Walking, Not Running, Toward Healthcare Market Change

Employer groups, including unions and coalitions, are taking some control of healthcare costs in local markets.

Haven Healthcare hit the market with a splash in 2018.

Three major U.S. corporations—Amazon, Berkshire Hathaway and JPMorgan Chase & Co.—banded together with technology resources, more than one million employees, and some of the greatest minds in healthcare at the helm (surgeon and author Atul Gawande was named CEO). But the organization was disbanded in 2021 having made no major headway in its goals of reducing hospital and pharmacy costs and expanding access to primary care. On paper, Haven’s market power and technology should have been able to accomplish things individual employers did not have the wherewithal to manage. But the organizations were spread across too many locations. And the needs of varying employee populations may have been more akin to herding cats.

The unions and coalitions are focused on high-cost hospitals, increased transparency and state legislatures.

One such coalition created guidelines and payment models for advanced primary care and started implementing pilot programs in California.

Advanced primary care is patient-centered care that offers immediate access to providers when needed.

“Change has to be made regionally or locally,” says Chris Skisak, executive director of the Houston Business Coalition on Health. “They didn’t have enough people in each market

to make any kind of change. The Amazon warehouses in Houston don’t have the number of lives to make change happen here.”

Kerry Drake, president emeritus of employee benefits at Cadence Insurance, agrees. Drake helped form the Employer Coalition of Louisiana in 2022, which is employer-led and dedicated to collaboratively increasing the value of healthcare by lowering costs and improving safety, quality and consumer experience. “The whole point of these coalitions is can we collaborate together and maybe do something. … Healthcare is local; this has got to be driven locally.”

If there is no national answer and individual employers aren’t able to curb costs, then it may be those local forces—coalitions and unions—who have mass, technology and gumption to change markets. And they are focusing on high-cost hospitals, increased transparency and local legislative changes to move the needle.

“High-quality care at a good cost is the outlier more than the rule,” says Michael Thompson, president and CEO of the National Alliance of Healthcare Purchaser Coalitions. “We need to turn that around and take new approaches. We know what doesn’t work: contracting a network that includes everyone and expecting a price that is fair. The evidence is in. We need to start speaking with a common voice in each marketplace and advocating for market and policy reforms.”

Advanced Primary Care

Skisak has nothing against bundled pricing or narrow networks. But in general, he says, these options are not being promoted well enough by insurers. Not only are insurers often not set up to manage these things, he says, but they don’t necessarily have a big incentive to reduce costs.

This leaves employers to try to discern better ways, and few can do it alone, especially in highly concentrated markets like Houston. So his organization is beginning a program somewhat new to the industry known as advanced primary care.

The Purchasers Business Group on Health created guidelines and payment models for advanced primary care and started implementing pilot programs in California in 2021. In essence, advanced primary care is patient-centered care that offers immediate access to providers when needed. There is a care team that includes practitioners in areas like behavioral health, wellness and pharmacists. And care is coordinated, meaning they can move among their care team and specialists seamlessly.

Many employers are hesitant to try this kind of model, Skisak says, because you have to throw a lot of money at primary care with no guarantee of overall cost reduction. Primary care is a small chunk of the spending problem, but allowing these doctors to better manage people with chronic conditions can lead to fewer specialty referrals and unnecessary hospital visits, which is where the major outlay of healthcare funding goes.

Many factors go into making this kind of program work, but technology, care coordination and local bargaining are primary drivers in reducing costs. Skisak says the Houston Business Coalition on Health has cultivated relationships with local hospitals to negotiate “Medicare-like pricing” for their services.

“We are exchanging volume for cost,” he says. “And we’re talking 150% of Medicare prices. No employer should be paying more than that, with few exceptions.”

Skisak says the coalition will create a smart network where the hub is the primary care providers. These physicians will navigate patients through a narrow network of high-quality, low-cost providers when other care is required. Primary care providers will need a tool to help navigate this system and interface with specialists. Only a few third-party administrators can do this, and Skisak says it’s not the BUCAs (Blue Cross, United Healthcare, Cigna and Aetna).

A population health services organization will contract with the employers to run the program. Skisak says he hopes to have a small-scale product ready for purchase starting in 2024. The Houston Business Coalition on Health has begun working with primary care groups and finalizing the navigation platform. Skisak’s goal is for about 50% of the coalition’s members to get 20% of their employees to take advantage of the program. That would get the coalition started with about 50,000 covered lives. “We’re walking, not running, right now,” he says.

But Skisak hopes the program will pan out in saved dollars and improved quality within a couple years of its inception. He encourages employers to join local coalitions that may be working on this kind of initiative.

“You need covered lives and consolidation in markets,” he says. “Even though we have some of the largest employers in this city, not one has the kind of influence to make it happen on their own.”

Incremental Changes Provide Slow Progress

The state of Connecticut has one of the richest employee health benefits plans in the country. It’s a union-negotiated plan covering more than 216,000 lives with $1.6 billion in annual outlays for healthcare services. Like every other employer, plan administrators have repeatedly tried and failed to make significant spending cuts.

“Our goals have shifted after trying one-off programs,” says Josh Wojcik, the state’s assistant comptroller. “We may save a few million here and there, and it adds up…but we are trying to look at the longer term and how we, as a state plan, help to drive broader market changes.”

The state tried a tiered network in 2020. Based on cost efficiency and quality measures for certain episodes of care, facilities were labeled as centers of excellence or providers of distinction. The plan negotiated a fee for episodes of care—often similar to what was being paid for fee-for-service or a slight discount, Wojcik says. Members using these providers for procedures (including a breast biopsy, hip replacement, tonsillectomy and cataract surgery) received a monetary incentive ranging from $100 to $1,000.

From 2019 to 2022 the program saved about $6.9 million and just over one third of participants shifted to preferred providers. It was about a 2% change in the overall cost of these services, which totaled more than $301 million.

Wojcik admits the savings weren’t stunning, but he also says the program had some challenges that the state has remedied. Employees no longer have to register for an incentive and determine which provider to use. Now, when a patient uses the provider lookup tool, the tool automatically shows which providers take part and the incentive amount. Checks are automatically sent to anyone who uses the preferred providers.

The plan has also been working with providers on chronic disease management. The plan offered analytics and care teams to providers to identify gaps in care and where improvements could be made to remedy underlying costs. This program was administratively heavy, so a new model was rolled out in January with more money given to primary care doctors who will commit to controlling overall costs. This year the plan increased its monthly per-member fee to $18 from about $3.

“We are giving them a meaningful amount of money to do things like hire more staff, improve coordination with behavioral health groups, and engage on social determinants of health,” Wojcik says.

In the end, substantial cost savings may not be attainable for this program, Wojcik says. But the 6% growth in medical costs is no longer sustainable. Wojcik says he would like to keep growth at 2.9% annually. And the state has asked the primary care physicians participating in the program to meet, or beat, those numbers. “We want a reasonable trend that is consistent, we can work with and can budget for,” he says. “The market is built up to spend the amount of money it spends today, and making huge changes to make prices point down to something reasonable would be incredibly disruptive. The market itself can’t handle that.”

Drake agrees with the piecemeal approach as well as the challenge of keeping up with rising costs. “I’ve got to show [employers] that we’re trying to do something, whether individually within their own company, through multiple different solutions from pharmacy management solutions to medical management to musculoskeletal… But they just chip off a little piece…. Our cost of care from pharmacy to genetics and gene therapies, how much is that going to cost? Are we even going to get it to a level point? I doubt it.”

“We are exchanging volume for cost. And we’re talking 150% of Medicare prices. No employer should be paying more than that, with few exceptions.”

Chris Skisak, executive director, Houston Business Coalition on Health

Cost Data Transparency

When Gloria Sachdev became the president and CEO of the Employers’ Forum of Indiana in 2015, she met with business owners across the state to determine their pain points. The unanimous answer: healthcare costs.

Sachdev, a pharmacist by trade, sought data to understand why pricing was so high. She didn’t find a lot, so her organization contracted with the think tank RAND to produce some. The forum wanted to give RAND employer claims data to have the organization calculate how much the employers were paying in relation to what Medicare pays for those same services.

The forum’s first report was published in 2017 and showed that many hospitals in Indiana were charging employers rates that were upwards of 270% of Medicare costs. When Sachdev met with hospital leaders after the report inquiring about the rates, she says, they blamed low Medicare and Medicaid fees on the need to shift costs to employers, a common refrain in the industry.

Sachdev began talking to benefit consultants across the country and got data from 25 states to produce a second RAND report in 2019. To her surprise, the results showed that Indiana had the highest hospital prices of any of the 25 states.

“Everyone there lost their minds,” Sachdev says. “It wasn’t that we had more utilization; it was prices, and they were going up. Now we could compare prices of services in the same system in Michigan, and they were half what ours were.”

For Drake, RAND is the starting point of employer conversations. He notes that his company began to get involved with it roughly five years ago. “We have to have a starting point with the talking points,” he says, and RAND provided that. “Why are we paying three and a half percent or three times Medicare? What about this hospital down the street? They are only two and a half.”

There were two additional iterations of the pricing tool released, the last in 2022, which included 49 states and Washington, D.C., 4,100 hospitals and data from more than $78.8 billion in healthcare spend.

But providers began to argue that if you just look at costs you don’t consider quality. This data could be found by looking at sites like Quantros and the Centers for Medicare & Medicaid Services’ hospital ratings. But Sachdev wanted to make things as easy as possible for employers, so she helped develop Sage Transparency in 2022. It is updated quarterly and includes both pricing and quality data culled from a range of sources.

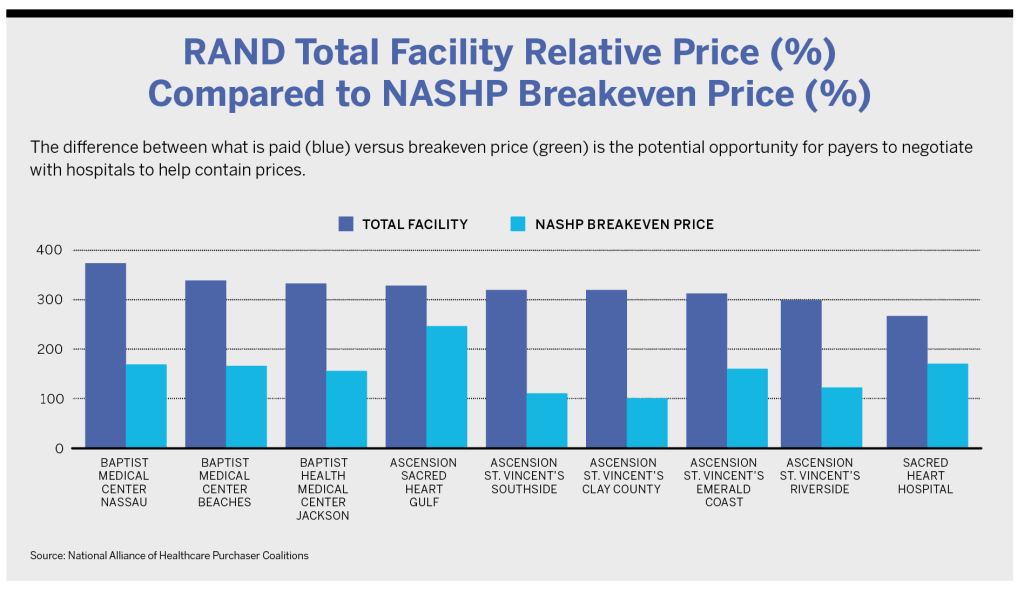

The pricing tool not only shows the average price hospitals charge for services, but it tabulates their break-even price on services. Sachdev describes this as the price commercial payers would need to pay to make a hospital whole for the losses the providers take on Medicare and Medicaid pricing. For example, Indiana University Hospital charges about 375% of Medicare pricing across the facility. According to Sage, its break-even is 106%. For a CT/MRI, the hospital charges 372% of Medicare rates; for emergency department services, 447%.

Sage is free and can be used by employers to get a better understanding of rates in their area. Employers can also pay to get a customized report. RAND can use an employer’s claims data to figure out what the employer is paying its specific hospitals as a percentage of Medicare rates.

Sachdev says employers should get their claims data and understand the pricing and quality scores of the providers their members use. Health insurance carriers may not want to provide that information. If they don’t, employers might have to amend their contracts.

“Employers need to assert that they have ownership of their claims data,” she says. “No one should tell them they can’t have access to it.” Sachdev asserts that denying access to claims data would be a violation of the Consolidated Appropriations Act.

Sachdev says she’s seen employers run the gamut of options, including reference-based pricing and narrow and tiered networks. But premiums and costs to employers keep rising, and medical debt soars.

“We have tried so many of these market solutions, but we’ve never had lots of information to hold folks executing these things accountable,” she says. “Like the promise of so many other things gone by, I hope this works.”

Fighting in the Statehouse

As important as transparency is to lowering prices, Sachdev says, it’s going to take more to change the way hospitals and other healthcare providers charge for services. Employers need to coalesce around policy changes and lobby at the statehouse.

“Even with greater transparency, hospitals aren’t shamed into changing, and prices will just keep going up,” she says. “There has been some market pressure and a little bit of change but not enough.” For this reason, her organization went to the legislature to fight for bans on surprise billing and gag clauses as well as greater efforts at price transparency. Laws pertaining to those issues were passed just before COVID-19 hit, but because so many hospitals took major income hits over the past three years, there was little appetite for more legislation. But interest has been renewed, and Sachdev says there are several bills that have been announced as priority legislation in Indiana this session.

“Legislators understand we need government support and policy change to create healthcare affordability,” she says. “The market can’t fix itself. It’s not a free market—the basic free market principles don’t apply to healthcare.”

Sachdev notes one bill that would offer tax credits for independent physicians and allow physicians employed by a hospital system to refer patients outside of the network for care. (The bill will likely be tweaked, Sachdev says, but she considers it a good starting point.) The bill would forbid the billing of facility fees and ban physician non-compete clauses. Most importantly, it would penalize providers that bill above 260% of Medicare rates for services. “We are trying to really focus on where the problems are and make changes there,” she says.

After wages, medical costs are typically an employer’s second-highest expense. Sachdev says it’s time that employers begin tracking bills going through their state legislatures and lobby for ones that will reduce the cost of care. There is no doubt, she says, that hospitals are there every year lobbying against those bills.

“We are giving them a meaningful amount of money to do things like hire more staff, improve coordination with behavioral health groups, and engage on social determinants of health.”

Josh Wojcik, assistant comptroller, state of Connecticut

Labor Union Takes a Leap

For most employers, cutting hospitals out of a plan is unconscionable. Employees tend to dislike these plans, and in some smaller markets, there would not be enough providers left to offer services.

But after years of trying to reduce costs through other means to no avail, that’s exactly what Local 26 did. In 2013, the Boston labor union representing about 10,000 workers in food service, hospitality, casinos and airports cut some high-priced hospitals out of its plan—major players in the city, including Massachusetts General Hospital, the Dana-Farber Cancer Institute and Boston Children’s Hospital.

In the early 2000s, the union health plan experienced what others across the country were seeing—costs that were outpacing what the union plan could afford. In 2004, a deductible was implemented requiring individuals to pay $500 and families $750. Then, in 2007, a contract was approved that contained kickers, which force companies in the union to pay into the system if the plan’s funds get low. Deductibles were eliminated, and every kicker was triggered. In 2010, money that was planned for a wage increase for employees was diverted to the fund to keep it from bankruptcy.

The plan was extremely generous and allowed people to see any doctor in the area. According to Carlos Aramayo, the union president, “It was the life of the Local.”

“But in figuring out how to keep that health plan, any other workplace issue, wage issue or retirement issue was subsumed underneath the question of how on earth we were going to keep paying for it,” he says. “It was the only conversation I heard from leaders and members, and it was, ‘How do we keep the healthcare?’”

In 2012, when the plan was set to renegotiate its contract, it sought input from insurers on how a new plan could be tailored to reduce costs. One insurer, Point32Health, responded with a narrow network option that the insurer said could cut costs by 15%.

About 30% of the union members did not want to change plans and cut out these major providers. This is partially due to demographics, Aramayo says. Union members are well paid, but they are generally in a lower-income group. A majority are immigrants, and Aramayo described others as “old-school white working class.”

“It’s not the most radical group of individuals,” he says.

For many members of Local 26, their health plan is a big differentiator between themselves and their communities. Healthcare was essentially free, and they saw family and friends struggling to pay high premiums for few benefits.

But the plan began looking at its spend and realized they were paying more for the same—and sometimes lower—quality services. For example, the plan compared knee surgery at Cambridge Health Alliance and Massachusetts General Hospital. The cost was three times more at Mass General, Aramayo says, and the outcomes weren’t as good. They found an MRI of the leg cost $636 at Cambridge, $1,249 at Mass General and $1,970 at Boston Children’s.

The Local underwent a campaign for about six months, much like they would for contract negotiations. Parts of the union were essentially shut down during this time, concentrating on campaigning and educational efforts and then getting people signed up, Aramayo says. When the new plan was put to a vote, it was supported by two thirds of the union members.

“For 98% of things, they can get better or equal outcomes, and members understood that because their friends were paying half of their paychecks for crap coverage,” Aramayo says. “In the end, sanity won.”

The results? An analysis by researchers at Harvard compared the Local 26 plan with claims data from a similar group without a narrow network and found a 20.6% decrease in healthcare prices. Because of the lower prices, Local 26 has been able to increase wages, including bumping room attendants’ hourly salaries to $27.20 from $17.20. It also increased the salary of doormen and bellmen by $8 an hour after noticing a dramatic drop in income because no one carries cash to tip anymore.

Marisa Fusco, director of client services for Point32Health, says they have educated brokers repeatedly over the years about the success of Local 26 and they offer similar plans to other clients. While some have shown interest, it’s the “rare client that will go all in,” Fusco says. If they offer tiered plans, some employees continue to opt for higher-priced plans with fuller networks negating any benefits of the narrow plan.

Fusco also notes that, while the plan sounds revolutionary, it was really looking “back to the future”—much like the HMO plans that used to be popular among many employers.

Ten years down the road, Aramayo says it was worth the effort, energy and stress it took to change plans. “If you are spending less money on insurance, you are spending money on something else,” he says, “and that really has made a very, very, very big difference in our members’ lives and the lives of their families.”

Where to Start

Thompson, of National Alliance of Healthcare Purchaser Coalitions, says there has never been more need than right now for employers to work to reduce healthcare costs. “Costs are too high already,” he says, “and in the absence of employers’ leadership, we will continue to see this spiral. Employees and their families can’t expect to pick up the balance, which is what’s been done for a decade. We’ve hit a wall. There’s no one left to pick up the bill.”

Thompson’s organization has put together a playbook that can help employers understand hospital transparency and how to use it to negotiate “fair prices” from providers. Some options it discusses are advanced primary care, reference-based pricing, creating tiered provider networks, and negotiating lower rates for episodes of care.

“Why should employers be subject to what we know isn’t fair,” Thompson says. “Fair prices are 140% to 200% of Medicare, and we see health systems charging 300% to 500%.”

Having competition in a market, coupled with price transparency, may increasingly help employers negotiate lower prices, even if it’s only for specific kinds of care. Transparency, Thompson says, should enable employers to take a more active stance and have more leverage over hospitals and other providers.

“As we’ve opened up the cover, we aren’t all that happy with what the system looks like,” he says. “Making change will require leadership to course-correct the system. The fact is that successes have been few and far between. There are some individual employers that have done good stuff, and we want to follow in their footsteps.”

It may take a village to shift a local healthcare system, but Sachdev says individual employers should start by understanding their own house.

Her first recommendation is to look at claims data and stop listening to anyone who tells you they are lowering costs or improving care unless there is proof. “You can’t just say you have a PBM and TPA and that’s their job to do this,” she says. “Hold every single person in your supply chain accountable for what they say they are doing.”

For example, if you have a program that is supposed to be working with your population with diabetes, get outcome measures. See if hemoglobin and A1c are improving. If someone is pitching a program like this, get a performance guarantee that members’ numbers will get better.

Next, negotiate rates based on Medicare to make things simple, she says. Try to get rates that are 180% of Medicare when possible. Tools like Sage make this easier than ever. For instance, if you go to Sage and see the market rate is about 300% for a provider and they offer 250% in negotiations, that may sound good. But Sage also may show that their break-even rate is 120%.

“Then, an employer can say, ‘We appreciate you offering 250%, but I think we can do better,’” she says. “Hospitals don’t want to lose business, and I have seen some really interested in these percentage of Medicare contracts, so much so that some hospitals are advertising these rates.”

The Health Resources and Services Administration has a free download that allows employers to reprice their claims based on Medicare fees. Using that will let an employer know what it is currently paying and enable it to compare that to the Sage’s break-even number for each provider.

“Everyone needs to start looking at data, and then opportunities will be evident,” Sachdev says. “You will see why you are paying so much, and your negotiations with providers won’t be blind negotiations anymore.”

Drake channels what he hears from frustrated employers everywhere and explains what it means to take on this work. “I’m the payer, but I’m the only one that doesn’t have a seat at the table. Everybody else is figuring out the prices they’re going to charge me…and I don’t have a seat at the table. What can I do differently? And, you know, as a broker consultant, we’ve got to give them hope.”