Brokers Deploy New Pharmacy Strategies

Adapting to the changing pharmacy benefits space requires new expertise in a complex area.

No other single area in healthcare in the last decade has created more affordability issues for employer-sponsored insurance plans and patients than drug price increases, which have been frequent and wide in scope.

As we enter 2023, the Inflation Reduction Act will introduce major new reforms in Medicare to rein in pricing, constituting the biggest shake-up of drug pricing regulation in decades.

To understand the impact of transparency efforts in the complex and opaque pharmacy supply chain, we interviewed seven of the leading benefits consultants around the United States. In particular, we focused on pharmacy strategies and capabilities being brought forward by benefits brokers and consultants to help clients. Here is a summary of their collective responses.

Q

There is no one-size-fits-all approach regarding pharmacy benefits management. The right strategy is largely based on the appropriate drug mix and distribution network. True or false?

A

True. The goal is to ensure members receive needed medications and practice adherence at the lowest possible net cost and highest quality for the plan sponsor and plan members. Each health plan has different demographics. This means that specific strategies, such as specialty drug exclusions, can be leveraged in groups with appropriate demographics without compromising access for most members.

One broker commented, “We just attack the spend in every case,” indicating that clients are sometimes apprehensive to make drastic changes to their plans. Still, once you show a client that an individual uses three different specialty medications to manage blood pressure ($2,500/year) and one change to a single generic drug can lower costs to $800/year, people begin to evaluate trade-offs logically.

Q

What pharmacy services are table stakes for brokers?

A

The minimum a broker can do is regularly review pharmacy key-performance metrics with plan sponsors to educate them on trends resulting from their current strategy. Two primary strategies brokers use consistently are (1) making sure specialty drug pricing is competitive and guaranteed and (2) ensuring that 100% of paid rebates go back to the plan.

One broker added, “If claims are going down, that is technically considered a win. Still, it’s difficult to measure return on investment, so we are making investments around measurement and asking ourselves how the programs we are implementing give us desired outcomes. Getting our data to work for us as opposed to us working for our data will help with this.”

Q

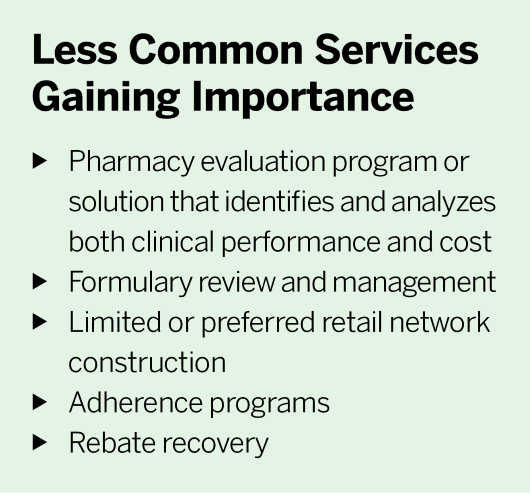

What pharmacy services are less common but growing in importance?

A

Interestingly, several brokers said they increasingly use pharmacy evaluation programs that identify clinical performance and cost to modify medications and pay for prescriptions. Some are even prioritizing hiring clinical expertise in-house, dubbing the talent search as “the next differentiator.” Brokers’ focus on clinical performance is notable. It reflects the new era of personalized medicine and begs the question of what role benefits consultants should have in providing individualized clinical advice. This is an important area to watch moving forward.

Q

What pharmacy investments are brokers making?

A

Unsurprisingly, expanding pharmacy consulting capabilities and pharmacy analytics led the list. Pharmacy subject matter expertise has been in hot demand by brokers in recent years. The market is changing rapidly, and as one broker commented, “If you’re not in pharmacy 100% of the time, you’re not in it.” Historically, brokers have partnered with third-party consulting firms or independent contractors. However, in the last few years, more brokers have been building in-house pharmacy consulting centers of excellence by hiring pharmacy-specific consultants and data analysts.

On the pharmacy analytics side, many brokers “can snorkel but aren’t scuba diving yet,” as one respondent put it. Larger brokerages are bringing this function in-house to enable more control over data quality and integrate other data sets to create a fuller picture for clients. However, more than half of the brokers surveyed still do not have a separate budget explicitly earmarked for pharmacy data and analytics.

Another area cited is creating firm-wide guidelines to assist with decisions on working with new “transparent” pharmacy benefit manager (PBM) market entrants. One broker said, “On a state, regional and national basis, PBMs and other pharmacy solutions are coming out of the woodwork.”

Q

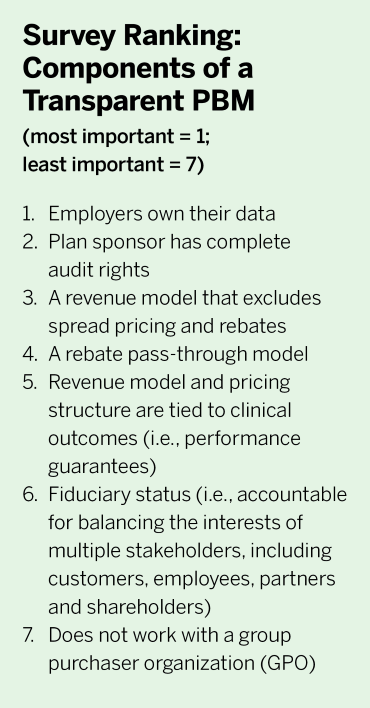

What are the essential criteria that make a PBM transparent?

A

Brokers responded unanimously that employers must own their data. Most believe that plan sponsors should retain complete audit rights and that transparency means these entities operate using a revenue model that excludes spread pricing and rebates or a pass-through rebate model. One broker also added that a transparent PBM is one that discloses all revenue sources associated with administering the pharmacy benefit and all third parties leveraged within their service model. A few brokers said they look for PBMs willing to be a fiduciary on the plan but this was not essential for a PBM to be considered “transparent.”

Q

How critical is transparency in the pharmacy industry?

A

Very critical. One broker commented, “Bodies are buried everywhere in the pharmacy space. It’s a black box still [based] on the dozens of different ways money is made from misaligned economic interests, and I also put us in the milieu. Brokers benefit from the status quo.”

Another broker commented, “If you aren’t in it every day, it’s easy to forget pharmacy is the most frequent and repeated health benefit with direct ties to every step in a patient’s medical care journey. Yet the pharmacy benefit is arguably the most opaque and complex, so someone might pay $5 for Atorvastatin, and her neighbor pays $350 for the same drug. The fact that prescription drugs are commodities—coupled with the widespread lack of information on costs and alternatives—makes pharmacy an ideal starting point for employers’ transparency initiatives.”

Multiple brokers speculated whether or not the new price transparency measures in the Consolidated Appropriations Act and Transparency in Coverage regulations can reconcile the information asymmetry that has plagued the pharmacy benefits space. The general consensus was not anytime soon. Price transparency on the medical side is only beginning to take shape. There are inherently more components and variables in pharmacy benefits, more data sources to integrate, and many involved parties across the spectrum of care. As another broker stated, “We need further data standardization and multiple layers of data transparency.”

Q

What areas of pharmacy benefits will keep you up at night in 2023?

A

1) RxDC Reports: Brokers are watching for when CMS will update instructions and provide guidance on the prescription drug and healthcare spending reports required under the Consolidated Appropriations Act before the next due date on June 1, 2023. The agency has been slow to publish FAQs and instructions. Many insurers, PBMs and employers have flagged snags in the system ranging from the inability for multiple service providers to provide data on the same plan to the lack of feedback from the online portal. For example, there is no way to verify whether the data reported meets compliance standards.

2) Inflation Reduction Act: Significant drug pricing reforms to Medicare begin to take effect in 2023, and all eyes are on whether the provisions will cause cost shifting in the commercial market. The major provisions include penalizing drugmakers that raise prices above the rate of inflation, capping annual out-of-pocket costs to $2,000 and, for the first time, handing the government the power to negotiate some of the most expensive brand-name drugs covered under Medicare Part B and Part D.

3) Gene Therapies: There is a lot of concern in the benefits market over gene therapies and medications coming to market in the next two to three years. Stop-loss carriers, brokers and employers are worried about how to build programs to manage utilization and anticipated costs. For example, on Nov. 22, the Food and Drug Administration approved the first gene therapy for hemophilia B. Hemgenix will have a list price of $3.5 million per use, making it the most expensive single-use gene therapy ever. However, as a rare disease, hemophilia B afflicts only about 6,000 people in the United States, and a smaller subset would be eligible for this new treatment. CSL Behring, the manufacturer, contends that financial exposure for payers will be somewhat limited.

The specialty pharmacy market is projected to continue growing by 8% per year through 2025, according to Evernorth. Growth will be largely driven by new-to-market drugs, which are anticipated to cost $62 billion. As more new drugs come to market, customized clinical strategies that address unique population risks will be a large area of focus.