Excess Exported

Legal frameworks that allow U.S.-style class-action suits are proliferating around the developed world. Access to justice or lawyers’ license to print money?

In the U.S. mass tort system, class actions are a huge source of claims against the casualty side of the P&C sector.

Now this American-made form of legal financial redress for the multitudes is emerging in various jurisdictions around the world. In this case, however, imitation is hardly flattery. While rebalancing the scales in favor of the little man, the worldwide emergence of new ways to bring group legal actions for compensation brings uncertainty and no small measure of consternation to commercial liability brokers and underwriters. In Europe, in particular, policymakers hope to avoid the perceived excesses of the American system while still reaping its benefits.

The worldwide emergence of class actions brings no small measure of consternation to commercial liability brokers and underwriters.

Mass tort regulations are firmly established in Australia, more restricted but growing in the United Kingdom, and taking hold in the European Union.

The popularity of U.S.-style “opt-out” class actions—once seen as anathema—are gaining ground.

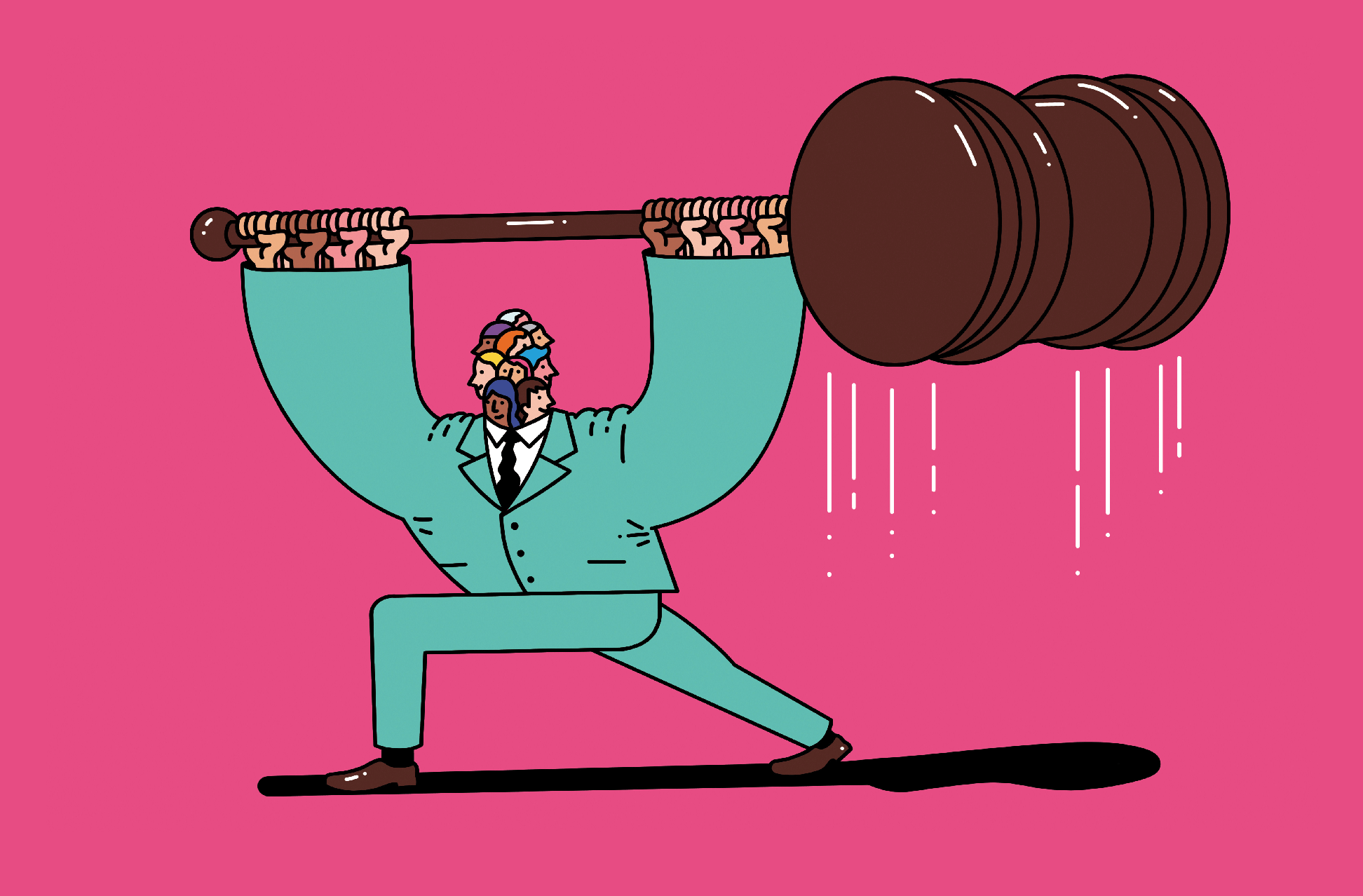

David vs. Goliath

The principle is simple. If an organization (a company, government or NGO) makes an error that affects multiple people in a compensable way, the organization’s specific liability to each affected individual (collectively, the class) can most efficiently be decided through a single legal action. When, for example, a company’s board of directors has been negligent in its disclosures to the detriment of shareholders, it makes eminent sense for those shareholders to be permitted to seek compensation through the legal system as a group rather than having to bring thousands of individual actions.

Notwithstanding the fundamental flaws of this approach—it assumes every class member’s entitlement to redress is equal, and attorneys typically receive a larger share of damage awards than any individual plaintiff—the system has enormous merit. It genuinely gives a collection of Davids a hand up in their battle against a negligent Goliath.

Many former U.S. jurisdictions have begun to introduce mass tort regulations to grant citizens exactly this option. Such regulations are firmly established in Australia, more restricted but growing in the United Kingdom, and taking hold elsewhere, including in the European Union, where a federation-wide framework is now being constructed. Notably, the permissibility and popularity of U.S.-style “opt-out” class actions—once seen as anathema—are gaining ground.

Opt-outs automatically make all potential litigants part of the action unless they actively choose to be excluded. That inflates potential top-line compensation totals to their maximum: an award to satisfy, say, two million product buyers will have to be a lot larger than for 200 actively disgruntled ones. One U.K. data-breach class action, for example, saw only about 9% of the class (grocery store employees) opt in. Had the suit been brought under an opt-out regulation, all 100,000 potential claimants would have joined the action, dramatically inflating the potential award (which ultimately was denied).

These large, sometimes dizzying totals attract and nurture a professional plaintiffs bar and encourage speculative financiers. Litigation funding, an emerging industry almost everywhere, sees speculators funding plaintiffs’ legal costs. Loans for legal expenses are repaid—with a substantial bonus—only when suits succeed.

The “ability to pursue claims on an opt-out basis and get the funding to do it is now expanding rapidly outside the U.S. and Canada,” says Francesca Richmond, a solicitor with law firm Baker McKenzie. “That expansion means that all corporates need to really think about cross-border class-action litigation now and account for it in their business planning, no matter what sector they’re in.”

England and Wales

Data abuse is the newest opt-out class-action battleground in England (which, with Wales, has different laws from the rest of Great Britain). Facebook has again been summoned to London’s High Court to face allegations that it failed to protect the personal details of about a million users. Two actions (both tied directly to the 2016 Cambridge Analytica-Trump campaign scandal) claim the social network sold private data without permission. Facebook has already been fined £500,000 ($697,000) by U.K. data protection authorities over the misstep.

The case is interesting for two main reasons. First, it’s opt-out, with all the plaintiffs’ virtual “friends” automatically enrolled in the class. Opt-outs have been allowed in England since 2015 but only as follow-on damage claims for breaches of competition law previously confirmed by the Competition and Markets Authority or the European Commission. Second, litigation funders are footing the bill. Balance Legal Capital, self-described as “providing commercial litigation and arbitration funding in the UK, Australia, and around the world,” stands to benefit from a claimant success.

We understand that litigation funders were behind over 70% of all Australian class actions filed and are looking broadly for causes of action.

Cameron Green, Head of International Casualty Reinsurance, Willis Re

Opt-out is currently being tested in the English courts in a data case against Google (a judgment had not been delivered by press time). Seven similar active cases await the outcome. Meanwhile, England’s opt-in mass tort system is maturing. With a court-approved group litigation order (GLO), multiple claimants pursue a defendant through a single action. The court decides who is eligible to join the class of claimants and sets up a register that each must join to take part. Cases are heard before a High Court judge rather than a jury.

Peter Rudd-Clarke, legal director at the London law firm RPC, says the introduction of GLOs in 2000 was considered “a significant moment,” but proceedings remain relatively rare. Only 109 GLOs have been made to date. That said, they are gathering pace in areas such as personal injury, fueled in part by “qualified one-way costs shifting,” introduced in 2013, which protects failed claimants from liability for defense costs. “Consequently, personal injury group litigation has prospered more than claims in other areas, such as environmental litigation,” Rudd-Clarke says.

Both routes to group justice go hand in hand with third-party litigation funding, which can be used alongside an after-the-event insurance policy to cover legal expenses and solicitors’ conditional fee agreements. The combination has potential to create serious conflicts of interest for insurers, who might find they are interested parties on both sides of the courtroom.

Litigation funding is already embedded in the English system. A decision in a massive, funded, opt-out case brought against credit-card provider Mastercard by the United Kingdom’s Financial Ombudsman on behalf of 46 million consumers is expected imminently. When the Court of Appeal permitted the class action, it declared: “The power to bring collective proceedings … was obviously intended to facilitate a means of redress which could attract and be facilitated by litigation funding.”

Class actions by investors against corporate directors and officers are less common in the United Kingdom than in the United States or Australia. This may be due to higher thresholds of proof for negligence and the U.K. regulator’s lesser emphasis on continuous corporate disclosure, says Cameron Green, head of international casualty reinsurance at Willis Re. But the opt-in nature of U.K. securities suits may also play a role. “We do not see such a significant volume [of securities class actions in England], which is still very much an opt-in jurisdiction for these types of litigation,” Green says.

As things stand in the United Kingdom, Rudd-Clarke says, “insurers of products are particularly exposed.” He cited some “notable examples” of U.K. group actions seeking redress, particularly for medical products and malpractice.

European Union: Opt-Out Is a Difference Maker

Rule changes are forthcoming in the European Union to ensure that a minimum facility for class actions exists in all 27 member states, some of which already have mass tort regimes. The European Commission’s Collective Redress Directive, in the works for more than a decade, must be incorporated into each country’s laws by the end of 2022. Brussels was “anxious to avoid importing what it considered to be the excesses of the U.S. class action procedure” but was “keen to address perceived barriers faced by individual consumers in obtaining effective and affordable redress in the context of mass claims,” according to international law firm Linklaters.

Once implemented, the new EU-wide rules will allow groups of claimants to seek injunctions, damages and other forms of redress but only for breaches of specific EU consumer protection rules, such as those for false advertising and unfair contracts. Local regulation can be written to allow group action over a wider range of injuries. Punitive damages are not allowed under the EU minimums, although third-party litigation funding is. More importantly for cross-border disputes within the European Union, actions can be brought only by nonprofit consumer protection organizations, which marks a major difference from the U.K. and U.S. systems, where actions are, in effect, brought by firms of attorneys.

Here, class action is not a fast lane. One case, against a bank, took five years just to start the formal procedure, and it can take twice as long to get the final verdict.

Piotr Cieślak, Chief Executive, MAI CEE

“Class actions are expected to increase throughout the EU,” says Willis Re’s Green, “but a significant difference remains between the European and U.S. systems in relation to standing and whether class actions are opt-in or opt-out.” Differences will remain between countries, too. In Germany, for example, claimants must actively join a class action by registering online, but in Belgium a judge can decide to define a class as opt-out.

“An opt-out system tends to be more effective in terms of including victims into the action,” says Frank Kroes, a partner in Baker McKenzie Amsterdam. However, Kroes says, opt-out clashes with the creation of “what, with a bit of horror, is usually seen as a U.S.-style claims culture. We don’t want that in Europe.” That inherent tension, he notes, leads to different national models.

Mass torts began in many European countries well before the European Union’s new directive. The Volkswagen emissions scandal, for example, led to ongoing class actions in Belgium, Italy, Germany and the Netherlands. In the last two countries, shareholders and car owners can take separate collective actions. The German system for shareholder suits was established specifically to handle the claims against Volkswagen.

National rules requiring the involvement of a consumer protection organization have not prevented attorneys from seeking a large slice of the pie. Early this year, German Volkswagen owners, represented by the nation’s Federation of Consumer Organizations, were offered a joint settlement of up to €830 million ($1 billion). However, the deal was derailed when the federation itself sought €50 million for its efforts. Volkswagen board member Hiltrud Werner said, “The lawyers’ unwarranted demand for €50 million was unacceptable…. The business practices of the plaintiffs’ attorneys should not have a negative impact on the customers.”

Less Impact Further East

The likely impact of the European Union’s slightly more permissive class-action rules appears to diminish in importance as one moves east. Jan Stok, director of the Central-Europe focused MAI CEE Insurance Brokers, reports that class-action suits have been possible in the Czech Republic, where he is based, for some time but have been very limited in scale. “We do not see them happening often,” he says. “Suits for compensation may be brought against government following the closure of various businesses, but neither if they will come up, nor the extent to which they will be successful, can be evaluated.” Stok says he has yet to see developments that indicate a trend toward class actions.

Nor are concerns rising in Poland, where the impact of the few cases heard under the 2009 Class Action Act has been insignificant. “Here, class action is not a fast lane,” says MAI CEE chief executive Piotr Cieślak. “One case, against a bank, took five years just to start the formal procedure, and it can take twice as long to get the final verdict.”

The current regime for mass torts in Poland has little or no impact on local insurers, Cieślak says, since most of the very few class actions cover pure financial losses, but policies generally do not cover such claims. Similarly, insureds facing employment-related mass torts are unlikely to find they are covered. Cieślak sees financial institutions professional indemnity as the only area of potential class-action impact for Poland’s insurers but expects losses to fall to reinsurers. “We do not consider class actions to be an important area,” he concludes.

Australia: Growing Financial Services Suits/Litigation Funding

Mass tort legislation was introduced in Australia in March 1992. It allows the Federal Court to hear class actions in a variety of areas, and 122 such actions were listed as “current” by the Federal Court in March. More than 550 have been filed since enactment of the legislation known as the “the Part IVA regime.” Originally associated with product liability claims, by 2009 the number of shareholder and financial services class actions had outstripped those for product liability.

Willis Re’s Green says many security class actions are fueled by insurers’ broad policy wordings, by the Australian Stock Exchange’s continuous disclosure rules (which demand immediate publication of any information which might reasonably affect a listed company’s share price), and by speculative financiers. “We understand that litigation funders were behind over 70% of all Australian class actions filed and are looking broadly for causes of action,” Green says.

An opt-out system tends to be more effective in terms of including victims into the action.

Frank Kroes, Partner, Baker McKenzie Amsterdam

In practice, fewer than a 10th of Australian actions ever make it to trial. Most are settled for average values of about A$55 million ($43 million), but Australia’s largest class-action loss, which arose from the Victoria bushfires in 2009, settled in 2014 for A$500 million ($387 million), according to Willis Re. Settlements exceeding A$100 million ($77 million) are not uncommon.

“The development and availability of litigation funding, increased access to information, and the growing number of law firms willing to represent claimants have contributed to the continued growth of class actions in Australia,” according to defense attorneys Ashurst Australia. “When class actions were introduced in 1992, there was concern it would result in a flood of U.S.-style litigation.” That hasn’t happened, Ashurst says, but a number of cases have been brought which otherwise would have lain fallow.

“Increased entrepreneurialism on the part of law firms representing plaintiffs and litigation funders has resulted in the commercialization of the class-action industry,” the lawyers believe. From another perspective, the Federal Court of Australia said: “The Part IVA regime has become an effective, sustainable, and well accepted system for Class Actions in Australia.”

Asia Pacific

Litigiousness is generally considered low across Asia, driven by its high cost, low awards, sluggishness, poor access and, in some cases, cultural or religious considerations. Despite these barriers, many countries have made legal provisions for group actions under varying circumstances.

Class actions have been allowed in New Zealand since 2009, but the system is opt-in and litigation funders must demonstrate that an action supports the public interest. Most class actions there relate to financial products or defective houses. China has legal avenues for class actions and has seen cases touching on public interest, product liability, environmental protection, workers compensation, and shareholder suits. However, progress remains slow in Hong Kong, where litigation funding is banned. Korean law allows for securities class actions and defective-product suits, but class actions against financial institutions are rare. They are increasing in number in Japan but so far are not considered a major concern. The country’s opt-in system tends to keep numbers down, and group litigation is used only for direct financial loss.

A COVID-19 Second-Wave Class-Action Upswell?

The question on everyone’s mind is whether nascent mass-tort regimes in the United Kingdom, Europe and Australia will be tested by a surge of COVID-19 claims. Commentators have observed the attraction for litigation funders and claimant solicitors of suits which could, for example, seek redress for classes comprising employees who contracted the virus at work during COVID’s second wave, when precautionary preventive measures were widely known. Lawyers have certainly spotted the pandemic opportunity in England, where 20 or so new claimant law firms with the word “COVID” in their name have been launched since lockdown. They at least will be hoping the virus is the new asbestos—but perhaps not quite as fervently as loss-hit casualty insurers will be praying it’s not.