Same Treatments, Dramatically Different Costs

Q&A with Allison Oakes, Chief Research Officer, Trilliant Health

Oakes discusses a new analysis of the cost of healthcare procedures ranging from colonoscopies to coronary bypasses in both hospital and non-hospital settings.

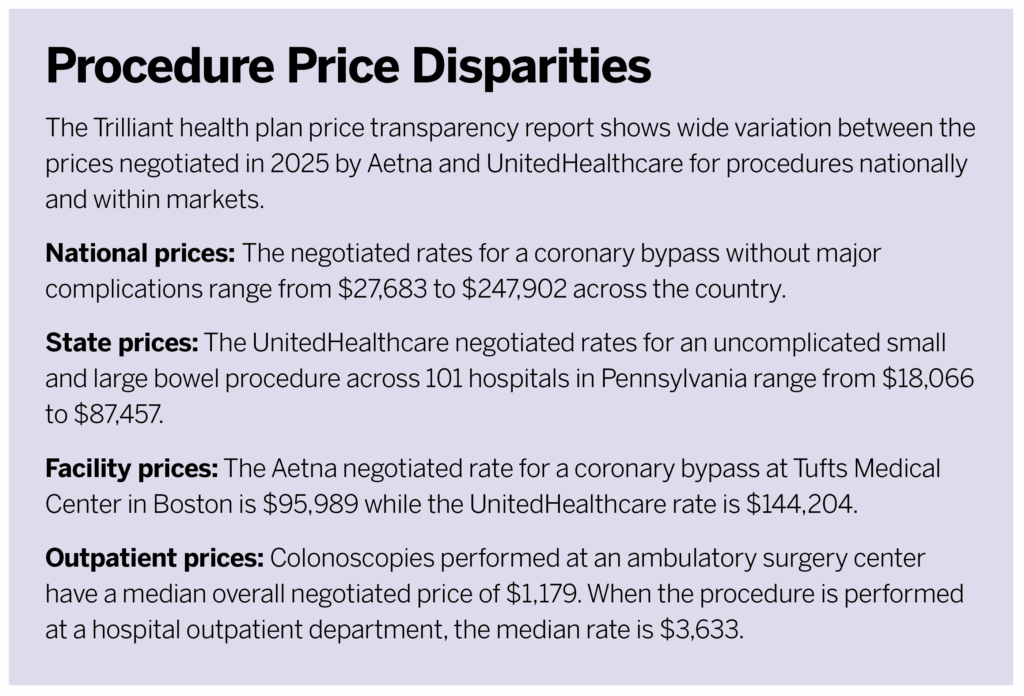

The report, from healthcare analytics and research firm Trilliant Health, finds that prices negotiated by Aetna and UnitedHealthcare for the same treatment can vary by thousands, tens of thousands, or even hundreds of thousands of dollars based on facility or location around the country.

Q

What makes this new report important?

A

In July of 2022, insurers had to make the prices they negotiate for healthcare services publicly available [under the federal Transparency in Coverage final rule]. The data we used in this report is from 2025, so it allows for real-time analysis of healthcare costs. In the healthcare space, data gets old relatively quickly. We think it’s really exciting that these files have to be published and updated monthly so you can look at current negotiated rates. The second important thing is that the health plan price transparency files include information on negotiated rates for both hospital and non-hospital care. Traditionally, a lot of these analyses have only focused on the hospital side of the equation, but non-hospital care accounts for the majority of utilization and spending. And lastly, but importantly, the health plan price transparency files are national so they’re representative and generalizable, but they also allow you to analyze things down to the level of an individual provider. That allows us to look at the price a specific provider is negotiating for a specific procedure.

Q

How did you choose the procedures and data to evaluate?

A

We’re very much scratching the tip of the iceberg, if you will. In order to get this into a manageable report, we chose to focus on just a handful of DRG codes [used by doctors to indicate what treatment they are performing]. We picked 11 different procedure codes. Six are focused on the inpatient setting, and five are focused on the outpatient setting. We wanted to make sure that we were picking codes that were relevant to the commercially insured population. But we also wanted to pick codes that allow patients to shop within healthcare. So, things that people weren’t necessarily being put in an ambulance for—where they don’t have any sort of choice in where they’re getting care.

Q

This data shows dramatically different negotiated prices even for the same procedure at the same facility.

A

That’s really the most consistent thing we see in health plan transparency data—the extent of the variation. No matter how we cut it, we know this variation in negotiated rates exists, and it’s really unwarranted. Just looking at a subset of 10 well-known hospitals, we looked at the relationship between their negotiated rates and measures of quality. We didn’t see a strong relationship between those two things. So, unlike every other industry, where you can expect to get what you pay for, healthcare doesn’t work that way. We think that needs to be addressed. Another thing that’s quite startling is the extent to which two different patients can go to the exact same hospital and, in this case, one has Aetna and another UnitedHealthcare, that same procedure could cost very different amounts of money. Largely because of proprietary pricing, healthcare has been this industry that’s been able to defy many rules of economics for many decades. And now that this pricing information is available, payers and providers need to start competing on price. We hope that by getting them to do that some of this unwarranted variation can be checked.

That’s really the most consistent thing we see in health plan transparency data—the extent of the variation.

Allison Oakes, Chief Research Officer, Trilliant Health

Q

Did you find any procedures or facilities that tended to be less expensive?

A

We did typically see, overall, that getting procedures performed at an ambulatory surgical center was less expensive than a hospital outpatient department.

Q

You compared prices for Aetna and UnitedHealthcare. Why just these two insurers?

A

This data is really difficult to download, ingest, and work with. For this particular report, we were looking at data for Aetna and United, two of the largest national payers in the country. That entails working with more than 20 terabytes of data. Once you get your hands on it, there’s still a lot of cleaning that needs to be done to make the data reliable and accurate. It is a large data-science undertaking. But when you get it processed and adjusted correctly, you end up with something that’s very intuitive. You can see what a particular facility charges for one procedure. After a lot of time and energy, we end up with a data set that is very workable and usable for people.

Q

Could employers perform this data breakdown on their own?

A

Unfortunately, to work with any subset of the data, you do have to get your hands on the whole thing. But companies like Trilliant are able to split things out into much more easily manageable pieces of data. Whether that’s a particular state or even a particular market, once we’ve cleaned the data, we’re able to subset it, and that’s something that we’re happy to partner with employers on. We think it’s really important that they’re aware of this information and are able to start using it.

Q

How can employers and brokers use this new report even though the data isn’t specific to their negotiated prices?

A

I don’t think a stakeholder like an employer necessarily needs access to every single data point in order to start asking the right questions. They can read the report and use it as a foundational educational piece to understand just how much variation we’re seeing across the country, to see the wasteful spending that’s likely going on within the U.S. healthcare system. By understanding that piece of the puzzle, employers can start asking benefits brokers and other folks across the health economy to start sharing more information with them about the sort of value that they’re providing to their employees.

Employers can begin to understand within their markets who the high- or low-value providers are, generally speaking. In most markets, we tend to see there’s just a handful of high outliers [facilities that charge much more for services than others in their market]. And there actually could be a strategy where, so long as your employees avoid a few problematic, very high-priced, average-quality providers, that could be one way to improve care value.

We also think that, by arming employers with the knowledge that rates vary in this way, they can begin asking tough questions to the folks that help them administer their benefits. They can start holding them accountable by ensuring they’re steering their employees towards the highest-value providers in their market. Employers can either start directly working with the data themselves or start asking the people who are helping them buy benefits if they are bringing high-value providers to the table in the networks they are setting up.

We also think that, by arming employers with the knowledge that rates vary in this way, they can begin asking tough questions to the folks that help them administer their benefits. They can start holding them accountable by ensuring they’re steering their employees towards the highest-value providers in their market.

Allison Oakes, Chief Research Officer, Trilliant Health

Q

Why are employers such an important part of the healthcare economy?

A

They are a huge stakeholder. Healthcare spending in [the U.S.] system was about $4.9 trillion in 2023, and employers were responsible for 30% of all that spending. That’s more than $1.4 trillion.

Employer-sponsored health insurance is considered a welfare plan under ERISA, so employers have the fiduciary duty to be administering benefits solely in the interest of participants and beneficiaries. An important piece to all of this is that, before the 2020 Transparency in Coverage final rule, information on negotiated rates was really hard to get your hands on. This was because of federal antitrust laws and different clauses included in these commercial health plan contracts. Though this information is hard to access it is technically publicly available. It implicates the fiduciary duty of those employers, and they need to be using this information to help make informed business decisions for their employees.

Q

What are the main takeaways from the report?

A

I would say the theme is that a market with proprietary prices is doomed to fail. We don’t see a relationship between price and quality. And when we see huge variations in negotiated rates across the country, while concerning and problematic and shocking in some ways, I also think it’s not surprising. We do really hope that this data can shift the pendulum where all these different players will start competing on things like price now that they know that people have access to this sort of information. They need to make sure they’re actually providing value to the healthcare consumer, which we think is employers—because of the way they administer benefits—but also, most importantly, to patients.

I do think during the last five to 10 years, a lot of the price transparency efforts have put the onus on patients or employees to be shopping for their healthcare services with a handful of different tools. I don’t think we’ve seen that be hugely successful. And I think that the extent of the problem that we reveal in this report mandates much broader systemic change, rather than expecting employees to shop their way out of this problem. If just those top 10% of the most expensive providers across the country reduce their rates to the market median, that would have a huge impact on overall healthcare spending.