Medicare Advantage Sicker Than Expected

Medicare Advantage was booming a few years ago, but higher than expected claim severity and lower government payouts are driving carriers out of markets, leaving insureds to scramble.

After years of steady growth, Medicare Advantage has hit a snag.

During the 2026 Medicare annual enrollment period last fall, nearly 3 million Medicare Advantage beneficiaries were forced to find new coverage after several of the largest carriers closed their plans or exited markets. It represented the highest forced disenrollment in the program’s existence, says Susan Reilly, vice president of communications at the Better Medicare Alliance advocacy organization.

Leading health insurance carriers stopped providing Medicare Advantage plans in more than 800 U.S. counties from 2025 to 2026, far more than the number of counties they entered. Nearly 3 million beneficiaries had to find new coverage.

Brokers are also feeling the pain as insurers reduce or eliminate their commissions on Medicare Advantage plans in order to slow enrollments.

The carrier actions were driven by three primary concerns, sources say: higher-than-expected claims, inadequate compensation from the federal government, and legislative updates to the Part D prescription drug program.

Together, the top carriers (UnitedHealthcare, Humana, Elevance, CVS Health, and Centene) exited Medicare Advantage in over 850 counties across the nation from 2025 to 2026, according to analysis by KFF. They entered fewer than 150.

The carrier retrenchment on Medicare Advantage, the private alternative to government-provided “traditional” Medicare that serves roughly 35 million seniors and people with disabilities, reflected their concerns with higher-than-expected claims, insufficient federal compensation, and legislative changes to the Part D prescription drug program that reduced claims limits and thereby increased carrier exposure.

Many of the largest carriers also curtailed or suspended Medicare commissions to brokers immediately prior to or during the 2026 enrollment period. That included Humana, UnitedHealthcare, Anthem, and Centene, along with SummaCare and other regional insurers, STAT reported last November. Six brokers interviewed for this story said that many carriers cut Medicare Advantage availability and commissions for brokers throughout much of the country in the second half of 2025. Some had done the same during the 2025 Medicare enrollment, they said.

The 2026 Medicare enrollment period opened with carriers paying us, and then two weeks later, we found out from them that, ‘Hey, our plan’s too [generous and attractive to beneficiaries] in our eyes, and we’re going to pull commissions to slow enrollments,’” says Matthew Miklos, vice president of individual Medicare solutions at UROne Benefits, a Richfield, Ohio-based health insurance brokerage acquired in 2019 by Oswald Companies. That hurts both brokers and their insured clients, he adds.

“What we saw at the end of 2025 during the open enrollment was a reduction in service from these Medicare Advantage plans, where many [carriers] were removing PPOs and just keeping their HMOs, where they can contain costs more and also reduce their networks of higher-paid providers, or leave the markets totally,” adds Elizabeth Gavino, founder, president, and owner of Lewin & Gavino, a national insurance consulting firm.

All eyes will be on 2027 open enrollment, which begins Oct. 15, to see exactly where carriers’ Medicare Advantage offerings head next. Brokers say they and their colleagues must prepare again for uncertainty about which plans will be available in which markets and what they will offer. Many say it is almost certain that the challenges will largely not be resolved by then, likely leading to additional thinning of benefits, increased plan costs, and further reductions and eliminations of commissions.

The Medicare Advantage Value Proposition

Medicare is the federal health insurance program that serves Americans 65 and older and a younger subset with certain medical conditions and disabilities. Traditional Medicare is composed of four parts: Part A covers inpatient hospital care; Part B covers outpatient services ranging from home health to some surgeries and imaging; Part C is private Medicare Advantage; and Part D is prescription drug plan coverage, also offered by private carriers.

Dating to 1997, Medicare Advantage provides private senior healthcare plans under which insurers, instead of the federal government, offer coverage through an HMO, PPO, or similar platform. To join Medicare Advantage, one must still be enrolled in both Medicare Parts A and B, pay Part B premiums, and live in the plan’s service area. Brokers and agents are involved as captive agents representing a single Medicare Advantage and/or Part D carrier, independent agents representing multiple carriers, or brokers helping beneficiaries select among many plans. Beneficiaries can also buy Medicare Advantage directly from carriers.

Many Medicare Advantage plans offer Parts A, B, and D benefits together in one plan. Unlike traditional Medicare, under Parts A and B, Medicare Advantage enrollees must use a local network of providers. A participant must pay a deductible, copays, and co-insurance up to the plan’s out-of-pocket maximum, notes Danielle Kunkle Roberts, a founding partner at Fort Worth, Texas-based Medicare-oriented brokerage Boomer Benefits. Plan offerings often vary significantly by state or even county, and prior authorization is needed for some treatments or services.

However, Medicare Advantage reduces out-of-pocket costs compared to traditional Medicare and pays for wellness extras such as eyeglasses, hearing aids, and gym memberships.

Growth, then Setbacks

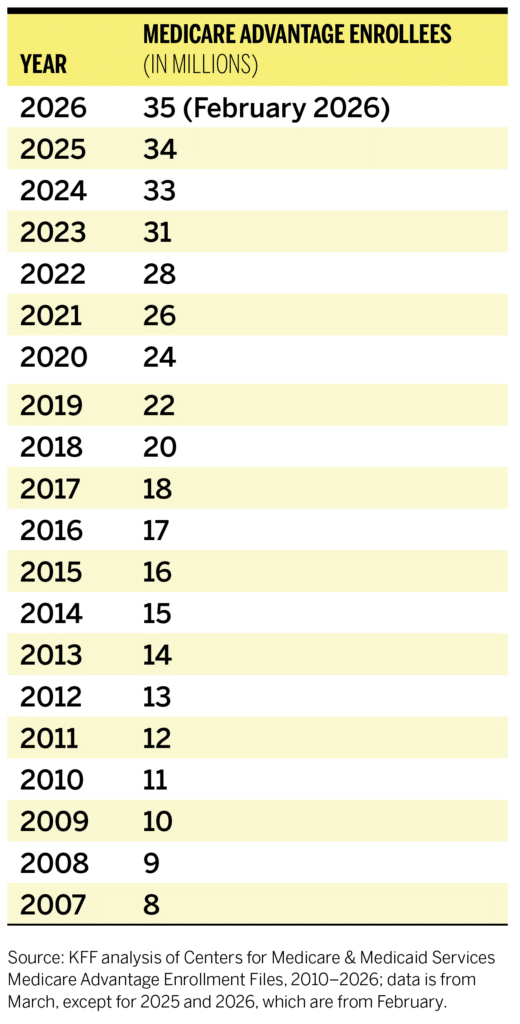

Over the decades, Medicare Advantage steadily claimed market share from traditional Medicare to become the nation’s leading retirement health plan delivery vehicle, rising from 8 million enrollees in 2007 to more than 35 million in 2026.

For the federal government, Medicare Advantage offered a path away from the expensive defined benefit of traditional Medicare. Carriers and brokers saw an opportunity to profit in a new line of business previously occupied (but still paid for) by the U.S. government.

A total of 3,373 plans were available for enrollment for 2026 nationwide, down 9% from the prior year, KFF reported. Annual enrollment growth rates sat between 7% and 10% early this decade but slowed to 3.6% for 2025 and 2.5% for 2026, according to a February 2026 report from consulting firm HealthScape Advisors.

There are several causes for this slowing growth. First, patient care costs have risen more than anticipated, challenging the program’s profitability for carriers. Second, as of this year, the federal government has pushed to contain healthcare spending by slowing growth of its Medicare Advantage payments to carriers and attempting to detect and resolve inflated billing or fraud. Finally, carriers have been forced to adjust to a federal rule change that changed the economics for one component of many Medicare Advantage policies: Medicare Part D prescription drug coverage.

“Medicare Advantage used to be a major profit driver for almost every payer—it was the primary line of business they were focused on,” says Brooks Deibele, executive vice president and employee benefits practice leader at brokerage Holmes Murphy. “But at this point in time the utilization is up, and the focus for payers has shifted from being all about growth to, now, all about margins and doing whatever they can to get back to a position where they’re comfortable with their financial standing.”

Sicker Patients, Higher Costs

Medicare Advantage’s troubles reflect the healthcare cost crisis nationwide, notes Megan Mason, formerly director of government affairs and public policy at the Steptoe law firm, who recently joined the Maryland Insurance Administration as an associate commissioner.

Per-capita healthcare expenditures rose from $14,580 in 2024 to $15,474 in 2025, a 7.2% increase, according to a Health Affairs Publishing study. Between 2022 and 2023, overall U.S. health spending rose 7.5%; it was projected to rise another 4.2% in 2025, according to an April 2025 Peterson-KFF Health Care Tracker analysis.

The tsunami of baby boomers passing out of employer plans and into Medicare and Medicare Advantage, an unprecedented demographic event, proved to be less healthy than anticipated, with high rates of chronic diseases such as diabetes and Alzheimer’s. And there is no healthier segment of the Medicare Advantage market to balance out older users at greater risk for health issues. Gavino says carriers told her that increased costs also in part reflected a surge in beneficiary healthcare procedures that were deferred during COVID-19 but later taken in recent years.

Design Flaws

Some have also faulted structural shortcomings in Medicare Advantage’s design that result in overpayments by the government relative to the healthcare services being delivered.

Carriers receive a fixed fee per beneficiary per month based upon the number of beneficiaries in Medicare Advantage, which is adjusted to reflect the cost of care for each individual, notes an analysis by the Better Medicare Alliance.

A March 2026 report from Congress’s Joint Economic Committee concluded that all Medicare Part B premiums, for traditional and Medicare Advantage alike, are higher because Medicare Advantage is overpaid, with beneficiaries on average costing about 120% the amount of a user of the traditional Medicare program. Two aspects of Medicare Advantage’s structure, coding intensity and favorable selection, are at the root of the overpayment, according to a report from the Medicare Payment Advisory Commission (MedPAC), a nonpartisan, independent legislative branch agency that provides Congress with analysis and policy advice on the program.

Coding intensity accounts for differing financial incentives to document medical conditions between Medicare Advantage and traditional Medicare. Medicare Advantage plans often use aggressive, automated, or in-home coding practices to document more diagnoses than the traditional program. This “upcoding” inflates beneficiary risk scores, leading to an estimated $21 billion to $38 billion annually in excessive, non-care-related payments this decade, the MedPAC report found.

Favorable selection, meanwhile, is the trend of beneficiaries with lower-than-expected medical expenditures preferring to enroll in a Medicare Advantage plan over fee-for-service Medicare. That leads to overpayments to Medicare Advantage carriers beyond what their beneficiaries’ health needs warrant, given risk scores predicting beneficiaries’ costs in advance are used to set Medicare Advantage payments. According to MedPAC, favorable selection led to larger overpayments than upcoding: between $31 billion and $57 billion annually over the course of this decade. (This, however, does not change the fact that the overall baby boomer-focused Medicare Advantage population is less healthy than had been anticipated.)

Other research suggests that Medicare Advantage plan design and practices may contribute to hospital discharge delays, adding to costs and care utilization issues. A 2025 Journal of the American Medical Association study found, for example, that in a cohort study involving more than 89 million hospitalizations from 2017 to the third quarter of 2023, Medicare Advantage beneficiaries experienced disproportionately greater increases in extended hospital stays, especially among those discharged to skilled nursing facilities, compared to traditional Medicare beneficiaries. According to the study, “Hospitals have reported growing difficulty in discharging patients in a timely manner, often citing bottlenecks in postacute care.” The study notes that while administrative and network challenges with Medicare Advantage may contribute to these delays, national evidence is lacking.

“Across the industry, the core challenge is that medical cost trend and utilization pressures including inpatient/outpatient costs and pharmacy cost trends continue to escalate, while multiple programmatic and technical policy changes (including risk adjustment-related changes) can also affect plan economics,” says Joshua Meeks, vice president for Medicare individual business at Blue Cross Blue Shield of Michigan. “Many organizations have experienced cost increases that outpace what would be considered ‘normal’ in prior years, which is why you’ve seen broad benefit, pricing, and portfolio adjustments across carriers.”

The federal government has sought recently, with some success, to place downward pressure on funding for Medicare Advantage. In January, the Centers for Medicare & Medicaid Services (CMS) announced a preliminary 2027 Medicare Advantage and Part D federal government payment rate increase of only 0.09%, down from 5.06% in 2026, 3.70% in 2025, and 3.32% in 2024, despite surging healthcare costs. In early April, responding to heavy lobbying by payers and beneficiary advocacy associations, CMS announced a final net average increase of 2.48%, or over $13 billion, in additional payments to be paid to Medicare Advantage plans in 2027.

CMS is also phasing in a new Medicare Advantage risk adjustment system—the agency uses risk scores to estimate enrollee healthcare costs and pay more to carriers for patients are likely to be more expensive—designed to reducing coding intensity that has led to program cost growth. However, the existing 2024 risk adjustment model is expected to remain in place for 2027.

The Trump administration is also taking enforcement actions to rein in questionable carrier cost submissions, including against carriers alleged to have submitted inaccurate diagnosis codes to inflate CMS payments. In January, for example, the Department of Justice announced that affiliates of healthcare consortium Kaiser Permanente had agreed to pay $556 million to resolve allegations that they violated the False Claims Act by submitting invalid diagnosis codes for their Medicare Advantage Plan enrollees. In March, it announced a $117.7 million settlement in a similar case involving Aetna.

Additionally, the Inflation Reduction Act of 2022 affected Part D coverage, which is a part of many Medicare Advantage programs, Boomer Benefits’ Roberts says. Essentially, that legislation reduced the cap on beneficiary payments from $8,000 to $2,000, greatly curtailing a funding source for carriers, leading them to increase premiums. In response, the Biden administration instituted a subsidy to buy down the premiums. But that subsidy ended on Dec. 31, 2025, as CMS, now under the Trump administration, said that it would return Part D premiums to operating under regular market conditions, she notes.

Carriers Respond

Medicare Advantage is a highly concentrated industry. In 2025, the top five carriers held a roughly 70% market share of all Medicare Advantage subscribers, according to KFF figures. Even within that small group, UnitedHealth GroUp (parent of UnitedHealthcare), Humana, and CVS Health dominate, with 29%, 17%, and 12% market share, respectively. In all, 164 organizations offered Medicare Advantage plans in 2025, according to the 2026 MedPAC report. But that is down from 175 carriers in 2024 and 183 in 2023, MedPAC reports to Congress show.

The recent adverse cost and compensation trends led to drastic actions by some carriers. For instance, UCare, a Minnesota HMO that for decades primarily served low-income Medicaid and Medicare Advantage policyholders, went from having more than $1 billion in reserves in 2023 to insolvency and is scheduled to close this year.

On Oct. 1, 2025, just before the opening of annual enrollment for 2026, UnitedHealthcare announced that it would eliminate Medicare Advantage plans in 109 counties around the country, affecting about 600,000 policyholders, in order to offset increasing costs.

“UnitedHealthcare made strategic adjustments to its Medicare Advantage offerings for 2026 to ensure long-term affordability and stability for the millions of members who rely on us,” a UnitedHealthcare spokesperson says. “Some of these changes included plan closures and market exits, and impacted individuals received a CMS-required notice last October, with clear guidance on options and next steps. Many Medicare Advantage plans across the industry experienced benefit changes in 2026 due to funding constraints and rising health care costs. For UnitedHealthcare, any changes to benefits are always guided by a commitment to preserving sustainable access, affordability, and quality care, and prioritizing core benefits that matter most to consumers—and are foundational to MA’s value beyond original Medicare.”

Many other carriers also withdrew from markets or curtailed Medicare Advantage offerings. The KFF analysis found that, in addition to UnitedHealthcare, Humana, Elevance Health (formerly named Anthem and the parent company of many Blue Cross Blue Shield carriers), and CVS Health all exited Medicare Advantage in at least 100 more counties than they entered in 2026. Another leading carrier, Centene, exited 104 and entered 63. Several large carriers declined to comment for this article.

An analysis by Oliver Wyman, a Marsh management consulting firm, found that nearly 70% of individuals likely to be affected by plan closures in 2025 were covered by Humana, CVS Health, or UnitedHealth Group.

Medicare Advantage used to be a major profit driver for almost every payer.…But at this point in time the utilization is up, and the focus for payers has shifted from being all about growth to, now, all about margins.

Brooks Deibele, executive vice president and employee benefits practice leader, Holmes Murphy

In 2025 earnings calls, UnitedHealthcare executives said unexpected costs and slowing government funding in programs that serve Medicare-eligible populations, including Medicare Advantage, were sufficient to drag down the healthcare giant’s bottom line.

“The primary driver of the UnitedHealthcare earnings shortfall for 2025 is that our pricing assumptions were well short of actual medical costs,” CEO Tim Noel said in July 2025 during a second-quarter earnings call with investors. “Our current view for 2025 reflects $6.5 billion more in medical costs than we anticipated in our initial outlook. A little over half, or $3.6 billion, of this is in our broad-based Medicare portfolio.”

In an April investor call announcing first-quarter 2026 earnings, Noel said Medicare Advantage costs have continued to grow from 2025. “We continue to see the utilization patterns continuing at the high elevated levels that we experienced in 2025,” Noel noted. “We were talking about a 7%–8% [cost] trend in Medicare Advantage [in 2025], with the pricing assumption of around 10% into 2026.”

Notably, Humana, despite withdrawals from many county markets, has increased its Medicare Advantage enrollment. Total Humana Medicare Advantage members, group and individual, grew from nearly 5.8 million in first-quarter 2025 to over 7.1 million in the same period of 2026, according to Humana’s report on first-quarter 2026 financial results. In a February earnings call with stock analysts, the carrier sought to address concerns about cost exposure posed by that growth. “When we look at full-year 2026, we do anticipate individual MA membership growth of approximately 25%,” said CEO James Rechtin. “And I will continue to remind everybody that as we collect new information and as the market evolves, we are continuing to manage our go-to-market strategy dynamically. We have levers to pull if and when needed, and we are constantly evaluating that.” In an April earnings call, Rechtin made statements that analysts interpreted as suggesting Humana will trim benefits offered in its Medicare Advantage plan bids submitted to CMS for the 2027 plan year.

It makes sense for carriers to consider Medicare Advantage exits and entrances at the county level, industry observers say.

“There are real significant differences in the healthcare markets across the nation,” says Gretchen Jacobson, vice president of Medicare at the Commonwealth Fund. “Part of what drives a lot of business decisions is really what’s going on within a specific market. You could have situations where some markets are highly profitable and other markets are much less profitable, and it also comes down to which patients are choosing to enroll in Medicare Advantage plans in the market and which are not, in addition to a lot of other strategies that might be specific to a firm.”

Blue Cross Blue Shield of Michigan, for example, unlike some other Blue Cross Blue Shield companies, has not stopped offering Medicare Advantage in any counties this year and continues to offer stand-alone Medicare Part D prescription drugs plans in the state, Meeks says.

Carriers have also reduced some supplemental services provided to Medicare Advantage beneficiaries in recent years, a December 2025 KFF analysis showed. “While nearly all individual Medicare Advantage plans (98% or more) are offering vision, dental and hearing benefits, as they have in previous years, the share offering certain other supplemental benefits has declined, such as allowances for over-the-counter items such as toothpaste, vitamins, and cough syrup (66% in 2026 vs. 73% in 2025), meal benefit (57% in 2026 vs. 65% in 2025), remote access technologies (48% in 2026 vs. 53% in 2025), and transportation (24% in 2026 vs. 30% in 2025),” the organization said. The 2025 numbers were also down from 2024.

Other benefits, while still offered, have been reduced in scope, such as dental care. Medicare Advantage national availability of comprehensive dental as of 2026 had dropped by more than 5% from its peak at around 91% two years earlier, actuarial and consulting firm Milliman stated in a March 2026 report. The principal culprit was lower offerings through combination benefit packages.

Fewer Medicare Advantage plans are also offered on a $0 premium basis (no additional premium beyond the Medicare Part B premium, which is still required), an Oliver Wyman analysis found. The count of $0 PPO products fell from 1,145 in 2025 to 991 this year as carriers shuttered plans or added premiums in the face of profitability challenges, the report says. It noted that more than 77% of Medicare Advantage and Medicare Advantage Part D users in 2025 had $0 premium plans.

An alternative to Medicare Advantage is the private Medicare Supplement Insurance (Medigap) plans that offer additional types of coverage fixed by the federal government, but often at a hefty cost and, in some circumstances, requiring prior underwriting.

However, Medigap plans also face rising costs, keeping Medicare Advantage a relatively more attractive option for many, says Chris Mihin, vice president and managing principal at brokerage Hub Heartland. “We are seeing a 20% to 25% average cost increase on Medicare Supplements, and it doesn’t matter what carrier, what state you’re in. It’s getting cost prohibitive to stay on them due to the large increases and many beneficiaries are looking to Medicare Advantage for relief.”

Carriers Bucking the Trends

Some smaller health insurers also appear to be increasing their Medicare Advantage enrollments.

Devoted Health, which describes itself as an “all-in-one healthcare company for Medicare beneficiaries,” has expanded from 14 states in 2024 to 29 states in 2026. In January, it announced that it has grown to serve over 466,000 members, a year-over-year increase of 121%. The percentage comprised specifically of Medicare Advantage was not immediately known, as the carrier declined to be interviewed.

Another carrier, not-for-profit SCAN Health Plan, offers Medicare Advantage in California, Arizona, Nevada, New Mexico, Texas, and Washington. During the 2026 Medicare enrollment, it added 127,000 members—a 40.6% year-over-year increase that brought it to about 440,000 nationwide. Annual revenue in 2026 is expected to exceed $8 billion, the company reported.

SCAN’s success was driven by strong provider and broker relationships, along with disciplined network expansion, CEO Sachin Jain said in a statement. Jain added that approximately 25% of SCAN’s total membership growth stemmed from new provider partnerships.

Targeted products, including population-specific plans, have played a critical role in driving enrollment, according to SCAN. These plans serve populations including LGBTQ+ seniors, older women, and Asian seniors by connecting them to culturally aligned providers, specialists, and pharmacies. During the latest annual enrollment period, these population-specific plans all grew by well over 100%.

Brokers are also a part of the SCAN strategy. In April, the carrier launched a Brokers as Health Navigators program designed to equip brokers with training and tools to serve as advisors who actively support members in achieving their healthcare goals across SCAN’s Arizona, Nevada, New Mexico, Texas, and Washington markets.

Through late April, 200 brokers were participating in the program across the five states, says SCAN Health Chief Growth Officer Michael Blea. Beyond commissions, they receive payments based on supporting health-related activities with clients, such as $15 for reaching out to a client within 45 days of enrollment with a welcome call, and $20 for scheduling clients for flu vaccinations that are then completed, with other milestone payments planned.

“Our members are four times more likely to stay with the plan if they connect with SCAN within the first 30 to 60 days of their enrollment, and the idea is to really scale out these [and other broker-related] activities—brokers are in the clients’ homes, so they can see the living conditions and situations,” Blea says. “Our goal here is to give the brokers tools, technology, resources, and support to be able to have meaningful conversations with their clients that drive retention, drive better member experience, and ultimately improve healthcare outcomes.”

Decisions for Brokers and Agents

The roles of brokers and agents in Medicare Advantage range from advising employers on benefits options for their staff to providing specialists to help guide older workers through their coverage options. In some cases, they serve plan beneficiaries directly in a manner akin to retail brokers and agents.

The national maximum initial Medicare Advantage broker commission is set at $694 per member, though some states and the District of Columbia go higher. But there is no floor. Every insurance source interviewed said agents and brokers are already withdrawing from Medicare Advantage, with others to follow if commissions continue to be cut, though there are no hard statistics on broker withdrawals.

“There’s a growing truth to the concerns that insurance carriers are making sure they meet their margins by reducing compensation to brokers,” says health insurance entrepreneur Jeff Smedsrud. “And it requires so much continuous education to stay up to speed. The result is many brokers are saying, ‘It’s not worth my time to continue to educate myself about this,’ and that leads to them saying to their customers, ‘Hey, I don’t handle this anymore.’ And so the consumer calls some of these call centers, and they get enrolled in plans that they don’t really understand and are subjected to a lot of pressure tactics.”

Some entities have pushed back against the commission reductions.

In October 2025, the Idaho Department of Insurance issued a cease and desist order directing UnitedHealthcare of the Rockies and Care Improvement Plus South-Central Insurance not to, among other things, withhold agent commissions with the intent of manipulating the insurance market and depriving consumers of products. However, in December, a federal court in Idaho issued a temporary restraining order against the state, finding that UnitedHealthcare of the Rockies was likely to ultimately prevail on its claims that federal law preempts state efforts to regulate Medicare Advantage plans.

Also last year, the National Association of Benefits and Insurance Professionals issued a statement objecting to UnitedHealthcare’s decision to eliminate agent commissions across more than 100 Medicare Advantage plans in over 20 states. “This move limits access to trusted, licensed guidance for Medicare beneficiaries and threatens the role of independent agents who serve as vital advocates for older Americans,” the organization said.

UnitedHealthcare notes that it had retained commissions for brokers in the majority of its plans. “The shift away from paying commissions for new members in around 20% of UnitedHealthcare MA plans allows us to prioritize stability and value for current members by maintaining the benefits that matter most,” according to the carrier’s spokesperson. “We recognize the critical role agents and brokers play in guiding and servicing beneficiaries, and that is why we continued to pay commissions related to existing members who stay enrolled in these plans for 2026.”

The reduction in Medicare Advantage commissions will hit smaller brokerages the hardest, Roberts says: “What the carriers are doing right now is going to push out some of your smaller agencies, your local hometown agents.”

For brokerages that have the capacity to do so, however, this current storm could be worth weathering. And some brokerages and agencies have launched major Medicare Advantage initiatives in recent years that they say are continuing.

Marsh McLennan is developing Medicare and Medicare Advantage support for its 20,000 employers and the 11 million people those organizations employ, says Jeff Snegosky, individual Medicare leader for the upper Midwest at Marsh McLennan Agency. That includes an expanding pool of Medicare advisors.

“We handle all things Medicare for them,” Snegosky says. “And so we go into those offices, Zoom or in person, and we’ll do Medicare 101s a couple times a year to educate the employees on all things Medicare, what they need to do, timelines, penalties to avoid, and more. And then we meet with every single employee individually to help navigate their Medicare decisions.”

CMS has in recent months increased its outreach to brokers and other insurance industry stakeholders, seemingly acknowledging their relevance, notes Mason. That has included sending members of the Medicare team to meetings of the National Association of Insurance Commissioners and scheduling a call with broker trade groups.

“One-third of all Medicare enrollments come through agents and brokers, according to CMS staff,” she says. “That’s a huge chunk of people. And again, as we know, it’s an older population. Some of them are not very tech savvy or computer savvy and they just want someone to hold their hand through enrollment. I think CMS is starting to realize the value that brokers bring to this and the education that brokers have.”

“You could invest tens of millions of dollars in bolstering the nonprofit counselors who do this. But absent that, most people want someone [such as a broker or agent] who’s going to explain the plans to them,” says Michael Adelberg, executive director of the National Association of Dental Plans and earlier director of the Insurance Programs Group at CMS.

This raises the question—could CMS intercede to address broker compensation?

“I can tell you what I heard from CMS on this topic, which is that while they do have the ability to regulate what is considered a reasonable limit for broker compensation, they cannot impose a floor under the regulations they work under,” Mason says. “I don’t know if that’s something that CMS would be willing to take on. It would take a regulation change, probably, and that’s kind of up to this administration, whether or not they want to attempt to do that.”

The Next Enrollment Period

Carriers are expected in early June to submit bids to CMS for 2027 Medicare Advantage payment amounts, which include estimates of health costs of offering plan benefits, administrative expenses, and anticipated profits. CMS usually issues its decisions in late August.

For brokers, much is riding on whether carriers continue to believe that their plans will pencil out in 2027. Snegosky is not optimistic. “I think [Medicare Advantage carrier enrollment withdrawals and broker commission cuts] are going to continue to happen going into this year and, hopefully, the market rights itself by the time we get to 2028.”

“We’re not in a position to speculate on specific 2027 commission levels or plan-by-plan approaches in advance of final decisions and formal communications,” says Blue Cross Blue Shield of Michigan’s Meeks. “Agents play a major role in Medicare Advantage in Michigan, and we want to continue to support them.”