Japan: A Tale of Three Insurers

Market Dynamics, Consumer Demand, Regulatory Updates, and More

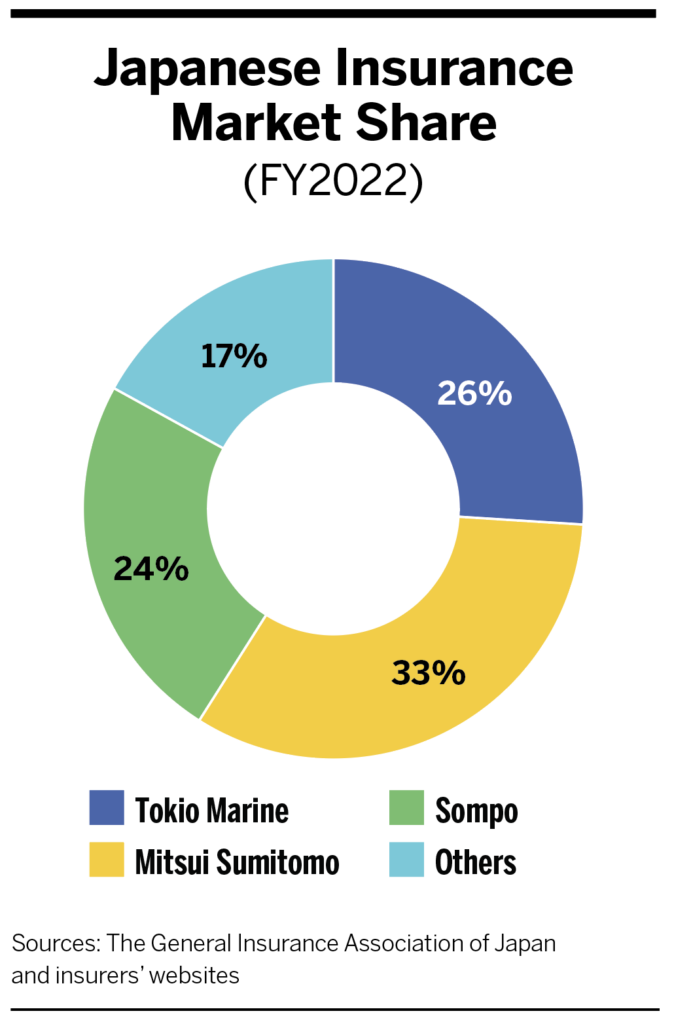

Japan’s insurance market is dominated by three companies: Tokio Marine & Nichido Fire Insurance, Sompo Japan Insurance, and Mitsui Sumitomo & Aioi Nissay Dowa Insurance.

These insurers occupy nearly 80% of the market share, with net written premiums totaling approximately $61 billion for fiscal 2022.

Multinational insurers find the market challenging, given its unique practices and traditions, such as the emphasis on paperwork and the tight relationships between Japanese insurers and their clients.

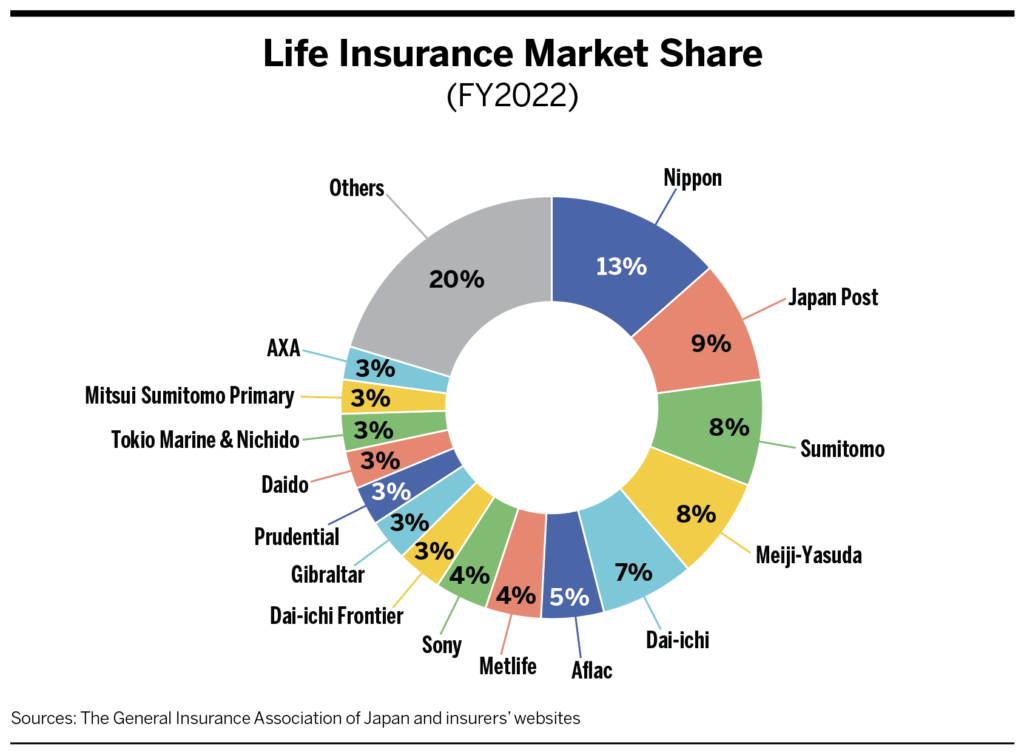

As of 2023, approximately 42 private life insurance companies operated in Japan, comprising 75% of market share in that sector.

The top three insurers by market share for group long-term disability in Japan are Capital Insurance Corp., Chubb, and Aioi Nissay Dowa. The leading insurers for medical and group personal accident are Chubb, AIG, and Sompo Japan.

There are no general taxes on insurance premiums in Japan. The only tax applicable is 10% on locally earned commissions.

Market Dynamics

Pricing

- Employee Benefits: The market remains stable, with less than a 5% annual rise in medical inflation. Foreign companies are generally keen to provide above-market employee benefits, including long-term disability and additional medical benefits over and above the 70% cost coverage from the national health benefit program.

- Property: Rates for property and business interruption lines have increased by 5-10% per year. Rates are also increasing for certain industry verticals, including energy and professional services, with energy up by 10% or more. Fire and all-risks policy rates have also jumped by 10% on average twice in the last five years due to losses from natural catastrophes, particularly earthquakes, typhoons, floods, and snow. Recently Japanese insurers have also been revising the property premium rate every two years as a result of increasing nat-cat losses. The most recent revision, on Oct. 1, 2022, increased the rate by an average of 15%. Another rate increase is scheduled for fall 2024.

Capacity

- Employee Benefits: For group life policies, the maximum limit varies from ¥20 million to ¥100 million (about US$127,000 to US$635,000), depending on the group size. Group long-term disability is ¥1.5 million (US$9,500) monthly per person. Group personal accident with medical pays out ¥15,000 (US$95) per day for inpatient and outpatient care, with a ¥3 million (US$19,000) cap for medical expenses.

- Property: Underwriting capacity remains stable for most coverage lines. However, large losses resulting from natural disasters in recent years have led to a 5-10% decrease in capacity for property lines, with many insurers specifically limiting their underwriting capacity for flood and windstorm risks.

Notable Offerings and Consumer Demand

- Employee Benefits: One of the defining aspects of the Japanese life insurance market is the nation’s aging population. In 2022, the birth rate fell to a historical low of 1.26 (the average for the number of children per woman), substantially below the replacement rate of 2.06. The need for large death benefits is declining; however, growth in dual-earning households, low birthrates, and the aging population has increased the need for medical, pension, and nursing care coverage.

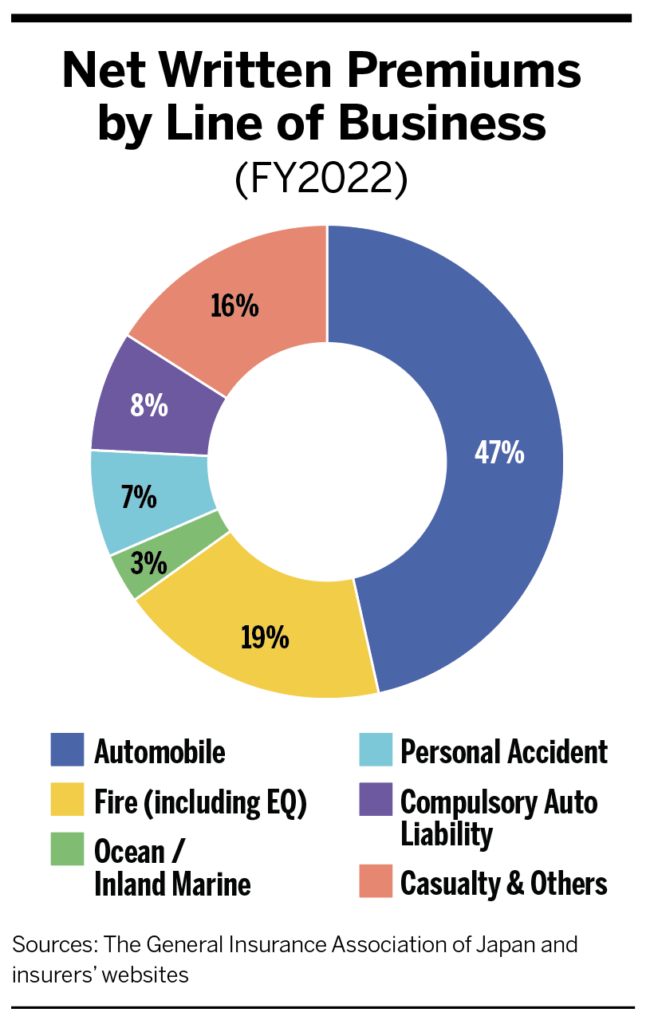

- Property: While nearly all firms purchase property damage coverage, business interruption coverage is not widely used. An estimated 80% of large corporations have policies, but only 20% of smaller companies do. This low penetration is attributed to high premium costs and the perception that business interruption claims are rare. Aioi Nissay is the only Japanese insurer to offer business interruption earthquake coverage to multinational companies. Auto and compulsory auto account for nearly 55% of total net written premiums industrywide. Only 34.6% of households are insured against earthquakes. Casualty and other lines of business have grown steadily to 16% of total net written premiums over the past 20 years.

Regulatory Update

Pensions

There are two main pension schemes: the National Pension for all residents and Employees’ Pension Insurance (EPI) for employees of private companies. The current retirement age for EPI is due to increase from 60 to 65 for men by 2025 and for women by 2030.

Updated Solvency System

The Financial Services Agency has been researching and developing an economic value-based solvency system since 2010, assisted by a council of experts. The new framework and the official regulations are expected to be implemented in fiscal 2025, parallel to the introduction of the Insurance Capital Standard by the International Association of Insurance Supervisors.

International Financial Reporting Standard 17

Implementation of IFRS 17 is not compulsory in Japan, as official disclosure requirements are still reported based on the nation’s generally accepted accounting principles. However, the standard will affect some foreign insurance companies that have head offices in countries where IFRS 17 is compulsory.

Notable Differences from U.S.

Employee Benefits

Japanese citizens under 75 years of age are eligible for National Health Insurance, as are all foreigners who have lived in Japan for more than three months. National Health Insurance is funded through employee, employer, and government contributions and covers most common medical expenses.

Property

Workers compensation insurance is compulsory and applies to all persons and types of businesses. It is controlled by the government with no insurance agent or broker involvement allowed. While not compulsory, employers liability and additional workers compensation insurance are also available. Another key difference is that agencies are the predominant distribution channel, with approximately 90.4% of premium share. The remaining premium share is split between direct business and brokers, respectively with 0.9% and 8.7% of premium share.

3 Tips for Doing Business in Japan

1. Exercise patience because the Japanese decision-making process takes time.

2. Understand Japanese business culture, which tends to be formal in the initial stages, with the intention of getting to know the other person, creating a feeling of harmony, and establishing consensus-making and respect for authority.

3. Respect is highly valued in business in Japan.