two transparent PBMs (which commit to passing all discounts and rebates back to health plans and to providing detailed data about their costs) as endorsed partners in the Midwest Health Purchasers Collaborative, a purchasing arm of the organization. It wants partners that will avoid what Larson calls the “usual suspects” that increase pharmacy costs, such as spread pricing and rebates, while still providing medication adherence and care navigation support.

Brown & Brown’s Baker says his clients spend about 55% of their total pharmacy output on specialty drugs, and that amount is rising. So, these savings can net employers hundreds of thousands of dollars per year. For instance, a plan that steers patients to biosimilars can save thousands, or hundreds of thousands of dollars annually. Biosimilars are copies of biologic drugs that work in much the same way but generally cost much less.

Phifer found that a large number of employees were using Humira, so the company changed its formulary to provide biosimilars at no cost to plan members. Prices for Humira vary, but the discounted GoodRX cash price is upward of $6,000 for a month’s supply (the retail price starts at about $8,500, depending on the dosage). Several biosimilars are available for Humira; one, Adalimumab-adbm, starts at $550 per month on GoodRX (with a retail price starting at about $1,500).

Another way to reduce the cost of specialty medications is to monitor where they are provided. In a 2021 report, the Employee Benefit Research Institute found 15% to 84% differences in the cost of specialty drugs, depending on the site of service. Supportive cancer drugs, for instance, cost $5,444 when administered in-home and $10,078 in a hospital outpatient department. The analysis identified a total of $11.2 billion in potential savings for employers and employees by eliminating price differentials between hospital outpatient services and other locations for 25 distinct healthcare services.

Employers are addressing a rising pharmacy conundrum—GLPS-1s— by either not covering the drugs or increasing the clinical criteria for coverage. Some are only approved by the Food and Drug Administration (FDA) for certain conditions like diabetes and heart disease, not weight loss for people who aren’t obese. So, employers can choose to cover them only for their FDA-authorized use.

“We don’t have to make it so complicated, but do have to make some tough decisions,” Berkowitz says. “People are accustomed to getting what they want when they want it and thinking insurance should cover it. But it’s hard to argue that Ozempic is a preventive medicine.”

Phifer ultimately built an on-site pharmacy when DuBose realized employees’ medication adherence was in the low 60th percentile. Workers were receiving medication and filling it once or twice, then stopping.

The company has a zero copay for employees who fill their medications on-site because the cost of adherence outweighs any cost the plan would get from a copay, DuBose says. The pharmacy and on-site clinic are colocated, which drives business to both organizations. In rural areas, Phifer has contracted with three independent pharmacies that work through its PBM. The workforce’s prescription drug adherence jumped to over 90% by the end of 2025.

Finding strategies to save an employer money is the easy part in the healthcare system, Berkowitz says. The challenge is implementing changes that fit into the employer’s culture so that employees embrace the new approach.

“It can be devastating to employees if not done well,” he says.