To Whose Benefit?

Insurers and policyholders face real costs from the growth of litigation funding as an industry.

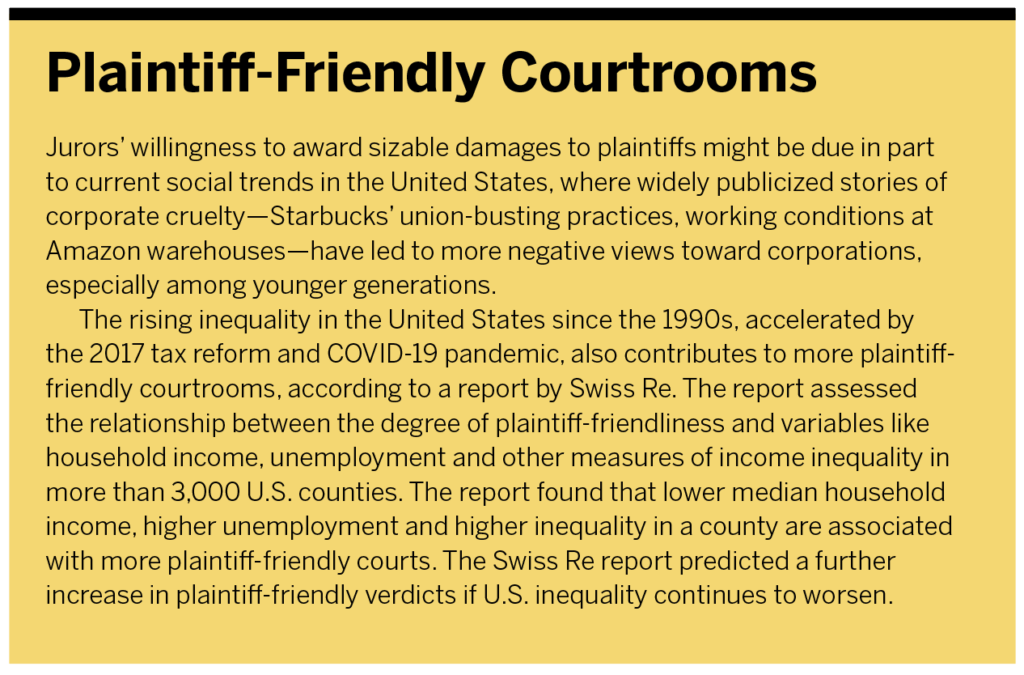

In the United States, the median award for general liability verdicts over $1 million increased from $8.2 million in 2010 to $10.3 million in 2019—almost 26%, according to a Swiss Re report on litigation funding and social inflation.

For vehicle negligence, the increase in the median award over $1 million was even higher, at 29%. Three-year averages show that not only is the median award trending upward, so is the average award for general liability verdicts, with a whopping increase of 224% from 2010 to 2019.

In 2021, 47 active commercial litigation funders in the United States had about $12.4 billion of assets under management and had committed $2.8 billion more to new litigation deals.

Third-party litigation funding (TPLF) can be particularly attractive for plaintiffs, who repay their funders only if they win or settle the case in their favor.

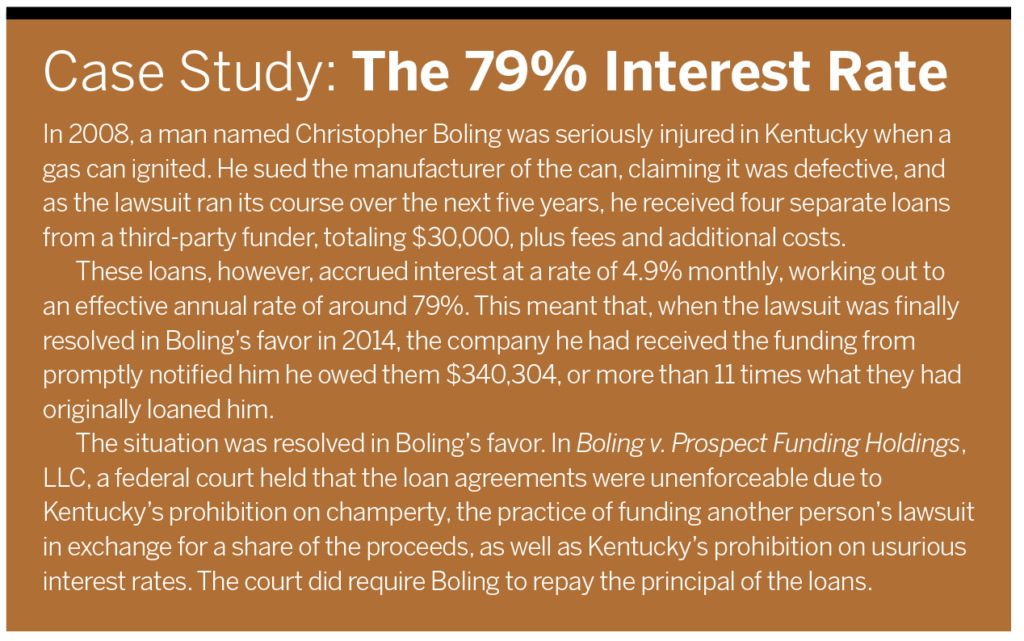

The interest rates on TPLF investments can be incredibly steep, especially in consumer cases.

A study of more than 600 cases by the American Transportation Research Institute (ATRI) showed the average size of a verdict in trucking accident litigation soared to $22.2 million from around $2.3 million between 2010 and 2018, or more than 850%.

Nuclear verdicts are considered one of the key drivers of social inflation—the trend of increases in carrier claims payouts above the general rate of inflation, leading to higher loss ratios for the industry and ultimately pushing the cost of coverage up for everyone as carriers struggle to remain profitable.

But verdict size is only a factor if cases are brought to trial and not settled outside of court, and more cases have been indeed moving to trial in recent years. “We’re seeing both a frequency issue, and we’re seeing a severity issue,” says Mark Berven, president and COO of Nationwide Property & Casualty. “More claims are moving into litigation, and the cost of resolving litigation is increasing at a rate that exceeds significantly general inflation trends.”

Third-party involvement is creating an environment that is not core to what the insurance policy is intended to address and cover.

Mark Berven, president & COO, Nationwide Property and Casualty

According to Berven, third-party litigation funding (TPLF) is to blame. He calls it “litigation abuse.”

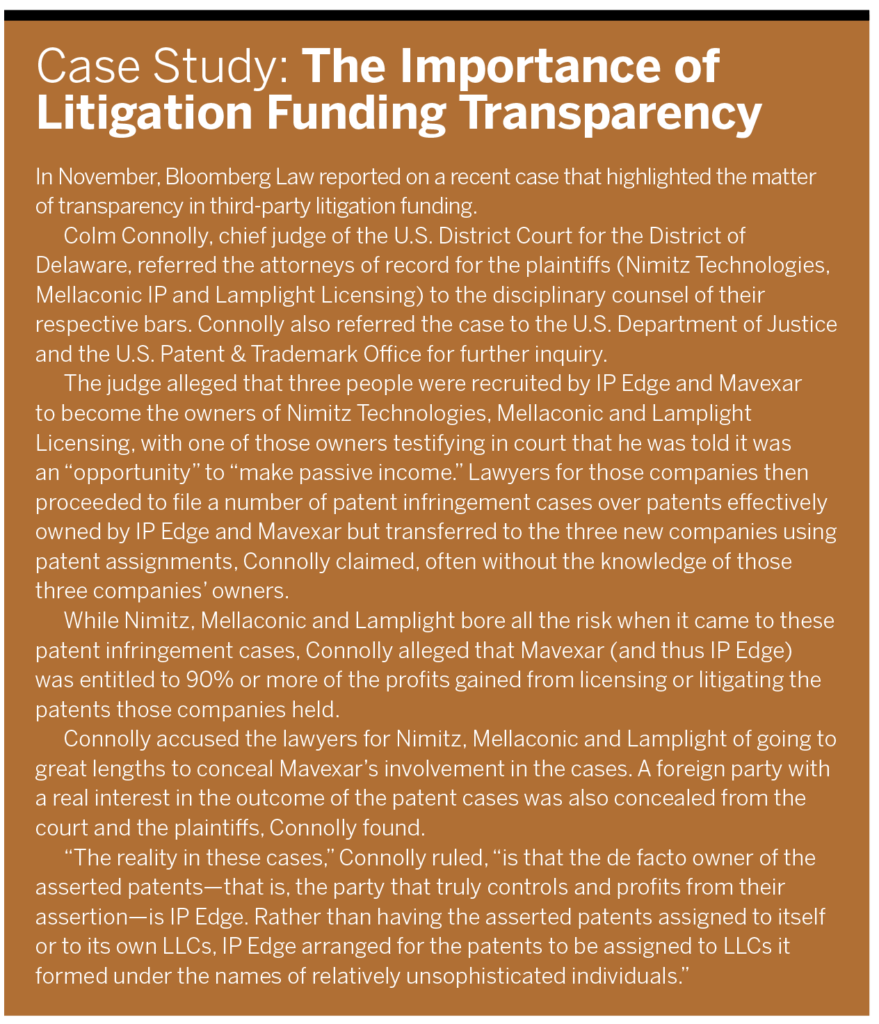

TPLF refers to a third-party providing funding to a plaintiff or law firm to enable them to pursue litigation in court. According to a December 2022 report by the Government Accountability Office (GAO), third-party litigation funders are typically private entities that specialize in such arrangements and get their capital from a variety of investment sources, among them institutional endowments and pensions.

Both GAO and Swiss Re report the 47 active commercial litigation funders in the United States have about $12.4 billion of assets under management and had committed $2.8 billion more to new litigation deals in 2021. According to Swiss Re, 52% of TPLF investments globally in 2021 were made in the United States. The GAO also notes there is a lack of publicly available information about the TPLF market, as there is no true central database on litigation funders and no federal laws requiring funders to report their data publicly.

Third-party litigation funding generally falls into a few typical categories: commercial, in which funders offer financing to corporations or law firms for commercial cases like breach of contract, antitrust or insurance claims; consumer, in which funders work with an individual to pursue a personal injury case; and mass tort, which involves a group of plaintiffs, as in a class action. According to Swiss Re, 38% of new TPLF investments were in mass tort litigation, followed by commercial (37%) and personal injury (25%).

Jeff Lula, a principal at GLS Capital, a commercial litigation funding firm, says consumer litigation is often treated differently by state regulators, “while commercial is separate—more sophisticated parties involved on either side.” Of course, all three types of third-party litigation funding matter for insurers, as any one could require a sued party to access its liability insurance.

Third-party litigation funding can be particularly attractive for plaintiffs, who repay their funders only if they win or settle the case in their favor. If they lose, there is generally no requirement for them to repay the funder. When a plaintiff wins a case funded by a third-party, the plaintiff repays the loan plus an agreed-upon return on the investment. And the interest rates on those TPLF investments can often be incredibly steep, especially in consumer cases.

More Just or Just More Money

Some argue that third-party litigation funding allows for more just outcomes by enabling cash-strapped plaintiffs to bring lawsuits or by evening the playing field between plaintiffs facing off against defendants with deep pockets. Lula notes there is historical context for this type of practice. “It’s not uncommon historically for friends, families and partners to functionally serve as litigation funders, even if that’s not how they would have thought of themselves,” he says.

In its 2022 paper on TPLF, the Insurance Information Institute recalled that advocacy organizations such as the ACLU or the NAACP have effectively served as third-party funders in the past, though in compliance with legal and ethical rules requiring disclosure of involvement.

That seems to have changed. The same Triple-I paper says that, of the 47 commercial litigation funders active in the United States in 2021, “41% of total commitments in 2021 across the funders were allocated to ‘big law,’ firms ranked in the AmLaw 200 according to gross revenue.” Those commitments, the report said, represented a “seismic increase” from 2020. “Only 34% of TPLF deals with large law firms were designated for client-directed, single-matter deals,” the report found, “indicating TPLF may play more of a role in keeping law firms profitable across their case load than in empowering individuals to fight for justice.”

The Swiss Re report also suggests that litigation funding is less beneficial for plaintiffs than it may appear. “Globally, 75% of TPLF investment supports commercial litigation and mass torts; and two thirds of TPLF settlements for commercial litigation go to large rather than small companies,” the report found.

Estimates in the report also show that, if TPLF is involved in a commercial tort case, the award would need to be about 27% higher than a case without third-party funding for the plaintiff to receive the same award. According to the report, these estimates were done with the assumption that “TPLF involvement will on average lead to higher award amounts and total liability costs, given that third-party funding allows plaintiffs to pursue better prepared cases further and make more effective use of the litigation strategies that have contributed to social inflation.”

At the end of the day, what we are trying to do is to invest money in good cases that we think are going to win and potentially be profitable to the plaintiff and ourselves. We probably have higher standards for merit for liability and for damages than plaintiffs, or sometimes even contingency lawyers, and wind up turning down 95% or more of the opportunities that come to us.

Jeff Lula, principal, GLS Capital

Does TPLF Drive Successful Cases?

A California State University at Long Beach study of consumer third-party litigation funding in 2022 found that restrictions on consumer third-party litigation funding from outright prohibitions to caps on interest rates and fees that funders can assess, increase the win rate at trial by 5.9%. The study also found that, with the same restrictions on consumer TPLF, the amount of tort lawsuits filed in that jurisdiction fell by almost 20%. Part of this decrease could be because some plaintiffs simply cannot afford to bring lawsuits without the aid of third-party funding.

Commercial TPLF, however, is a different story. “At the end of the day,” Lula says, “what we are trying to do is to invest money in good cases that we think are going to win and potentially be profitable to the plaintiff and ourselves. We probably have higher standards for merit for liability and for damages than plaintiffs, or sometimes even contingency lawyers, and wind up turning down 95% or more of the opportunities that come to us. There have been at times thoughts that litigation funding is promoting frivolous or unmeritorious litigation. But unmeritorious or frivolous litigation would be absolutely detrimental to the very core of what we’re doing. It would be so economically irrational, given what we’re trying to do as a business and as an industry.”

It’s a compelling argument, considering that litigation funding is inherently risky for funders, who lose their investment when plaintiffs lose their funded cases. “If anything,” Lula says, “we want to get rid of mediocre or bad cases as fast as possible, because it isn’t profitable to us.”

Globally, 75% of TPLF investment supports commercial litigation and mass torts; and two thirds of TPLF settlements for commercial litigation go to large rather than small companies.

Swiss Re, “US Litigation Funding and Social Inflation: The Rising Costs of Legal Liability”

The Cost of Third-Party Litigation Funding

The actual cost of third-party litigation funding to insurers can also be difficult to determine, given differences in jurisdictions, policies, awards and other factors. Dowling & Partners Securities, a Connecticut-based equity research firm, offered an estimate in its May 2023 “IBNR Weekly” newsletter. “For perspective on TPLF economics, every additional $1 billion of capital deployed would require a return of likely more than $2 billion to investors…. In order to produce a $2 billion return, lawyers would need to reap around $4 billion of contingency fees (assuming the fees are essentially split between the law firms & funders/investors). Assuming an approximately 40% contingency fee to award ratio would suggest the awards need to be more than $10 billion. So rough math is for every $1 billion of additional assets under management deployed, the resultant industry liability would be $10 billion.”

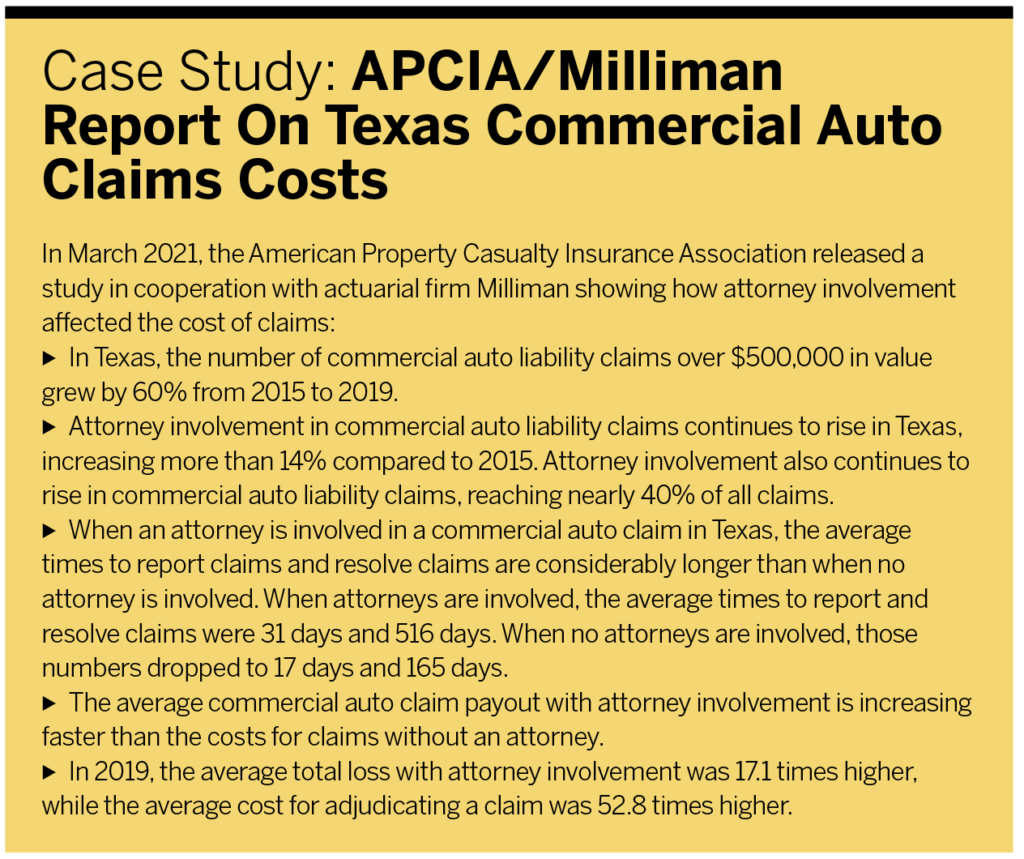

To get a handle on rough specifics, Dowling also dug into claims costs for two lines often affected by litigation: commercial auto and general liability. Its analysis shows claims costs for both of those lines steadily increasing over the past decade, with commercial auto claims costs increasing from around $3,800 in 2013 to almost $6,000 in 2022 and general liability claims costs essentially tripling from a little over $400 to over $1,200 in the same span of time.

That time frame does coincide with the rise of litigation financing. According to Lula, litigation financing as a business model “really started to grow in size around 10 years ago.” But litigation finance was not the only driver for claims costs for these lines. With commercial auto, for example, the increasing complexity of vehicles and the amount of technology packed into their chassis has contributed to the increased cost of claims.

Also following that trajectory is an increase in claim resolution time—the Swiss Re report found the average court case takes two months longer to reach a verdict compared to 2015.

All of this adds up. Chubb’s 2022 annual report notes, “Costs and compensation in the U.S. tort system amounted to $443 billion in 2020, equivalent to 2.1% of U.S. GDP, or $3,621 per American household. These levels are the highest since at least 2016 and have outpaced the growth in inflation and GDP over the same period. Only 53 cents of every dollar reach claimants, while the rest goes to litigation costs and other expenses—including the cut for the litigation funders.”

“Third-party involvement is creating an environment that is not core to what the insurance policy is intended to address and cover,” Nationwide’s Berven says. “It’s creating an environment that is creating more problematic solutions for what we do as general marketplace.”

Mandating Disclosure

Given the runaway costs, should governments step in? The existing regulatory field for litigation funding is already fairly complex, made more so by the fact many U.S. states had standing common law rules against “champerty,” defined by Black’s Law Dictionary as “A bargain made by a stranger with one of the parties to a suit, by which such third person undertakes to carry on the litigation at his own cost and risk, in consideration of receiving, if he wins the suit, a part of the land or other subject sought to be recovered by the action.”

However, many states have done away with their rules banning champerty, and some states, such as California and Texas, never enacted such laws. Only a handful of states have laws explicitly prohibiting the practice, including Alabama, Kentucky, North Carolina and Pennsylvania. Others, such as Delaware, have prohibitions against champerty but generally do not apply them to third-party litigation funding agreements.

For Berven, however, prohibiting litigation funding isn’t what he and the industry want to see in terms of regulation. “One of the biggest things that we in the industry are really looking for is transparency and creating a level playing field where knowledge is provided to all parties,” he says. “These costs are transferred to everyone directly or indirectly. The more that we can really emphasize that this is an environment that has changed dramatically, it is raising costs and there is no transparency about the involvement of third parties that have no real interest in this case other than return on investment—we need to do something about that.”

But there’s been little movement toward rules mandating disclosure of litigation funder involvement. There is no federal disclosure requirement, although federal courts in New Jersey and Northern California have implemented some form of disclosure rules. Colm Connolly, chief judge of the U.S. District Court for the District of Delaware, has issued standing orders requiring lawyers in his courtroom to report any third-party funding.

In Congress, Rep. Darrell Issa (R-Calif.) introduced to the House the Litigation Funding Transparency Act of 2021, which would require lawyers in class actions and multidistrict litigation to disclose to the court, the plaintiffs, and other associated parties if there is a third-party commercial enterprise that “has a right to receive payment that is contingent on the receipt of monetary relief in the class action by settlement, judgment, or otherwise.” Issa’s bill also would have required disclosure of a third party’s identity as well as the specific terms of the agreement.

At the same time, Senator Chuck Grassley (R-Iowa) introduced an identical companion bill in the Senate, but no action has been taken on either bill.

Senators Joe Manchin (D-W.Va.) and John Kennedy (R-La.) last fall introduced the Protecting Our Courts from Foreign Manipulation Act of 2023. The bill would require both parties in a civil action to disclose the involvement and identity of any foreign person, foreign state or sovereign wealth fund that has a right to receive payments contingent on the outcome of the civil action. The bill would also prohibit third-party litigation funding of U.S. civil actions by foreign states or sovereign wealth funds. To date, no action has been taken on the Senate bill.

Only 13 states have explicit limits on litigation funding or disclosure requirements, while three others don’t have statutes but their courts either prohibit litigation funding or mandate disclosure. Dowling’s analysis shows these states represent about 25% of total U.S. direct premium written.

At the state level, Berven says, Florida has set an example that he’d like to see other states follow. According to Verisk, bills proposed in both houses of Florida’s legislature “would require litigation funders to register with the Florida Department of State, post a surety bond and include certain terms and disclosures as part of litigation funding contracts.”

Berven supports those efforts to bring more transparency to third-party litigation funding. “I think it will lead to more effective litigation outcomes and strategies that still appropriately compensate harmed parties,” he says, “and avoid this financial element of litigation that really isn’t in support of those that need to be remedied.”

Montana’s recent law regulating TPLF could also be a model. It institutes a mandatory disclosure requirement in all civil cases, makes litigation funders jointly liable for the costs of a case, and imposes a 25% cap on the amount a funder can get from a favorable verdict or settlement. The law’s title specifies consumer TPLF as the intended target of regulation, Lula says, but it’s unclear if the law will also impact commercial litigation.

That ambiguity demonstrates the importance of understanding the distinction between consumer and commercial TPLF. Lula cautions that regulation should not be so overzealous in protecting consumers that it impacts more sophisticated companies that know how to protect themselves and their interests.

“There is pushback because they want to have profitable investments throughout the United States,” he says, “and wouldn’t want ad hoc legislation of litigation funding to interfere with that.”